Author: Fintax

Basic Positioning of CARF

CARF is an international automatic exchange framework for tax information related to crypto assets. It designates crypto asset service providers as the reporting entities, supporting tax authorities in various jurisdictions to obtain information on crypto transactions related to their taxpayers.

Global Implementation Progress and Timeline

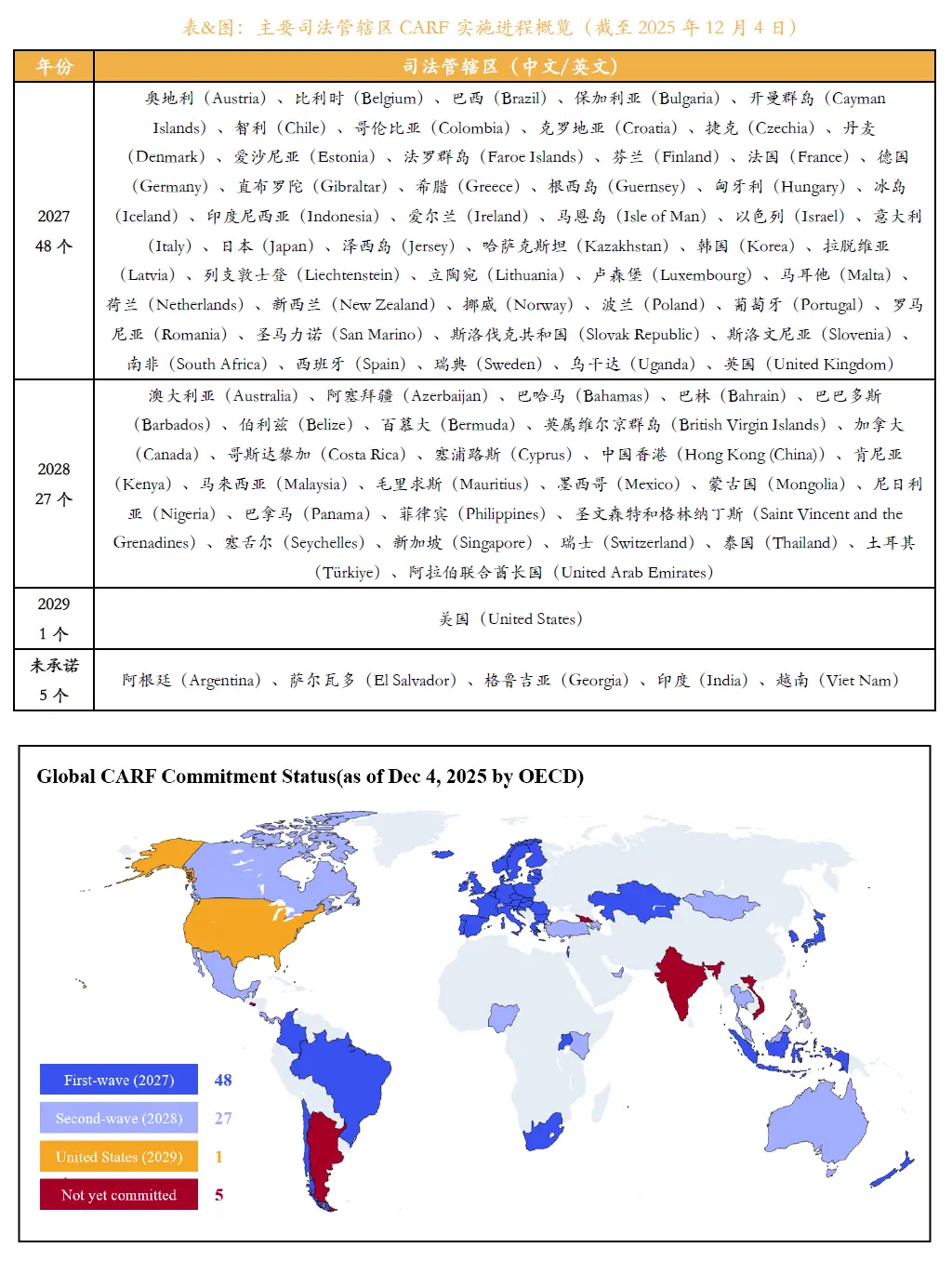

According to information released by the OECD Global Forum, by the end of 2025, 76 countries and regions have committed to implementing CARF, with phased rollout of the system.

The first batch of jurisdictions plans to conduct the initial automatic information exchange in 2027, mainly including the UK and EU member states; the second batch plans full implementation in 2028, including Singapore, the UAE, and Hong Kong SAR.

According to the system schedule, the collection of relevant transaction data will begin one year in advance. Starting from 2026, crypto asset service providers are required to systematically organize reportable transaction information.

Figure 1: Overview of CARF Implementation Progress in Major Jurisdictions

Hong Kong SAR: Clear Participation and Progress According to Schedule

In the above arrangement, Hong Kong SAR has explicitly committed to implementing CARF and will advance related work according to the international timetable.

Hong Kong plans to start collecting crypto asset transaction data from 2027 and to conduct automatic cross-border tax information exchange with other participating jurisdictions in 2028.

Crypto asset service providers operating under Hong Kong’s regulatory framework are required to establish corresponding data compliance and reporting mechanisms. Relevant reportable transactions will be included in the cross-border information exchange process.

Mainland China: No Commitment and Not Within Implementation Scope

In contrast, Mainland China has not yet committed to implementing CARF.

As of now, Mainland China has not been included in any of the CARF implementation batches, nor has it been listed by the OECD as a jurisdiction that is relevant but has not yet committed to participation.

Under the current regulatory framework, Mainland China maintains strict restrictions on cryptocurrency trading activities. There are no legitimate crypto asset service providers within the country that can be included in the CARF reporting system. Therefore, in the short term, there are no institutional conditions for participating in routine CARF information exchange.

Future Possibilities and Practical Judgments

It should be noted that Mainland China has fully implemented CRS since 2018 and has mature experience in financial account information exchange.

If future regulations on crypto assets are adjusted, Mainland China would have the conditions at the institutional and technical levels to connect with CARF.

However, given the current policy environment, the likelihood of Mainland China joining the framework in 2027 or in the subsequent years remains low.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.