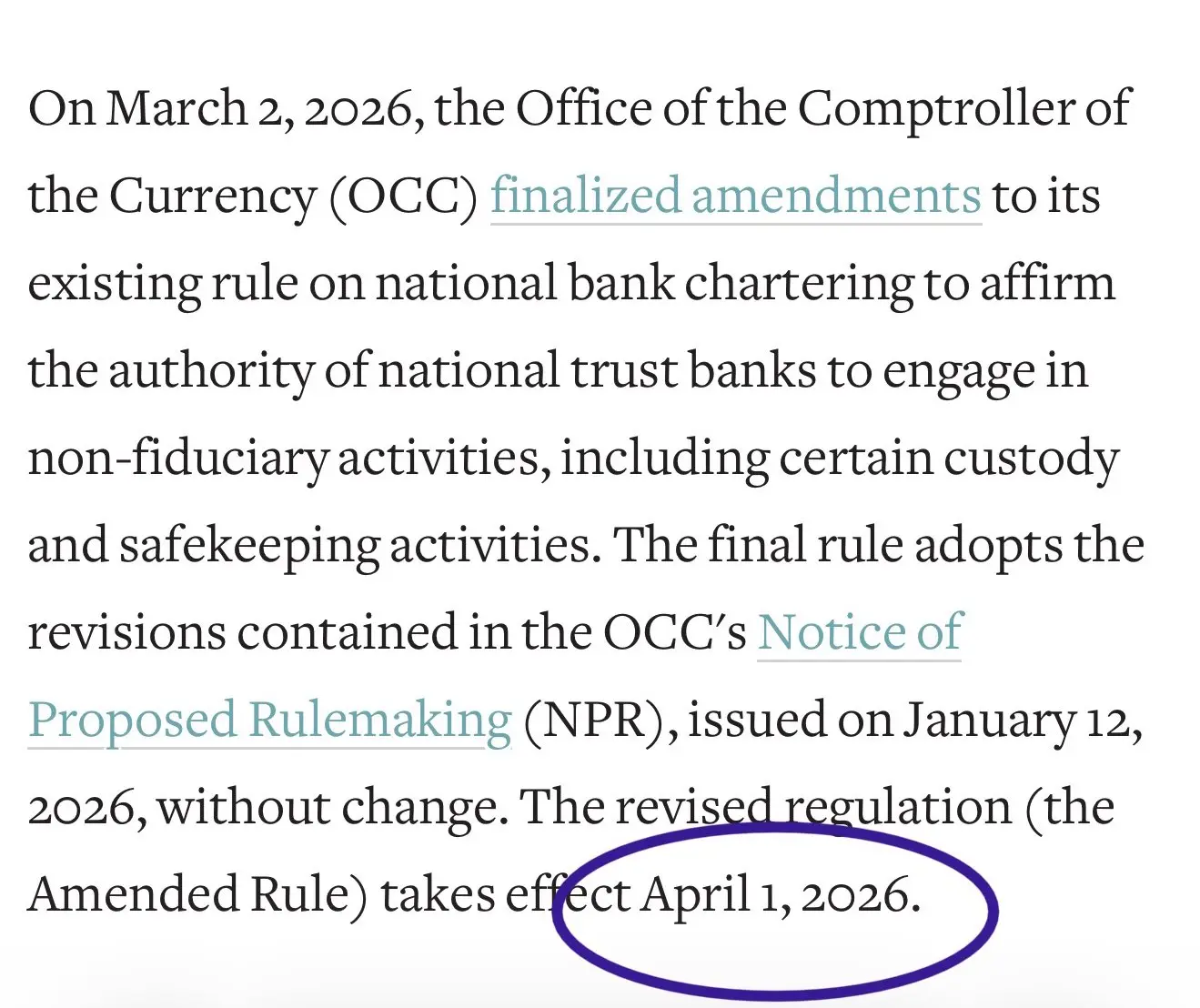

The Office of the Comptroller of the Currency (OCC) announced that it officially took effect on April 1, establishing an operating framework for national trust banks after meeting the prerequisites for opening. It provides a clear regulatory path for the conditional approval of the charter granted to Ripple for the Ripple-holding institution. Previously, the OCC had conditionally approved Ripple National Trust Bank’s charter application. This rule taking effect now means the above institutions are one step closer to full, formal operation.

