Author: CoinFound

Stablecoins are transitioning from trading tools to global financial infrastructure.

For a long time, market perception of stablecoins mainly focused on their role as “cryptocurrency trading media”: used for exchange quoting, on-chain hedging tools, or as foundational liquidity assets within DeFi systems. But after 2026, this narrative is rapidly being rewritten. The functional boundaries of stablecoins have extended from “trading auxiliary assets” to payments, settlements, collateralization, yield generation, cross-border clearing, and even RWA settlement layers—gradually evolving into key infrastructure in the global digital financial system.

CoinFound’s latest research, “Stablecoin Ecosystem Map — From Trading Tools to Global Financial Infrastructure,” indicates that the stablecoin market is entering a new phase characterized by “high mainstream adoption and institutionalization.” Its significance no longer lies solely in price stability or on-chain circulation efficiency, but in becoming an essential bridge connecting traditional finance and decentralized ecosystems through programmability, global settlement capabilities, and multi-chain liquidity networks.

The Stablecoin Market Has Entered a Trillion-Dollar Normalized Cycle

By 2026, the total market cap of global stablecoins has surpassed $310 billion, with annual trading volume reaching $33 trillion. This figure alone demonstrates that stablecoins’ practical applications have long gone beyond internal turnover within crypto exchanges, extending into broader real economy sectors and global fund clearing networks.

From an evolutionary perspective, stablecoins are no longer just “dollar substitutes” on the chain; they are undertaking deeper infrastructural roles:

They serve as carriers for cross-border value transfer, underpin liquidity in DeFi and RWA systems, and are gradually embedded into payment gateways, corporate treasury management systems, and backend clearing structures of social networks.

Particularly noteworthy is the rapid growth in Asian markets. Stablecoin market cap on BNB Chain grew by 133% year-over-year in the past year. This trend indicates that the stablecoin ecosystem is not only deepening integration within Western financial systems but also forming new regional payment and clearing networks across Asia.

Three Major Macro Drivers Accelerate Stablecoin Expansion

The underlying logic driving the rapid upgrade of the stablecoin ecosystem mainly stems from three factors:

First, regulatory clarity.

Major jurisdictions worldwide are gradually establishing compliance frameworks for stablecoins. Clear regulations reduce policy uncertainty and create preconditions for large-scale institutional capital entry. Historically, many traditional financial institutions were cautious about stablecoins—not due to doubts about efficiency, but because of the lack of legal clarity. Now, these barriers are being progressively removed.

Second, continuous inflow of institutional capital.

As regulatory boundaries become clearer, VC firms, asset managers, and traditional financial companies are increasing investments in stablecoins and related payment infrastructure. According to data, this sector has already attracted $7.9 billion in institutional funding, with a CAGR of 44% for VC investments. This indicates that the stablecoin space is no longer just a playground for crypto-native startups but is becoming a core focus for traditional capital allocation.

Third, geopolitical economy and global clearing demands.

Complex international environments, cross-border payment frictions, and the normalization of traditional financial sanctions have objectively increased demand for alternative clearing networks. Stablecoins, with their borderless liquidity and 24/7 settlement capabilities, have natural advantages in this trend. Capital migration in extreme scenarios further validates stablecoins’ role as a global liquidity network.

Global Regulatory Frameworks Are Reshaping Industry Boundaries

By 2026, the regulatory environment for stablecoins is shifting from pilot programs to systematic implementation.

In the U.S., a federal framework is taking shape, focusing on 1:1 high-liquidity reserve assets, strict audits, and inclusion under national banking supervision. Meanwhile, debates over whether “yield-bearing stablecoins should pay interest” have become a critical industry dividing line.

This controversy essentially reflects whether stablecoins should be regarded as “payment tools” or evolve into “shadow deposits” and similar deposit-like financial products.

The EU’s MiCA regulation has been fully implemented, imposing strict requirements on reserve segregation, whitepaper disclosures, and interest payments, reflecting a highly cautious regulatory approach.

Hong Kong is accelerating the development of a local stablecoin licensing system, emphasizing local registration, 100% backing by cash or US Treasuries, aiming to seize the institutional high ground in RWA and digital finance hubs across Asia.

The UK is also pushing for regulation of “systemically important stablecoins,” integrating them into the traditional financial services legislation.

This means the global stablecoin ecosystem is no longer in a “regulatory vacuum” but is forming a clear policy map.

