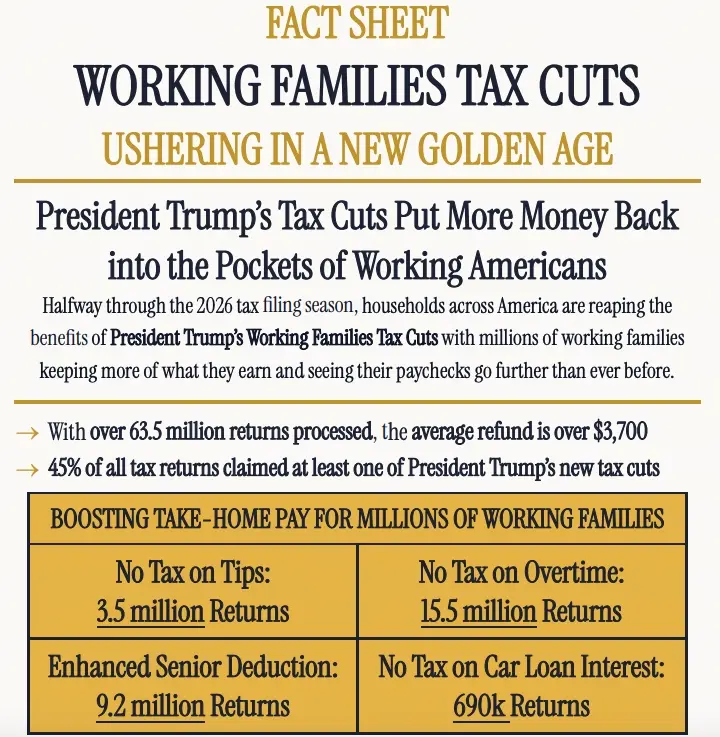

According to a notice issued by the U.S. Department of the Treasury, the Trump administration’s “Working Family Tax Relief” policy has demonstrated results in the 2026 tax season: over 63.5 million tax returns have been processed so far, with an average refund exceeding $3,700, and nearly 45% of filers claimed at least one new tax benefit. However, for cryptocurrency investors, this policy reform does not include new tax rules for digital assets; cryptocurrency gains are still reported under existing tax laws.

Four Core Tax Benefits: Who Benefits the Most?

(Source: U.S. Department of the Treasury)

The “Working Family Tax Relief” policy includes several deductions aimed at common income types for middle-income families. Here are the application figures released by the Treasury:

- Tax-Free Overtime Pay: Approximately 15.5 million returns claimed this, making it the most widely used new benefit so far.

- Senior Tax Benefits: About 9.2 million taxpayers applied, easing the tax burden on retirees.

- Tax-Free Tips: Around 3.5 million returns claimed, mainly for restaurant and service industry workers.

- Car Loan Interest Deduction: About 690,000 returns claimed.

Officials stated that these policies aim to reward overtime work, reduce financial stress for retirees and working-class families, with the core idea of putting “more money back into the pockets of American workers.”

“Trump Account” and Overall Refund Data

Beyond increased refunds, the government has also launched a new savings plan called the “Trump Account” to complement the tax reform. So far, about 3.5 million accounts have been opened, with over 800,000 qualifying for a $1,000 government pilot grant.

Treasury officials said early data from the 2026 tax season shows that the new policies have increased refunds and reduced tax liabilities for millions of families. However, some economists caution that the full impact of the tax changes will only be clearer after more returns are processed.

Cryptocurrency Taxation: Excluded from New Benefits

For cryptocurrency investors, the 2026 reporting rules are similar to previous years. The IRS still treats digital assets like Bitcoin and Ethereum as property, not currency, applying property tax rules: gains from selling crypto are subject to capital gains tax; income received in crypto is taxed as ordinary income; exchanges between different cryptocurrencies are taxable events.

Notably, starting from 2025 transactions, crypto brokers are required to issue Form 1099-DA reporting total sales proceeds of digital assets. Executives at exchanges like Coinbase warn that since 1099-DA reports only total proceeds and not cost basis, some filers may overestimate their taxable gains. Taxpayers should verify their cost basis before filing.

Although lawmakers continue to discuss potential crypto tax reforms—such as tax exemptions for small transactions and simplified reporting rules—these measures are not included in the current new tax relief policies. Cryptocurrency investors still face some of the most complex reporting scenarios in the tax code.

Frequently Asked Questions

Q: What are the main tax benefits covered by Trump’s Working Family Tax Relief policy?

A: Mainly includes tax-free overtime pay (about 15.5 million returns), senior tax benefits (about 9.2 million taxpayers), tax-free tips (about 3.5 million returns), and car loan interest deduction (about 690,000 returns). The newly introduced “Trump Account” savings plan also offers up to $1,000 in government pilot funding.

Q: Are cryptocurrency gains affected by the new tax relief policies?

A: No. Cryptocurrency gains are not covered by this tax relief; they are still reported under current IRS laws, treated as property rather than currency. Profits from sales are subject to capital gains tax; income received in crypto is taxed as ordinary income; exchanges between cryptocurrencies are taxable events.

Q: What should crypto taxpayers pay special attention to in 2026?

A: Starting from 2025 transactions, crypto brokers are required to issue Form 1099-DA reporting total sales proceeds, but without including cost basis. Filers should verify their cost basis to avoid overestimating taxable gains. Additionally, proposed crypto tax reforms (such as small transaction exemptions) have not yet been legislated.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.