The U.S. Treasury Department has officially categorized stablecoin issuers as “financial institutions,” requiring them to comply with the Bank Secrecy Act and implement anti-money-laundering regulations. In addition, the compliance officer responsible for issuer compliance must be an American resident with no criminal record.

The Treasury Department teams up with two major agencies to implement oversight, and stablecoin businesses are formally listed as financial institutions

Yesterday (4/8), the U.S. Treasury Department officially took a key step forward in regulation. Its Financial Crimes Enforcement Network (FinCEN) and the Office of Foreign Assets Control (OFAC) jointly issued a proposed rule aimed at comprehensively implementing the GENIUS Act passed in July 2025.

At the heart of this regulatory framework is defining “Authorized Payment Stablecoin Issuers” (PPSIs) as “financial institutions” under the scope of the Bank Secrecy Act (BSA). In a statement, U.S. Treasury Secretary Scott Bessent made it clear that the proposal’s primary goal is to protect the U.S. financial system from national security threats while ensuring that U.S. companies can continue to maintain their competitiveness within the stablecoin payments ecosystem.

The push for this legislation reflects the Trump administration’s ambition to position the United States as a global leader in digital assets, and also shows the government’s tough stance on national security defenses.

Strengthening anti-money-laundering and sanctions compliance, and granting issuers transaction-freezing authority

Under the proposed new rules, stablecoin issuers will bear legal responsibilities equivalent to those of traditional banks. Issuers must establish comprehensive anti-money-laundering (AML) and countering the financing of terrorism (CFT) programs and have the capability to proactively detect and report suspicious activity. The new rules explicitly require that issuers, at the technical level, have the authority to “intercept, freeze, and reject” specific transactions so that, in response to requests from law enforcement agencies, they can block funds linked to illicit actors.

Snir Levi, CEO of blockchain intelligence company Nominis, said that this shift turns issuers into gatekeepers similar to banks, and that in the future the market will see larger-scale wallet freezes, transaction interceptions, and asset seizure actions.

The Treasury Department believes these obligations are “tailor-made” and aligned with the purpose. The agency will adjust the standards based on the issuer’s size and business complexity, seeking to strike a balance between fighting crime and promoting technological development, and to avoid imposing an excessive administrative burden on the industry.

Carefully vet compliance officers and build a digital cash ecosystem through inter-agency cooperation

To ensure that the compliance program is effectively implemented, the proposal sets strict thresholds for staffing at issuers. In the future, stablecoin issuers must assign dedicated personnel to manage anti-money-laundering and terrorism-financing defense systems. The responsible person must reside within the United States, and must be prohibited from serving in this role if they have a record of criminal offenses such as insider trading, cybercrime, or financial fraud. In addition to the Treasury Department, the Federal Deposit Insurance Corporation (FDIC) and the Office of the Comptroller of the Currency (OCC) have also issued related implementation rules in sequence.

In its proposal, the FDIC specifically clarified that although the reserve deposits of stablecoin issuers would be protected, individual stablecoin holders would not be covered by federal deposit insurance. Moody’s senior vice president Warren Kornfeld analyzed that if all these requirements are fully implemented, a tiered digital cash ecosystem would be established within the banking system, and the boundary between traditional banks and digital assets would become even more overlapping.

- Related news: New U.S. FDIC rules for stablecoin reserves—strict requirements, and no $250k per-person deposit insurance

Market outlook and political maneuvering: Risks and opportunities facing stablecoin issuers

