Author: Changan, Biteye Content Team

A few days ago, many KOLs on X suddenly noticed that the badges symbolizing their partnership with Kalshi had disappeared from their accounts.

Prediction News reported on this incident, followed by a humorous screenshot: Polymarket’s official account quietly liked the article.

The business rivalry between Polymarket and Kalshi has been ongoing for a long time, and the prediction market is entering a true duopoly era.

On one side is the crypto-native Polymarket, and on the other is Kalshi within the compliant financial system.

The essence of this competition isn’t about which company is stronger, but about: who will control the future information pricing power—Crypto or Wall Street.

Therefore, this analysis is worth doing. 👇

1. Business War Chronicle: From Regulatory Battles to Offline Confrontations

Over the past year, the competition between the two has evolved from product battles to a three-dimensional war involving channels, regulation, and public opinion.

1.1 Valuation Race: Capital Counterattack in 41 Days

On October 7, 2025, Polymarket announced it received a strategic investment of $2 billion from ICE, valuing the company at $9 billion.

Three days later, Kalshi announced a $300 million Series D funding round, with a valuation of $5 billion. The timing was so precise it’s hard to believe it was just coincidence.

But Polymarket clearly isn’t planning to stop. On October 23, Bloomberg reported that Polymarket was in talks with investors to prepare for a new funding round, aiming to raise its valuation to $15 billion.

By November 20, Kalshi responded: completing a $1 billion financing, with its valuation jumping directly to $11 billion, led by Paradigm. Not only did it surpass Polymarket’s previous $9 billion valuation, but it also rapidly approached the $15 billion target. And this was only 41 days after its last D-round announcement.

1.2 Cultural Breakthrough: Traffic Competition

On September 24, 2025, “South Park” Season 27 Episode 5 “Conflict of Interest” released a trailer featuring prediction market content.

As soon as the news broke, both platforms realized an opportunity: this was the first time prediction markets entered mainstream culture’s view. Whoever could convert this attention into trading volume first would gain a bigger slice of the breakout dividend.

Kalshi and Polymarket quickly launched a batch of markets highly related to the storyline, allowing users to bet on plot developments in real time.

On the day of the episode’s release, the Kalshi team collectively changed their profile avatars to South Park cartoon styles and flooded X, embedding their brand into the day’s hot topics. Both platforms seized every marketing opportunity to turn trending topics into trading activity.

1.3 Ecosystem Accounts and Badge Wars

As user numbers surged, both Polymarket and Kalshi nearly simultaneously launched affiliate account programs in late 2024, starting to assign badges to KOLs, traders, and ecosystem projects on X.

Polymarket moved faster: Trader badges to verify active traders, encouraging them to share strategies and holdings on X to drive traffic. Builder badges targeted ecosystem projects, attracting developers to build applications on the platform and gain exposure through official endorsement.

Meanwhile, Polymarket also launched a $1 million Builders Incentive Program, directly offering cash to attract developers into the ecosystem.

Kalshi quickly followed with a broader badge system covering sports, culture, and trader verification, replicating this model in its stronger markets like sports and mass markets.

Today, prediction traders on Twitter either display Polymarket badges or Kalshi badges.

1.4 Physical Marketing Battles: Manhattan Free Goods War

On February 2, 2026, Kalshi announced on X that it would provide free food at Westside Market supermarket from noon to 3 pm the next day, with a maximum of $50 per person. The announcement drew long lines on-site, with students and low-income groups flocking in, creating a lively scene.

The next day, February 3, Polymarket responded swiftly, announcing the opening of its first pop-up free food event in New York, open to the public for five consecutive days. The rules were simple: customers could fill a tote bag with food and take it away, no conditions attached. At the same time, Polymarket announced a $1 million donation to Food Bank for New York City to help address food security issues across the city.

These two events played out back-to-back, with intense competition.

1.5 Regulatory and Political Resource Arms Race

Both sides’ lobbying efforts in Washington never stopped, with both bringing Donald Trump Jr. onto their platforms to mobilize Republican regulatory resources and to lay political chips in the public opinion arena.

But beneath the surface, the real battleground is distributed across two dimensions: regulatory loopholes at the CFTC and legal battles in state courts.

Polymarket, leveraging offshore structures, evades direct regulation while quietly expanding into the US market through acquisitions like QCEX. Kalshi, on the other hand, chooses to confront head-on, holding the first CFTC-licensed prediction market license, but this has made it a target for state prosecutors—at least four states have sued it, accusing it of illegal betting activities with local users.

This unglamorous business war is no longer just about products but a full-scale battle over political capital and traffic monopoly.

