The Federal Reserve pushes for streamlined main account sparks controversy, crypto banks call for relaxed limits, traditional banks worry about regulatory asymmetry, and payment system reforms face an uncertain future, becoming a key policy battleground in 2026.

Federal Reserve’s Streamlined Account Proposal Sparks Divergent Opinions

The U.S. Federal Reserve (FRB) officially closed the public comment period on the “Skinny Master Account” policy proposal on February 7, 2026, receiving approximately 30 letters of feedback from various sectors of the financial industry.

The core controversy of this proposal lies in whether to allow non-traditional financial institutions, such as virtual currency banks and new entrants, to directly access the U.S. central bank settlement system. Master accounts are critically valuable for financial institutions because they provide the most direct access to U.S. monetary supply and enable institutions to settle transactions without relying on third-party partner banks.

Federal Reserve Board Member Christopher Waller first proposed this idea in October 2025, calling it a “lean” account designed to promote financial innovation while limiting account functionalities to reduce potential risks. However, this compromise proposal has led to significant opposition between crypto industry players and traditional regional banks, with heated debates over entry barriers to the financial system and payment security.

Further Reading

Federal Reserve embraces crypto! Plans to introduce streamlined master accounts for stablecoins and crypto institutions to connect directly to payment systems

Federal Reserve proposes streamlined master account concept! Crypto firms may gain “limited” access to Fed payment system

Funding Limits Spark Debate, Crypto Banks Urge Relaxation

According to the Fed’s plan, the streamlined master account would face strict operational restrictions, including non-interest-bearing balances and an inability to borrow via the Fed discount window. The most controversial clause concerns overnight balance limits, with the Fed considering capping the funds that financial institutions can hold at the end of the business day to either 500 million USD or 10% of the total assets of the account holder, whichever is lower.