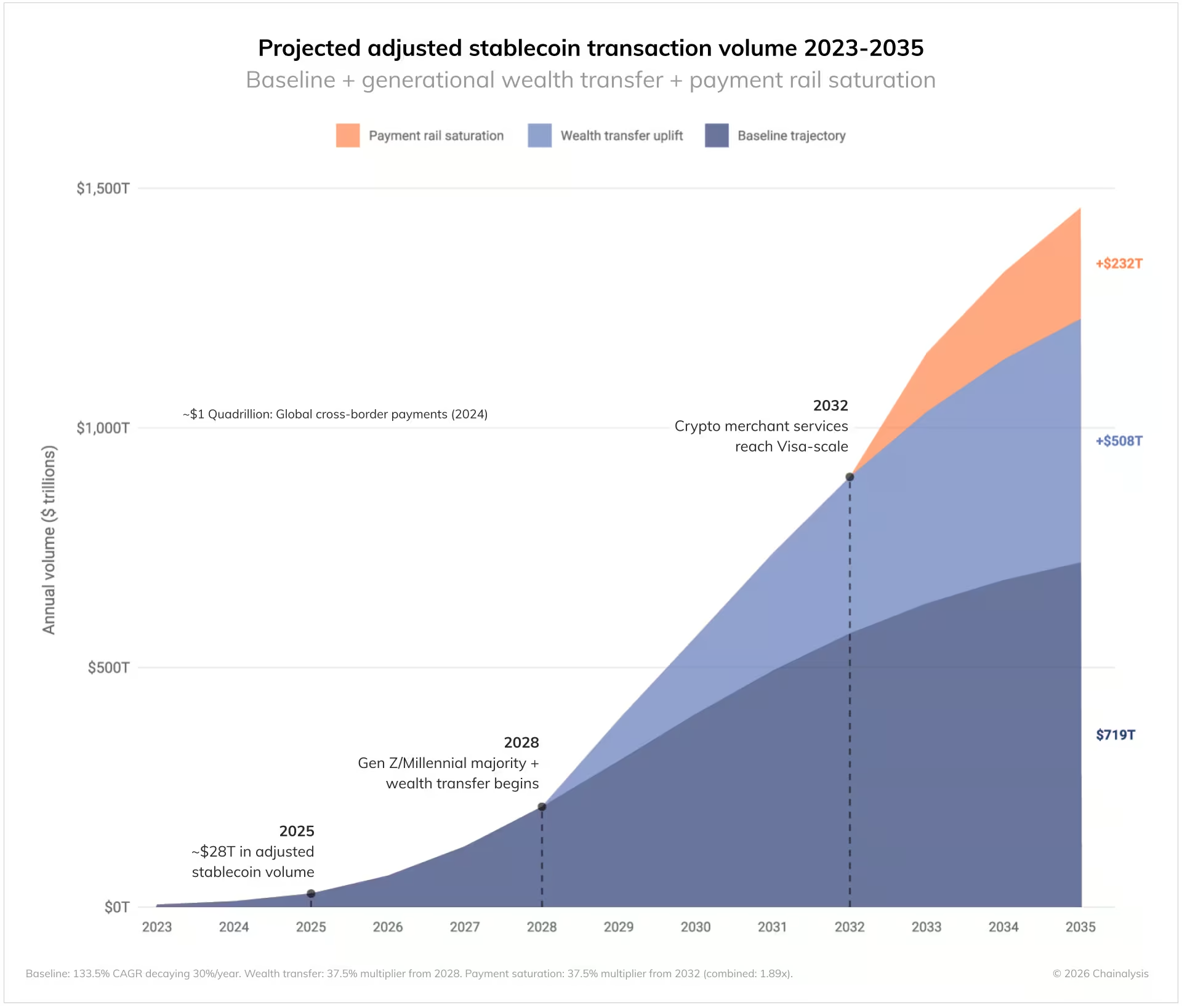

With the GENIUS Act expected to take full effect in 2027, major issuers such as Tether, Circle, Ripple, and World Liberty Financial, which is related to the Trump family, are all waiting for the final rule details to be finalized. Despite growing regulatory pressure, the industry generally believes that clearer regulations will help stablecoin assets move into the mainstream market. According to Chainalysis’s report, stablecoins’ annual transaction volume could soar to $1,500 trillion by 2035.

Source: Chainalysis Chainalysis predicts that by 2035, stablecoins’ annual transaction volume could soar to $1,500 trillion

However, political maneuvering has not stopped. The debate in the Senate over the CLARITY Act remains stuck in a stalemate. The White House Council of Economic Advisers opposes the stablecoin earnings ban, arguing that the ban does nothing to protect bank lending and would instead increase users’ costs.

On the international front, Iran recently announced plans to charge a $1 per barrel Bitcoin ($BTC) toll on oil tankers crossing the Strait of Hormuz to evade sanctions. The illegal financial risks arising from such geopolitical conflicts have prompted the U.S. Treasury to accelerate efforts to establish a strict control mechanism through the GENIUS Act.

Further reading

White House research: Banning stablecoin interest is almost useless for protecting bank loans—it instead deprives consumers of benefits

Hormuz Strait is open! Iran requires paying tolls with Bitcoin, and the Persian Gulf is still “filled with big ships”

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.