ProCap Chief Information Officer and BitwiseInvest Advisor Jeff Park analyzes that this week’s Bitcoin sell-off was triggered by traditional financial deleveraging, as soft technology stocks plummeted and dragged Bitcoin down, forcing multi-strategy funds to close basis trades and triggering negative gamma effects in options that accelerated the decline. However, market makers’ hedging demands and buying interest at lower prices led to unexpected net inflows into ETFs, indicating that Bitcoin has become deeply integrated with the capital markets. Edited and summarized by QuDong, the full text is as follows.

(Background: Bitcoin recovers to 70,000! MicroStrategy surges 26%, Michael Saylor dismisses the downturn with “LFG”)

(Additional context: Bithumb’s massive mistake “airdropped 620,000 BTC” to users! Fortunately, 99.7% has been recovered)

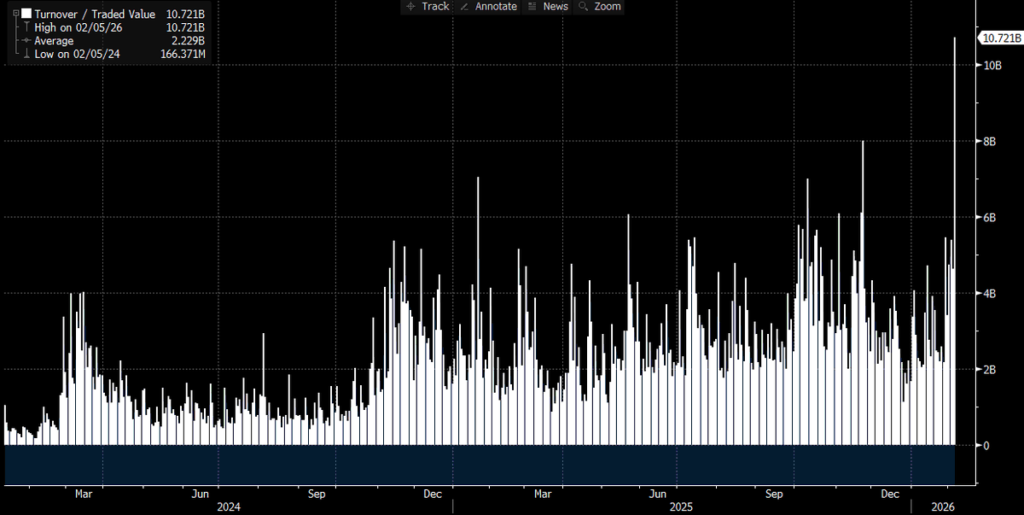

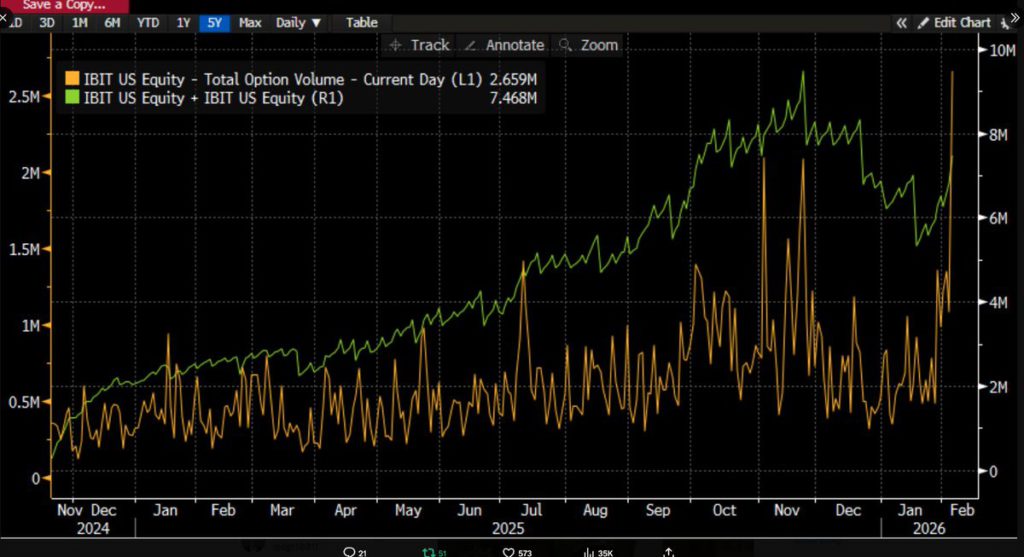

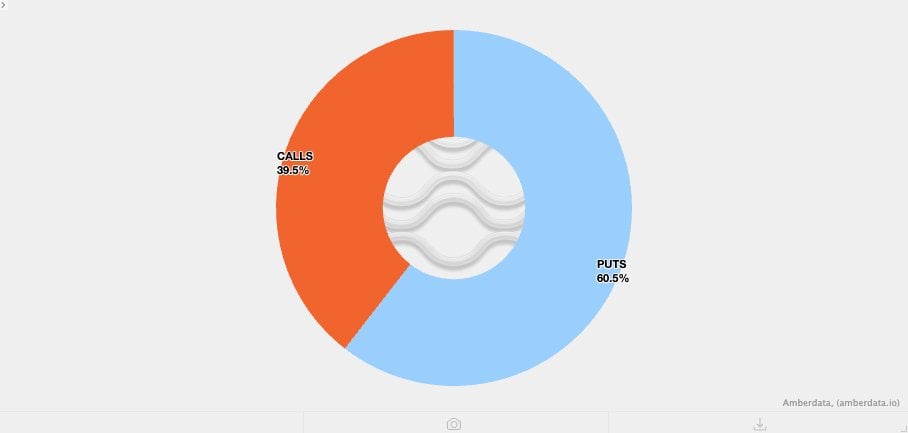