This map boosts institutional confidence and also raises the bar for yield-bearing stablecoins, DeFi protocols, and RWA products. Future competition will not only be about technology and scale but also about compliance, product isolation, and policy adaptability.

Market Structure Divergence: USDT and USDC Continue to Lead, Yield and RWA Rapidly Rise

In terms of competitive landscape, the stablecoin market shows clear concentration and structural differentiation.

Tether (USDT) remains dominant, holding about 58% market share, with deep liquidity in offshore trade and emerging markets.

Circle (USDC), leveraging its compliance image, institutional channels, and Ethereum ecosystem advantages, continues to increase its share in regulated markets, gaining about 7%.

Meanwhile, competition among issuers is shifting from “whose stablecoin is bigger” to capital efficiency, yield potential, and collateral structure:

- Tether is challenging institutional markets with more compliant product architectures;

- Circle is expanding beyond USDC into yield-generating and tokenized fund products to attract institutions;

- BlackRock’s BUIDL and other tokenized government bond products are becoming key collateral assets for DeFi protocols and stablecoin yield strategies.

This evolution indicates that stablecoin competition has shifted from “payment tool” to “financial infrastructure.” Those offering higher capital efficiency, stronger compliance, and deeper institutional integration will have greater chances to lead the next phase of ecosystem development.

Subsector Acceleration: Payments, DeFi, Institutional Clearing, RWA

From application deployment, the stablecoin ecosystem currently exhibits several prominent growth directions:

1. Cross-border Payments and Remittances

Still among the most practical use cases, especially in B2B scenarios.

Stablecoins have become vital tools for restructuring cross-border payment efficiency. Compared to traditional multi-layered banking and clearing, stablecoins excel in low-cost, 24/7 settlement across time zones.

2. DeFi Lending and Yield Generation

Stablecoins have evolved into benchmark rate assets within DeFi.

The rise of yield-bearing stablecoins transforms them from mere hedging assets into capital management tools with both payment and income functions. This shift is a key driver of recent rapid market growth.

3. Institutional Settlement and Backend Clearing

Traditional payment networks are gradually integrating blockchain-based backend systems.

Stablecoins are infiltrating institutional settlement, increasingly becoming the “invisible clearing layer” behind conventional payment systems.

4. RWA Tokenization and Underlying Liquidity Integration

RWA (Real-World Assets) is one of the most promising long-term trends.

As traditional financial assets are tokenized, stablecoins or similar yield products will increasingly serve as cash legs and collateral in transactions.

The combination of stablecoins and RWA is expanding on-chain financial activity from speculative trading to more authentic, large-scale traditional capital markets.

Risks Remain, but Market Shows Resilience

Despite the maturing of the stablecoin market, underlying risks have not disappeared.

The report categorizes risks into three main types:

- Operational and technical risks: smart contract vulnerabilities, cross-chain bridge attacks remain major concerns

- Market and liquidity risks: DeFi leverage models and collateral asset volatility could trigger de-pegging pressures

- Geopolitical and regulatory risks: offshore stablecoin networks’ use in global capital flows may further trigger AML and compliance crackdowns

Additionally, yield restrictions pose new compliance challenges for DeFi protocols; scaling RWA depends heavily on legal frameworks for offline verification and bankruptcy separation.

However, the market has not lost resilience due to these risks. On the contrary, after phases of volatility, the stablecoin ecosystem demonstrates strong self-healing capacity. Short-term deleveraging and sentiment shocks are followed by capital reflows, indicating that the market’s long-term view of stablecoin infrastructure remains intact.