2. Hardcore Comparison: Five Dimensions of the Two Giants

2.1 Trading Data Comparison: Disjointed Growth of Political Cycles and Sports Calendars

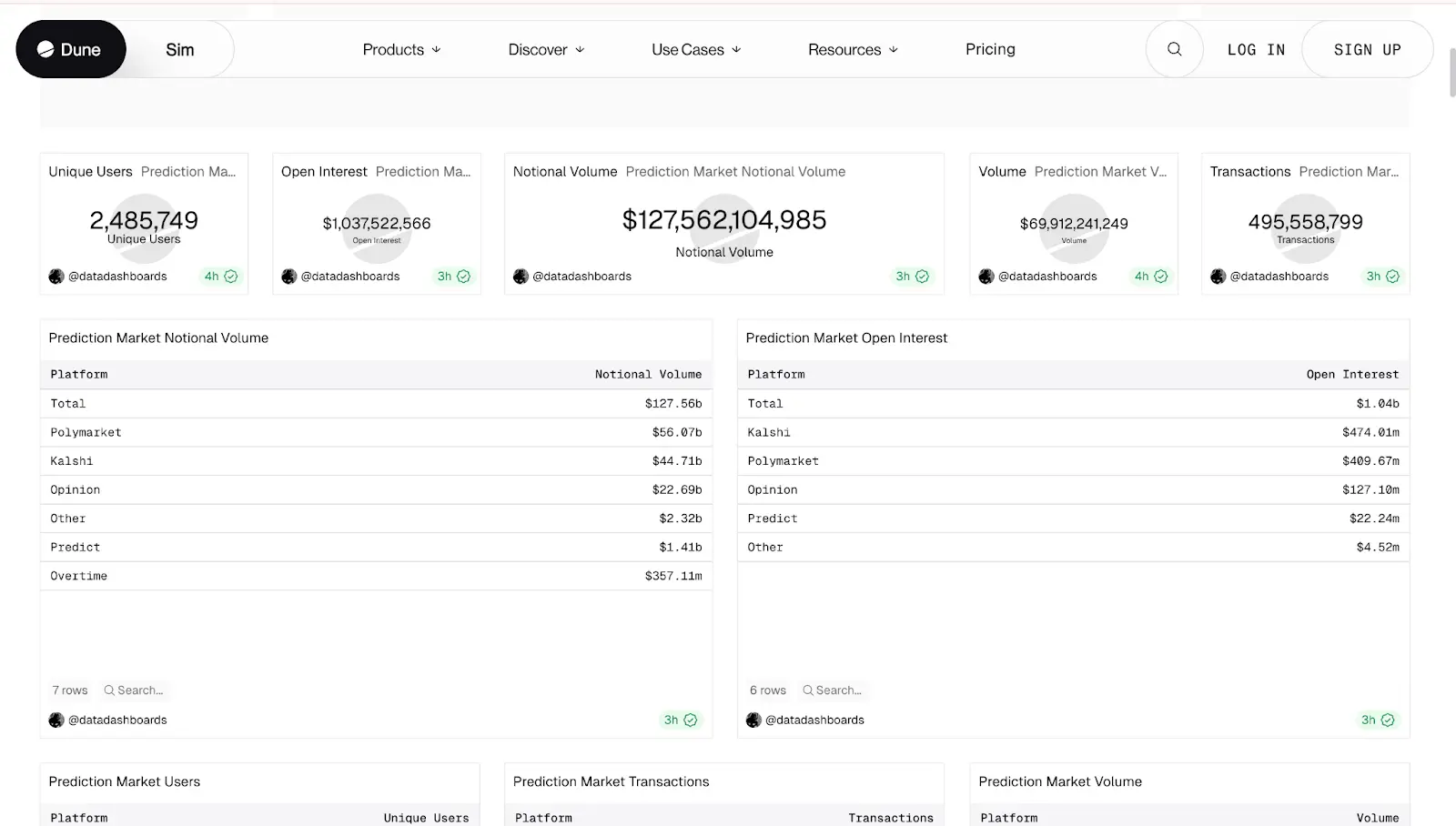

As of February 2026, the total Notional Volume of the prediction market industry reached $127.5 billion, with actual trading volume at $69.9 billion, and 2.49 million unique users. Open interest exceeded $1 billion.

Polymarket and Kalshi together hold about 79% of the market share. Polymarket leads with a $56.07 billion Notional Volume, followed by Kalshi at $44.71 billion. In terms of open interest, Kalshi slightly leads with $474.01 million over Polymarket’s $409.67 million, together accounting for over 85% of the total market OI.