As time passes, more data surfaces, and the picture becomes clearer: this intense sell-off is related to Bitcoin ETFs, occurring on one of the most brutal trading days in the capital markets. We can confirm this because IBIT set a historic trading volume record (over $10 billion, twice the previous high—astonishing), and options trading volume also reached historic levels (see below), the highest number of contracts since ETF launch.

Compared to past trading activity, one anomaly stands out: the options activity was dominated by puts (not calls), based on volume imbalance (to be discussed further).

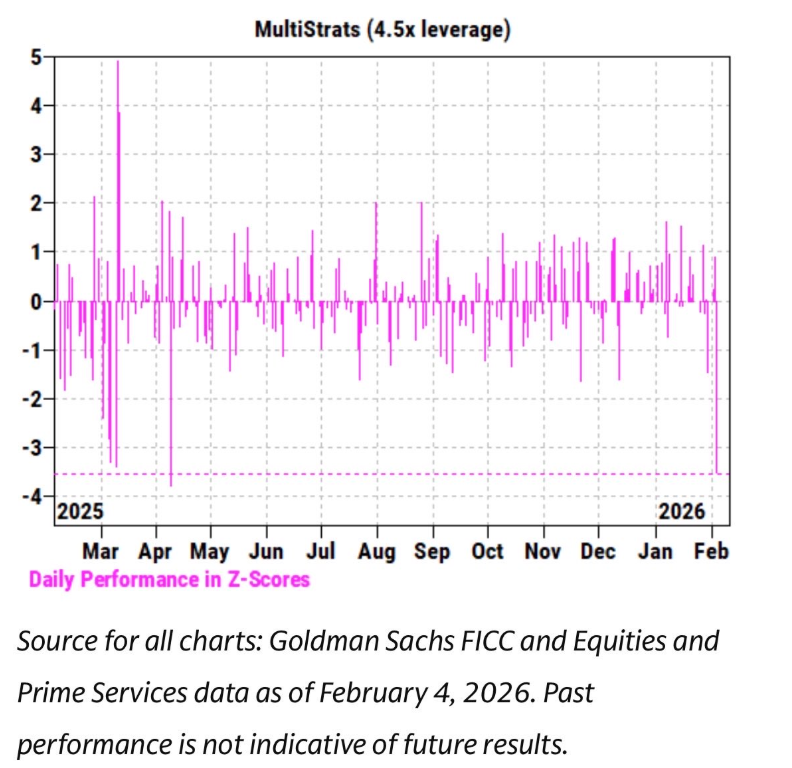

Meanwhile, we observe that over the past few weeks, IBIT’s price movements have been highly correlated with software stocks and other risk assets. Goldman Sachs’ Prime Brokerage team also released a report indicating that February 4th was one of the worst days ever for multi-strategy funds, with a Z-score as high as 3.5.