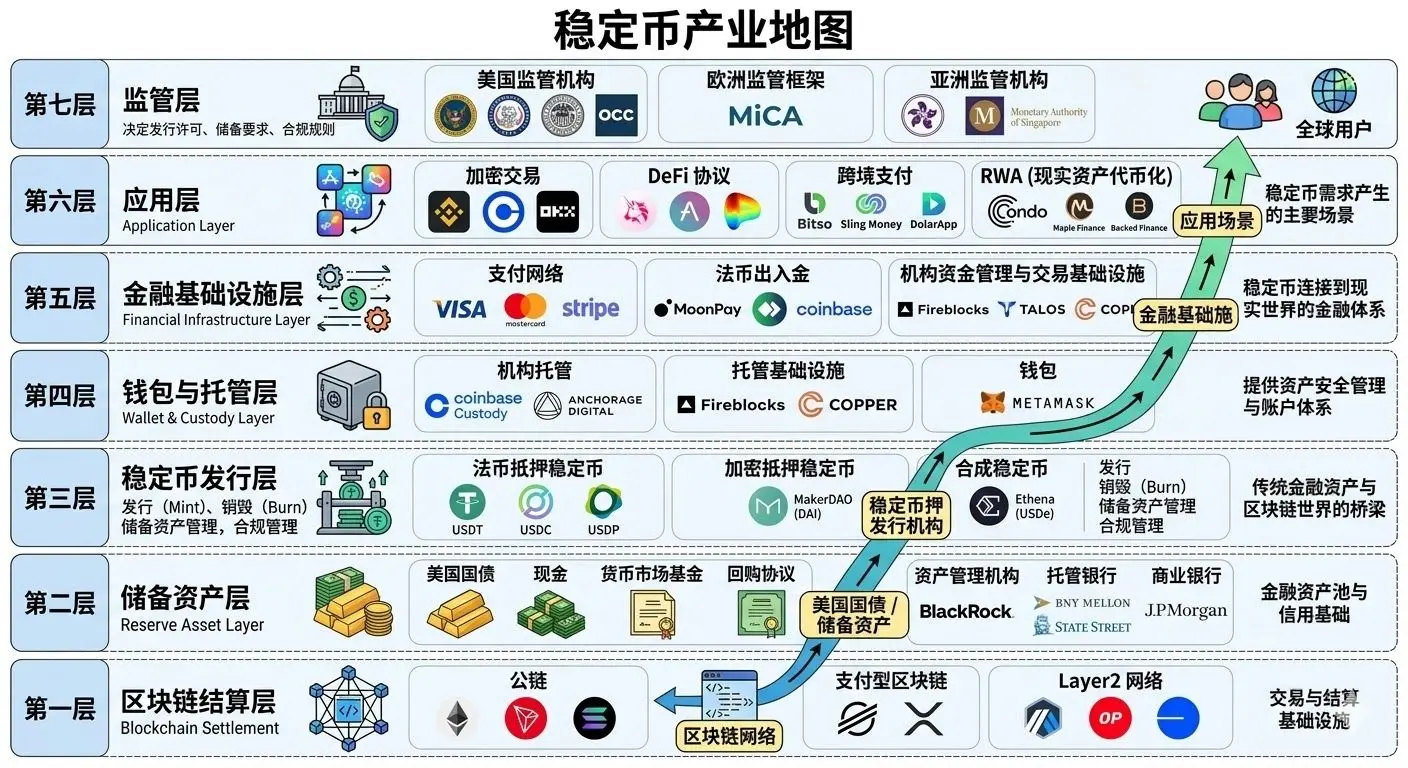

Stablecoins Are Building a Full-Chain Closed-Loop Ecosystem

From an industry chain perspective, stablecoins are no longer isolated assets but have formed a complete closed loop:

- Upstream: reserves, government bonds, regulated RWAs

- Midstream: issuance, custody, cross-chain routing, multi-chain liquidity networks

- Downstream: payments, settlements, DeFi, RWA, social payments, AI-driven scenarios

This full-chain ecosystem signifies that stablecoins are evolving from a single financial product into a scalable, composable, embedded global value transfer network.

Future key innovation directions include:

- Stablecoin payment integration within social platforms

- Regionally anchored compliant stablecoins linked to local fiat

- AI agent-driven machine-to-machine payments

- Lower-threshold fiat on-ramps and account abstraction technologies

These trends suggest that the future of stablecoins is not just “more holders” but “more systems adopting them as the default payment and settlement layer.”

Conclusion: From On-Chain USD to Global Financial Rails

The stablecoin industry is undergoing a fundamental identity shift.

It is no longer merely a convenient tool within the crypto market but is evolving into a comprehensive global financial infrastructure covering payments, clearing, yield, collateral, and asset settlement.

From regulatory clarity and institutional entry; from the consolidation of leading players to the rise of RWA and yield products; from expanding payment scenarios to integration with social networks and AI protocols— the next phase of stablecoin development will be less about isolated breakthroughs and more about systemic evolution.

For investors, fintech firms, policymakers, and Web3 builders, understanding stablecoins is no longer just about grasping a niche but about comprehending the foundational architecture of future digital finance.