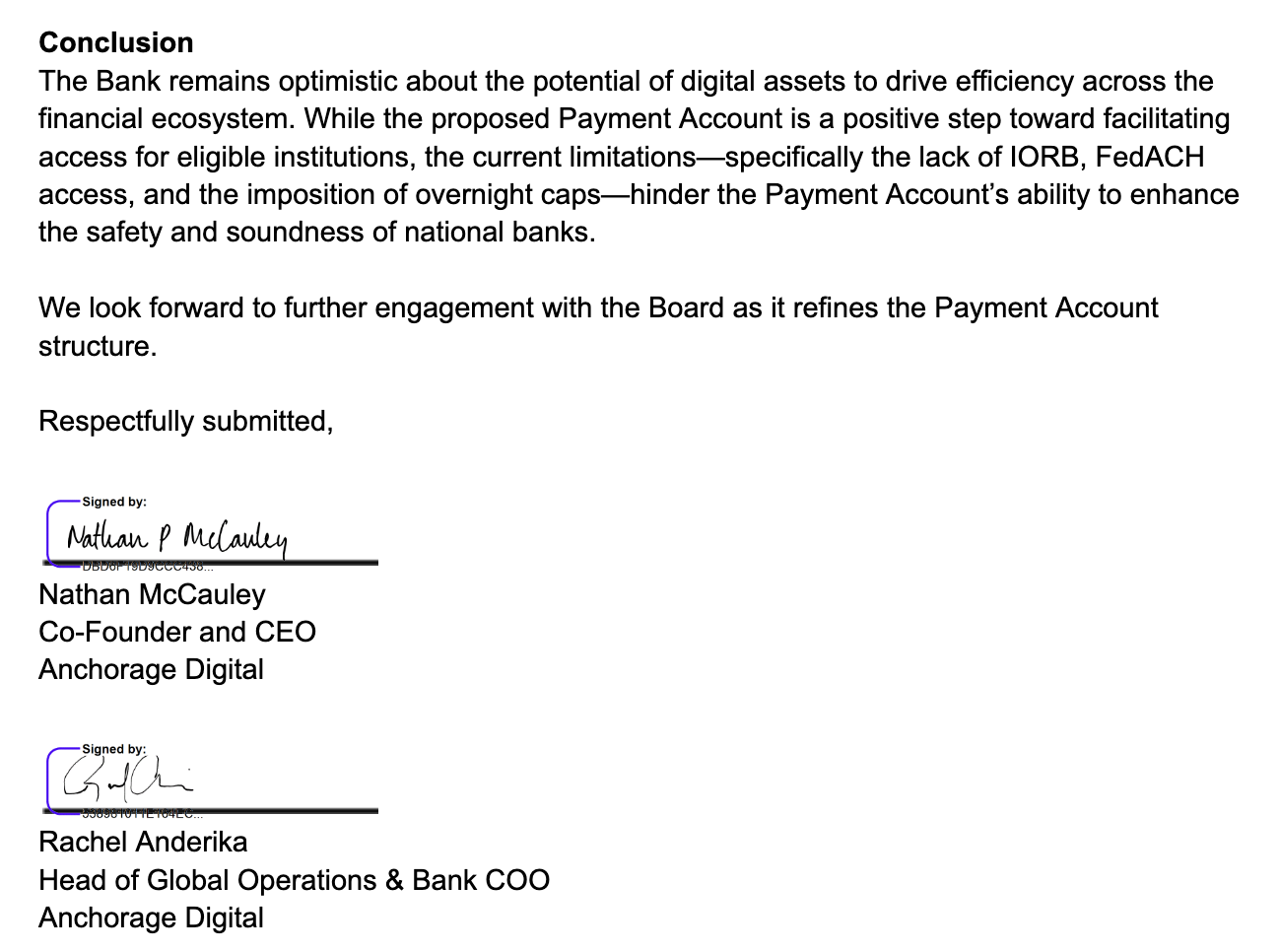

Anchorage Digital Bank, the first crypto bank licensed by the U.S. federal government, submitted comments on February 6, 2026, stating that while they support the Fed’s innovative initiatives, the existing capital limits are extremely unreasonable. Anchorage pointed out that such limits would force institutions to transfer customer funds to correspondent banks overnight, reintroducing credit and operational risks that the proposal aimed to eliminate, and could diminish the value of payment accounts in terms of business continuity and disaster recovery. Therefore, the bank advocates for removing or significantly raising these limits as a necessary step to maintain the stability of the settlement system.

Image Source: Anchorage Digital Bank Anchorage Digital Bank suggests removing or significantly raising limits in submitted comments

Consortium Sees Proposal as Catalyst to Promote Regulatory Legislation

Supporters, including blockchain payment coalitions initiated by organizations like the Solana Foundation and Sui Foundation, refer to the Fed’s proposal as a “delayed move.” They believe enabling new financial institutions to access the central bank’s settlement system is crucial for implementing the federal-level new stablecoin regulation bill, the “GENIUS Act.” The coalition emphasized in their letter that the advancement of the GENIUS Act demonstrates that stablecoins and blockchain technology are recognized as innovative components of the U.S. payment system, and the Fed should seize this opportunity to support these technological innovations while fulfilling its responsibility to ensure payment system security.

By implementing the streamlined master account, regulated virtual currency firms can participate more efficiently in the federal financial system, aligning with the U.S. government’s broader goals of strengthening virtual currency legislation and advancing market structure bills. For these emerging institutions, direct settlement pathways not only enhance market competitiveness but also represent a key milestone in integrating digital assets with the traditional financial system.