This is a rare event with only a 0.05% probability, ten times rarer than a three-standard-deviation event. It was catastrophic. After such events, risk managers in Pod Shop (the independent trading team under multi-strategy hedge funds) intervene, urgently reducing leverage across the board. This explains why February 5th was also a bloodbath.

Given all these record-breaking trading activities and the price decline of 13.2%, we initially expected to see net redemptions. Historical data, such as the record $530 million redemption on January 30 after a 5.8% drop, or the $370 million redemption on February 4 after consecutive losses, suggest that outflows of $500 million to $1 billion were likely.

But the reality was the opposite: we saw widespread net subscriptions—IBIT added about 6 million new shares, boosting assets under management by over $230 million. Other ETF complexes also experienced inflows totaling over $300 million and still increasing. This is quite perplexing. Perhaps the strong rebound on February 6 reduced outflows, but turning that into net subscriptions is a different story altogether.

This suggests multiple interacting factors, not a single narrative. Based on current information, I can hypothesize the following and propose my theory:

- The Bitcoin sell-off likely touched a multi-asset portfolio/strategy that is not purely crypto-native (possibly multi-strategy hedge funds as described above, or model-based investment portfolios like BlackRock’s, which rebalances between IBIT and IGV due to volatility).

- The acceleration of Bitcoin selling is probably related to the options market, especially on the downside.

- The sell-off did not result in a final net outflow of Bitcoin assets, indicating that it was mainly driven by dealer and market maker activities—“paper capital complexes”—that typically run roughly hedged positions.

Based on these facts, my current hypothesis is:

The catalyst was a broad deleveraging of multi-asset funds/portfolios due to risk assets’ downside correlation reaching statistically abnormal levels. This triggered a severe deleveraging, including Bitcoin risk, much of which was “Delta-neutral” hedges—such as basis trades or relative value trades against crypto-related stocks, or other types of trades—often used by dealers to lock residual Delta.

This deleveraging then led to short gamma effects, creating downward spirals that forced dealers to sell IBIT. But because the sell-off was too intense, market makers had to net short Bitcoin without considering inventory, creating new inventory and reducing the expected large capital outflows.

Subsequently, on February 6, we saw positive inflows into IBIT—buyers (which buyers?—question) took advantage of the lows, adding additional hedges to the small net outflows that might have occurred.

First, I tend to believe the trigger was driven by software stocks’ sell-off, as evidenced by their close correlation with gold. See the two charts below:

This makes sense to me because gold is generally not held as part of multi-strategy funds’ financing trades, although it may be part of RIA (Registered Investment Advisor) model portfolios. Therefore, this further supports the idea that the core event was related to multi-strategy funds. Then, the second point becomes even clearer—intense deleveraging involved hedged Bitcoin risks.

For example, basis trades on the Chicago Mercantile Exchange (CME), a favorite among Bitcoin trading platforms:

Please see the full dataset, including CME Bitcoin basis data for 30/60/90/120 days from January 26 to yesterday (thanks to industry expert @dlawant for the snapshots). It shows that the near-term basis jumped from 3.3% on February 5 to an astonishing 9% on February 6. This is one of the largest increases we’ve observed since ETF launch, indicating that basis trades were likely de-levered under instructions.

Think of giants like Millennium and Citadel—they were forced to unwind basis trades (selling spot, buying futures). Given their massive scale in the Bitcoin ETF complex, you can see how they caused such volatility. I have laid out my hypothesis here.

This leads to the third part. Since we understand the mechanism behind IBIT selling during broad deleveraging, what accelerated the decline? One possible “fuel” was structured products. While I don’t think the size of structured products alone explains this sell-off, it’s plausible that when everything aligns in ways unpredictable by any VaR model, it could trigger chain liquidation events.