Trend analysis shows both rely heavily on event-driven growth. Polymarket’s OI peaked around the 2024 October US election at $500 million, then declined; Kalshi’s OI surged starting with the 2025 NFL season, reaching a historical high at year-end 2025.

Both platforms are growing, but driven by different factors—one by political cycles, the other by sports schedules.

(Source: Dune, as of 2.26 11:00)

2.2 Revenue Comparison: Proven Dynamic Fee Rates vs. Emerging Taker Fees

The two platforms have fundamentally different fee structures.

Kalshi

Uses probability-weighted dynamic fee rates: charges transaction fees based on contract prices, with the rate peaking at 50 (50/50 probability) and decreasing toward 0 or 99. For a $100 trade, the maximum fee is about $1.74, with an effective rate of approximately 1.2%.

In 2024, revenue reached $24 million; in 2025, $260 million—a 994% increase. But revenue is highly seasonal: NFL season (September-November) contributed $138 million in a single quarter, with December hitting a record $63.5 million. Off-season revenue drops significantly, showing clear seasonality.

Polymarket

Took the opposite approach: until late 2025, Polymarket operated at a loss with zero fees, relying on free user acquisition. It wasn’t until February this year that they officially introduced Taker Fee dynamic rates in sports markets. In the first week after charging, Polymarket’s fee revenue exceeded $1 million. According to DefiLlama, in the past 30 days, Polymarket earned $3.18 million, with revenue only starting to trend upward from January this year.

It’s worth noting that daily markets might become future revenue sources for Polymarket. High-frequency, short-cycle markets generate more trades, and users in these markets are less sensitive to fees, similar to meme markets.

Comparison: Kalshi’s fee model is validated but relies heavily on sports seasons. Polymarket’s fee system is just beginning; although its annual revenue is still a fraction of Kalshi’s, the phase of using zero fees to attract liquidity is over, and they are now serious about making money.

2.3 User Profiles: Licensed Elite vs. Global Retail

The user structures of both platforms are largely shaped by regulatory environments.

Kalshi holds a CFTC license, allowing it to legally serve US users, mainly focusing on the domestic market.

Polymarket, after acquiring QCEX in late 2025, re-entered the US market. Prior to that, it mainly operated overseas. This “exile period” helped it build a broader international user base.

Revenue structures also reflect user differences.

Kalshi’s revenue is 89% from sports markets. Its user behavior resembles traditional sports betting: high trading frequency, smaller individual bets, and seasonal activity spikes. During NFL season, user activity surges, then drops off after the season ends, showing clear seasonality.

Polymarket’s structure is quite different. Political and macro markets dominate, attracting many institutional traders hedging macro risks. Bet sizes are significantly larger—for example, during the 2024 US election, a French trader bet over $50 million and made $85 million profit. Such volume is almost impossible in traditional sports betting.

2.4 Channel Moats: Distribution Agents vs. Developer Ecosystem

By late 2025, Robinhood and Coinbase had launched prediction market features on their platforms, both partnering with Kalshi. Not just brokerages, but sports platforms like PrizePicks and Underdog also direct their existing sports betting users to Kalshi. In December, Kalshi formed a Prediction Market Alliance with Coinbase, Robinhood, and Crypto.com.

The logic is straightforward: Kalshi holds a CFTC-licensed designated contract market license. For licensed financial institutions, integrating with Kalshi is like connecting to a traditional futures exchange—clear process, low compliance costs, manageable risks.

Polymarket’s approach is entirely different. They don’t focus on channel distribution but are building underlying infrastructure, hoping others will develop products around it.

A clear example is the recent acquisition of Dome, a YC Fall 2025 batch project. Dome provides prediction market APIs, allowing developers to write code once and access data and liquidity from multiple platforms like Polymarket and Kalshi.

Today, with Vibe Coding popular, developers can directly call Dome’s API to build trading bots, data dashboards, or embedded market components. AI agents can also execute prediction strategies automatically via this API.

Looking at both routes together, it’s clear: Kalshi is expanding channels through partnerships to bring in users and volume. Polymarket is building the underlying layer, expecting developers to grow applications on top. One path emphasizes business network expansion; the other relies on ecosystem self-formation. Once network effects kick in at the infrastructure level, copying becomes very difficult for later entrants.

2.5 Marketing Strategies: Brand Exposure vs. Community Viral Growth

Both companies’ marketing strategies align closely with their user structures.

Kalshi focuses on brand exposure, using very traditional, direct methods. During the NYC mayoral election, they placed real-time odds ads on Times Square, Penn Station, and subway trains, making prediction probabilities visible on street screens. During the NBA Finals, Kalshi produced a $2000-cost TV ad with AI tools in just two days, airing during prime time and garnering over 30 million views on X.