Traditional Banks Worry About Risks and Regulatory Asymmetry

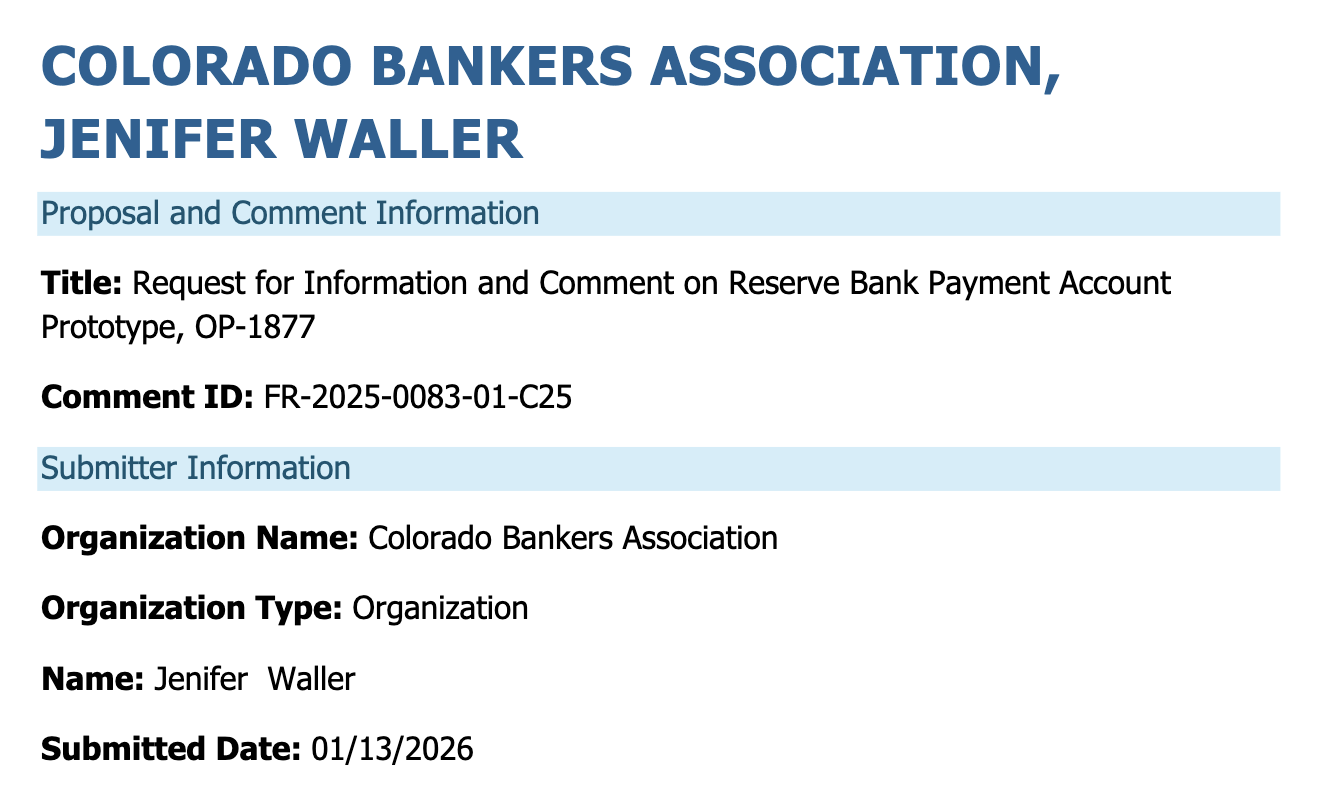

Conversely, the traditional banking industry has expressed strong caution and opposition to this proposal. The Colorado Bankers Association, representing over 126 banks and 20,000 employees, stated that the Fed’s master accounts are traditionally granted only to insured, highly regulated, low-risk institutions.

The association pointed out that insurance institutions undergo strict regulatory scrutiny and have clear restrictions on their commercial activities. Delegating account authority to institutions outside the low-risk category could threaten the defenses of the entire payment system.

Image Source: FED Colorado Bankers Association comments suggest that delegating account authority to higher-risk institutions could threaten the entire payment system’s defenses.