The Core Mechanisms of OCC Announcement 2026-4: The Structural Significance of Terminology Revisions

(Source: JackTheRippler)

(Source: JackTheRippler)

The core of this OCC rule revision is replacing the term “fiduciary activities” with “the operations of a trust company and its related activities.” This terminology adjustment explicitly allows national trust banks to conduct non-fiduciary activities while carrying out fiduciary functions, especially digital-asset custody and safekeeping services.

Under the old framework, licensed institutions could only exercise discretionary trust management rights for clients in the capacity of agents. The revised terms explicitly allow “custody services”—meaning the institution holds customer assets under federal regulation, but does not exercise discretionary management rights. For institutional customers, this distinction determines the full range of services that can be provided. The OCC also emphasizes that this does not create new regulatory authority; rather, it sufficiently and precisely defines existing powers so that digital-asset custody business can be fully included within the scope of the charter.

Ripple Regulatory Milestone: Five Key Progress Checkpoints

Over the past 18 months, Ripple’s regulatory standing has undergone a significant transformation. The OCC’s new rules taking effect is the latest development among a series of milestones:

December 2025: The OCC conditionally approved Ripple National Trust Bank’s charter application, contingent on meeting opening requirements such as anti-money laundering (AML), know your customer (KYC), capital adequacy ratios, and risk controls

March 17, 2026: The SEC and CFTC officially classify XRP as a digital commodity, ending years of legal ambiguity and removing a major obstacle to institutional compliance positioning

April 1, 2026: The OCC announcement 2026-4 takes effect, establishing a complete operating framework for approved institutions

Federal Reserve master account application: Ripple has submitted a Federal Reserve (Fed) master account application. Kraken was the first to be approved and set a precedent. If approved, Ripple will be able to directly connect to the Fed’s payment and settlement system

It is worth noting that the Institute for Banking Policy, representing JPMorgan, Goldman Sachs, and Citigroup, is considering filing a lawsuit regarding the OCC’s approval of charters for crypto institutions—showing that traditional banks have come to view these approvals as competitive threats.

XRP Market Reaction and Current Technical Conditions

(Source: Trading View)

(Source: Trading View)

On April 1, XRP traded at about $1.3364, with a 24-hour gain of roughly 2.6%. Technical indicators showed their first bullish signals in about two weeks, and exchange funding recorded net outflows—suggesting that some holders are accumulating positions. Support is concentrated in the $1.30 to $1.35 range, while the initial resistance level starts around $2.20.

XRP is still about 63% below its 2025 all-time high of $3.65. Standard Chartered has cut its 2026 XRP forecast price from $8.00 to $2.80, citing deteriorating overall market conditions. Analysts point out that the key catalyst for the next major inflow of institutional funds will be the formal approval of a full trust bank license—not the conditional approval itself.

Frequently Asked Questions

What is the direct impact of OCC Announcement 2026-4 on Ripple?

Announcement 2026-4 officially establishes an operating framework for a national trust bank after completing the prerequisites for opening. For Ripple, this means that its conditionally approved charter franchise now has a clear regulatory pathway. Once it meets prerequisites such as AML, KYC, and capital adequacy ratios, it can move into full operations and provide digital-asset custody services for customers under federal regulation.

What does XRP being classified as a digital commodity mean for institutional investors?

On March 17, 2026, the SEC and CFTC formally classified XRP as a digital commodity, eliminating years of ambiguity around its legal nature. This classification removes a major obstacle for institutional investors to allocate XRP within the compliance framework, and provides a clearer legal basis for Ripple’s bank business application.

How important is Ripple’s Federal Reserve master account application?

A Federal Reserve master account allows licensed institutions to directly access the Fed’s payment and settlement network, bypassing commercial banks’ intermediary role. If Ripple is approved, it will be able to directly participate in U.S. federal payment infrastructure, significantly enhancing its capability as an institutional-grade digital asset service provider, and potentially accelerating the adoption of the RLUSD stablecoin within the U.S. banking system.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.