They also partnered with CNN and CNBC, with Kalshi’s data appearing directly in news broadcasts. For ordinary viewers, this acts as an official endorsement, boosting trust.

Polymarket’s approach is quite different, leaning toward community-driven virality.

They designed a detailed referral system: users share a unique link, earning $0.01 per click. If the referred person deposits over $20, the referrer gets a $10 CPA reward.

Once clicks and transactions reach certain scales, additional rewards are distributed, creating ongoing incentives for promoters—similar to meme trading platforms’ affiliate links.

Additionally, Polymarket actively cultivates its content ecosystem, supporting influencers like @BrosOnPM. These KOLs serve prediction market builders and traders, producing daily content, connecting developers with traffic, and fostering internal circulation.

3. Who Will Be the Ultimate Winner?

The previous data describes the current state of both companies, but the present pattern doesn’t determine the future. Prediction markets are still in early stages, with many variables—regulation, new competitors, unproven business models.

Rather than giving a definitive conclusion, it’s better to identify key questions that will truly decide the outcome.

Both are expanding into each other’s territory

From their actions, both recognize their weaknesses and are actively addressing them.

When Polymarket re-entered the US, its first contracts were all sports-related. Later, it signed official partnerships with MLS, NHL, and the New York Rangers, using these league brands to endorse its sports market.

A platform that started with politics is now aggressively entering sports.

Possible reasons:

- Political markets may currently face less US regulatory scrutiny; sports markets are more easily accepted.

- To seize Kalshi’s US market share.

Kalshi is also not idle. They signed deals with CNN and CNBC, integrating their odds data into news graphics. Having started with sports, they now aim to establish media-level credibility in politics.

However, the risks are not equal. Polymarket has genuine trading volume in both politics and sports; Kalshi’s volume is almost entirely in sports. This structural difference will become a regulatory concern later.

Is the biggest channel partner also the most dangerous competitor?

Robinhood is one of Kalshi’s most important retail distribution channels, contributing over half of its trading volume in 2025. Coinbase has also launched prediction markets in all 50 US states, clearing through Kalshi.

But both made similar moves:

- Robinhood and Susquehanna jointly acquired MIAXdx.

- Coinbase acquired The Clearing Company.

Both are building CFTC-licensed trading infrastructure, expected to go live in 2026. After launch, they can choose to continue sharing revenue with Kalshi or operate independently, leveraging user data, trading habits, and liquidity they’ve accumulated.

For Kalshi, this isn’t just channel risk; it’s a concrete threat with a timeline. Its channel moat is essentially a temporary first-mover advantage.

Polymarket’s fee model: a key step in validating its business model

In 2025, Polymarket’s total trading volume exceeded $33.8 billion, but revenue was nearly zero. Yet, a $9 billion valuation requires revenue support—2026 is the year to deliver.

It started testing fees in crypto markets, then expanded to sports markets on February 18, 2026. The logic is clear: both are daily settlement markets with high trading frequency, small bets, and quick turnover, making users less sensitive to fees than long-term macro or political contracts. Charging here minimizes impact on core liquidity.

But risks are evident. Prediction market liquidity depends entirely on user-provided volume, with no market makers. If professional traders feel fees cut into arbitrage opportunities, they can withdraw instantly.

History shows many exchanges have suffered liquidity crashes due to poorly timed or sized fees, leading to a death spiral of declining liquidity and user exit.

Polymarket currently uses maker rebates to hedge this risk, returning part of taker fees to order submitters to maintain depth.

Whether it can establish stable revenue without driving away liquidity is fundamental to its valuation. Fee experiments have just begun; the full answer will be clear by the end of 2026.

Conclusion: No Kings in War, Only Era’s Winners

Prediction markets are still young. It’s too early to declare who will win or lose. But the outlines of both companies are becoming clearer.

Kalshi’s strengths are obvious: first-mover compliance advantage, mature retail channels, and a proven revenue model. But it faces significant pressures: high sports revenue dependence, ongoing regulatory uncertainties at the state level, and the looming threat of Robinhood and Coinbase building their own exchanges.

Polymarket’s advantages are also clear: deepest global liquidity, near-competitor-free in political and macro sectors, and a growing developer ecosystem. But its business model remains unproven; whether its fee mechanism can truly work out will only be known by late 2026.

The interesting part of this competition is that their current positions don’t fully overlap. Kalshi is expanding retail reach, while Polymarket focuses on information density and market depth. The real showdown will likely occur after Polymarket’s US sports market matures and Kalshi’s political market capabilities improve.

Until then, the industry space remains broad enough for both paths to develop in parallel.