Related to the Trump family, the DeFi project World Liberty Financial Inc. (WLFI) is pushing a governance proposal that requires investors holding unvested tokens to stake their tokens for at least 180 days in order to retain voting rights, in exchange for a 2% annual yield. Voting began on March 5 and ended on March 13. By the weekend, over 99% of participating voters supported the proposal, but the actual amount of tokens voting accounts for only 1% of the total supply.

Core Terms of the Governance Proposal: Voting and Liquidity Trade-offs

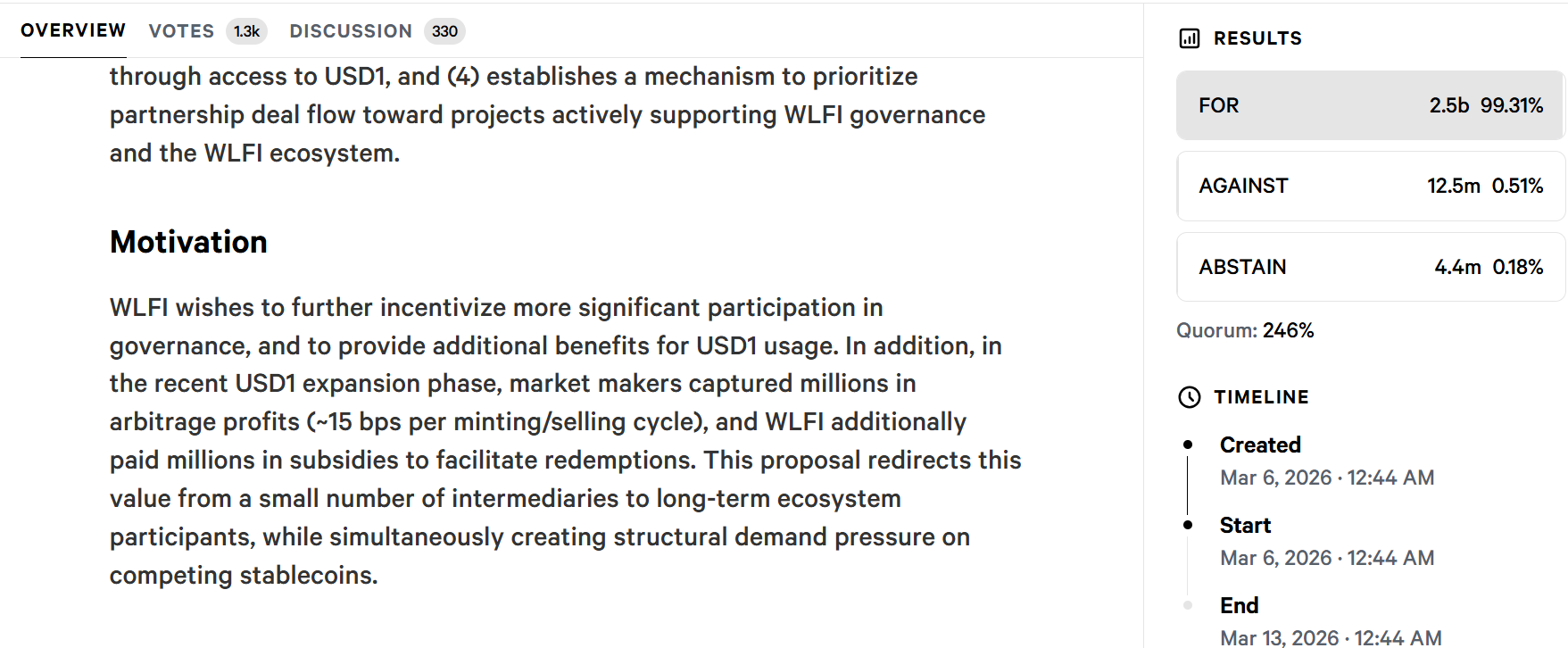

(Source: WLFI)

WLFI’s current token distribution presents investors with a specific dilemma:

- 80% Locked: No unlock schedule, no liquidity, and not directly affected by this proposal’s new rules.

- 20% Freely Tradable: The only portion investors can currently liquidate, and the target of this proposal’s regulation.

Trade-off: If investors want to retain governance voting rights, they must stake this 20% of liquid tokens for 180 days; choosing to keep flexibility means losing voting rights.

These governance decisions include when to release the locked 80% holdings—meaning if investors want a say in when their assets unlock, they must actively give up the only liquidity they have. WLFI raised over $550 million between October 2024 and March 2025, with early investors paying between $0.05 and $0.15 per token; the current trading price is about $0.099, down over 50% since some tokens became tradable.

Controversy Over Dual-Layer Governance: Whales’ Privileges and Transparency Concerns

The proposal includes a special clause: investors holding at least 50 million WLFI can directly negotiate with the project team. Critics argue this creates a two-tier governance structure favoring large institutional investors and disadvantaging ordinary retail investors.

Lex Sokolin, Managing Partner at Generative Ventures, pointed out transparency issues: “It’s unusual that the project doesn’t provide an unlock schedule; these figures are usually set at token issuance. This is one of the most critical areas where transparency should be maintained.”

Token holder Morten Christensen (AirdropAlert operator) plans to vote against, stating: “For WLFI, investors are completely investing blindly.” He also noted that staking mechanisms often involve participants buying an equivalent amount of tokens while staking, which can perpetuate selling pressure.

Andrei Grachev, Managing Partner at DWF Labs, confirmed that the company bought $25 million worth of WLFI tokens last year and currently holds them but has no plans to increase holdings before liquidity is available: “These tokens are locked. Until they gain liquidity, we have no plans for further investment.”

Project’s Long-Term Vision and the Trust Gap with Investors

On March 5, the project defended the proposal, stating governance decisions should reflect participants aligned with the ecosystem’s long-term direction, not short-term traders. Some supporters highlight WLFI’s ambitious long-term plans: applying for a U.S. national bank license, building cross-chain infrastructure, and launching a real-time lending market.

However, whether these visions can bridge the trust gap caused by the missing unlock schedule remains a key market focus. The project was supposed to publish an unlock schedule by March 12, which has become a critical deadline for assessing the future direction of this governance event.

Frequently Asked Questions

Q: What specific requirements does WLFI’s governance proposal impose on investors?

A: Investors holding unvested WLFI tokens must stake them for at least 180 days to retain voting rights, earning a 2% annual yield (calculated in WLFI tokens). Those who do not stake will lose voting rights. Only 20% of holdings are freely tradable, making them the only liquid assets.

Q: Why has the lack of an unlock schedule for WLFI tokens attracted criticism?

A: Lex Sokolin pointed out that tokenized projects usually publish complete unlock schedules at issuance, which are critical for assessing liquidity risk. WLFI has not disclosed plans for unlocking the 80% locked tokens, forcing investors to make governance decisions without understanding exit risks, which is seen as a serious transparency issue.

Q: How is the voting participation rate in the WLFI governance proposal, and what about representation concerns?

A: Although over 99% of voters support the proposal, the actual token amount voting is only about 1% of the total supply of approximately 10 billion tokens. This indicates extremely low overall participation, and the majority of “support” reflects the stance of a small, active voting minority rather than broad holder consensus.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.