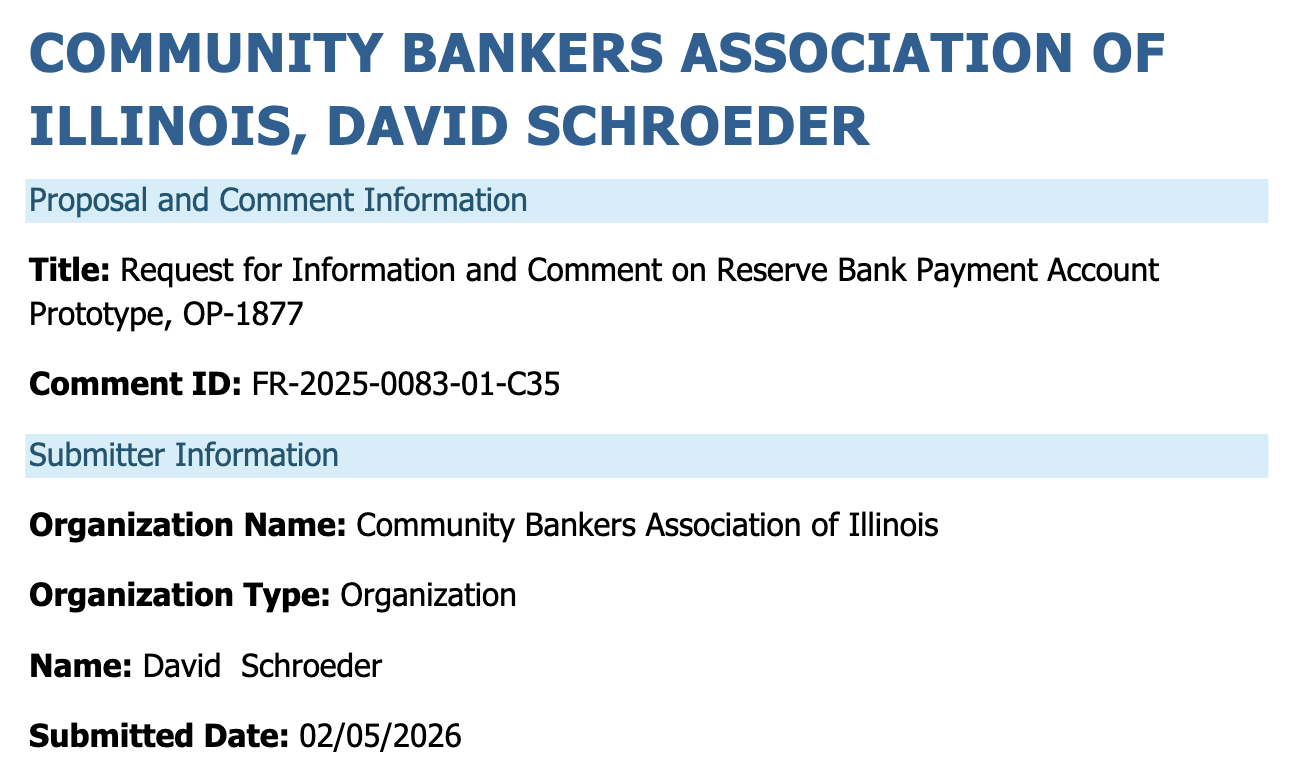

Similarly, the Illinois Bankers Association, representing 265 financial institutions in Illinois, expressed similar concerns, arguing that emerging financial institutions are not subject to the same rigorous regulatory compliance. They claim that allowing these “new financial institutions” to access Fed services would create an unfair competitive advantage over regional banks and could pose significant, unpredictable risks to consumers, the overall financial system, and U.S. taxpayers.

Image Source: FED Illinois Bankers Association believes emerging financial institutions are not subject to the same level of regulatory compliance

Policy Power Struggles Continue, Impacting Future Payment Landscape

The current dispute over the streamlined master account reflects the complex tug-of-war within U.S. financial regulation amid technological transformation. Despite market volatility—such as Bitcoin prices briefly falling below 60,000 USD in early 2026, and ongoing debates over stablecoin interest and reserve issues— the Fed’s pace of financial system modernization remains steady.

The Fed must balance promoting payment system efficiency with preventing systemic risks, especially amid debt pressure highlighted by Strategy’s CEO and market turbulence caused by incidents like Bithumb’s erroneous fund transfer. Ensuring the stability of financial infrastructure is more critical than ever.

Further Reading

Bitcoin crashes drag down markets! Strategy Q4 net loss of $12.4 billion, crypto concept stocks suffer collectively

2000 KRW becomes 2000 Bitcoins! Bithumb’s mistaken transfer sparks flash crash, prompting urgent regulatory investigation

The future policy direction will not only determine whether crypto banks can truly mainstream but also profoundly influence the U.S.’s competitive position in the global digital economy. The account reform initiated by the Fed will be a key development to watch in 2026.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.