This immediately reminds me of my days at Morgan Stanley, where knock-in puts could cause catastrophic scenarios—option Deltas exceeding 1, which Black-Scholes models don’t consider in vanilla payoffs.

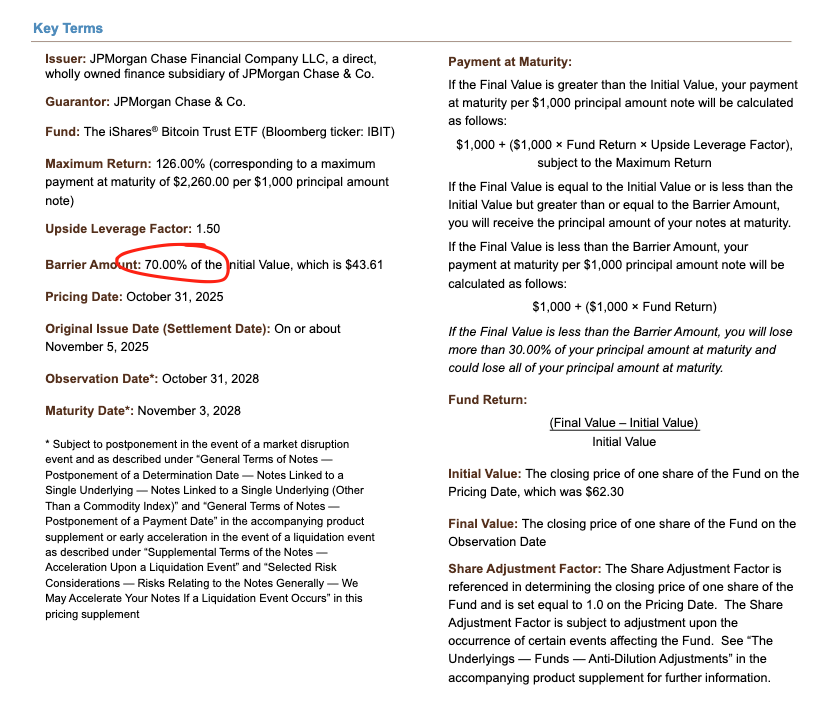

Look at a note priced by JPMorgan last November. The knock-in barrier was at 43.6. If the note continued to be priced as Bitcoin fell another 10% in December, you’d see large barriers around 38-39, which is at the core of the storm.

If these barriers are breached, and dealers use some short put combinations to hedge knock-in risks, the negative Vanna dynamic causes Gamma to change rapidly. Dealers would be forced to actively sell underlying assets in weak markets. This is exactly what we observed—implied volatility plummeted to record levels, nearly hitting 90%, indicating catastrophic gamma squeeze conditions, possibly forcing dealers to short IBIT to the point of net new units.

More imagination is needed here, as without more spread data, certainty is limited. But given record trading volumes, authorized participants (APs) could very well have been involved.

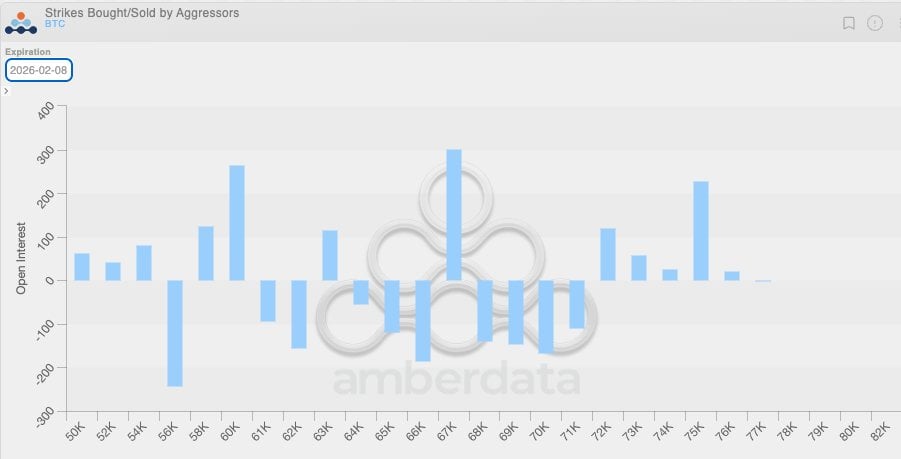

Now, combining this negative Vanna dynamic with the fact that volatility has been low, and recent weeks have seen crypto-native clients buying puts, it suggests that crypto dealers are also in short gamma positions—selling options at relatively cheap prices compared to the eventual realized volatility—thus exacerbating the decline. You can see this imbalance in the below chart, where dealers are mostly short puts in the $64,000 to $71,000 range.

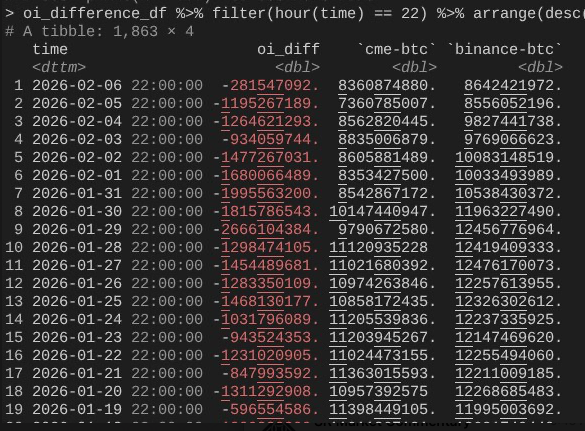

This brings us to February 6, when Bitcoin made a heroic rebound of over 10%. Here, I note an interesting phenomenon: CME open interest (OI) expanded much faster than Binance’s (thanks again to @dlawant, who checked hourly snapshots and aligned data to 4 PM Eastern).

You can see that from February 4 to February 5, open interest collapsed (confirming CME basis trades were unwound on February 5), but it may have rebounded yesterday to take advantage of higher levels, offsetting the capital outflows.

This ties everything together: you can imagine that IBIT subscriptions/redemptions were roughly flat because CME basis recovered, but prices were lower because Binance’s open interest had collapsed. This suggests that a lot of deleveraging likely came from crypto-native short gamma and forced liquidations.

So, this is my best theory for the events of February 5 and the subsequent February 6. It makes some assumptions, and unfortunately, there’s no single “culprit” (like FTX). But the key conclusion is: the catalyst came from traditional finance’s risk-off operations outside crypto, which pushed Bitcoin down to a level where short gamma, driven by hedging (not directional) activities, accelerated the decline, creating more inventory demand. This was quickly reversed on February 6 by traditional market-neutral strategies (though unfortunately, crypto directional positions did not follow).

While this may be unsatisfying, at least it’s clear that yesterday’s sell-off was not a 10/10 deleveraging event. That may be somewhat reassuring. Yes, I don’t believe what happened last week was an extension of 10/10 deleveraging. I read an article suggesting this disaster involved a non-U.S., Hong Kong-based fund engaged in a problematic JPY arbitrage trade. That theory has two major flaws.

First, I don’t believe any non-crypto prime broker would service such complex multi-asset trades with a 90-day margin buffer without risking insolvency when risk management tightens.

Second, if financing arbitrage was used to buy IBIT options to “escape,” Bitcoin’s decline wouldn’t necessarily accelerate—options would simply become out-of-the-money, with Greeks approaching zero. This implies the trade involved downside risk, and if you were short IBIT puts while long USD/JPY arbitrage, that prime broker would be doomed.

The coming days will be crucial as we gather more data to see if investors are absorbing at lows and creating new demand—very bullish signals. Currently, potential ETF inflows excite me because I still believe genuine RIA-style ETF buyers (not relative-value hedge funds) are diamond-holders—steadfast investors—and significant institutional progress is happening, driven by the entire industry and my friends at Bitwise. To observe this, I am monitoring net fund flows that are not accompanied by basis trade expansion.

Finally, this also indicates that Bitcoin has now been integrated into the financial capital markets in a highly sophisticated way. When we prepare for another wave of short gamma pressure, it will be more vertical than ever before.

The fragility of traditional margin rules is precisely Bitcoin’s antifragility. Whenever a counter-move surge arrives—in my view, since Nasdaq has increased options open interest limits, it’s inevitable—it will be spectacular.