In January 2026, the native token RIVER from the chain abstraction stablecoin system River saw an extreme inverted V-shaped price movement within just four weeks. The price soared from around $2 at the end of December 2025 to a record high above $87, a surge of over 2,700%. Then, within only six days, it rapidly fell back to nearly $11, marking an 87% decline.

This extraordinary volatility has drawn intense scrutiny from industry watchers and on-chain analytics firms. After third-party data providers like Bubblemaps released key evidence on January 27, suspicions have grown around RIVER token price manipulation, heavy early-stage token concentration, and profits realized by related addresses.

Secures $12 Million in New Funding, Backed by Arthur Hayes

The River project, developed by the RiverdotInc team, is positioned as a chain abstraction stablecoin system for the multi-chain ecosystem. The system is designed to connect assets, liquidity, and yields across different blockchains, enabling seamless cross-chain interaction without relying on traditional bridges or wrapping mechanisms.

On January 6, BitMEX founder Arthur Hayes publicly urged CEXs to list the token and predicted a breakout. Hayes’s endorsement gave RIVER its first major boost. While most mainstream crypto assets were trending down at the time, RIVER began a unilateral rally, with its market cap more than quadrupling within a few weeks.

On January 23, River announced the completion of a $12 million strategic funding round. In addition to previously reported investors Justin Sun and TRON DAO, this round included Maelstrom Fund (founded by Arthur Hayes), The Spartan Group, and Nasdaq-listed companies and institutions from the US and Europe.

According to official statements, the funds will support River’s expansion in both EVM and non-EVM ecosystems (including TRON, Sui, and major EVM networks), and the ongoing development of on-chain liquidity infrastructure. The capital will accelerate ecosystem deployment, deepen stablecoin liquidity, and promote the integration of satUSD in trading, lending, staking, and yield scenarios. River will also launch yield products Smart Vault and Prime Vault, providing users and institutions with a unified interface for accessing cross-ecosystem yields through protocol-native and institutional-grade strategies.

Notably, just two days after the large funding announcement, RIVER’s price hit its peak and began to decline.

Funding Rate-Driven Price Manipulation Patterns

CoinGlass previously used RIVER as a case study to illustrate how funding rates, combined with leverage structures, can drive price volatility. They emphasized that this pattern has appeared in several tokens over the past two years, with RIVER being just one example. CoinGlass noted that many traders misunderstand funding rates: funding rates do not predict direction, but rather indicate the imbalance between long and short positions and which side of the market is more crowded.

Step 1: Suppress price while pushing funding rates deeply negative. Prices are kept low or suppressed, and funding rates are driven into a sharply negative range. As a result, short positions become highly concentrated, and a market consensus develops that a negative funding rate signals a coming rebound.

Step 2: Induce some traders to go long. When funding rates are deeply negative, some traders open long positions, expecting a rebound and hoping to receive funding payments. CoinGlass describes this expectation as part of the trap.

Step 3: Price may be pushed up even during negative funding rate phases. CoinGlass’s key point is that when funding rates are extremely negative, the price does not need to reverse trend. The market only needs a controlled upward push to trigger a cascade among shorts, including liquidations, stop-losses, and forced buybacks.

Why do rallies occur while funding rates remain negative? Many sharp rallies start when funding rates are still negative. The upward move is driven by the unwinding of leveraged positions, and passive buying amplifies the gains. Once crowded shorts are cleared out, funding rates quickly return to neutral. Some traders view this normalization as a sign of market health.

CoinGlass warns that this is actually just a “reset” of the trap. Operators can repeatedly execute the cycle of “creating extreme rates, attracting consensus positions, forced liquidations, and resetting.”

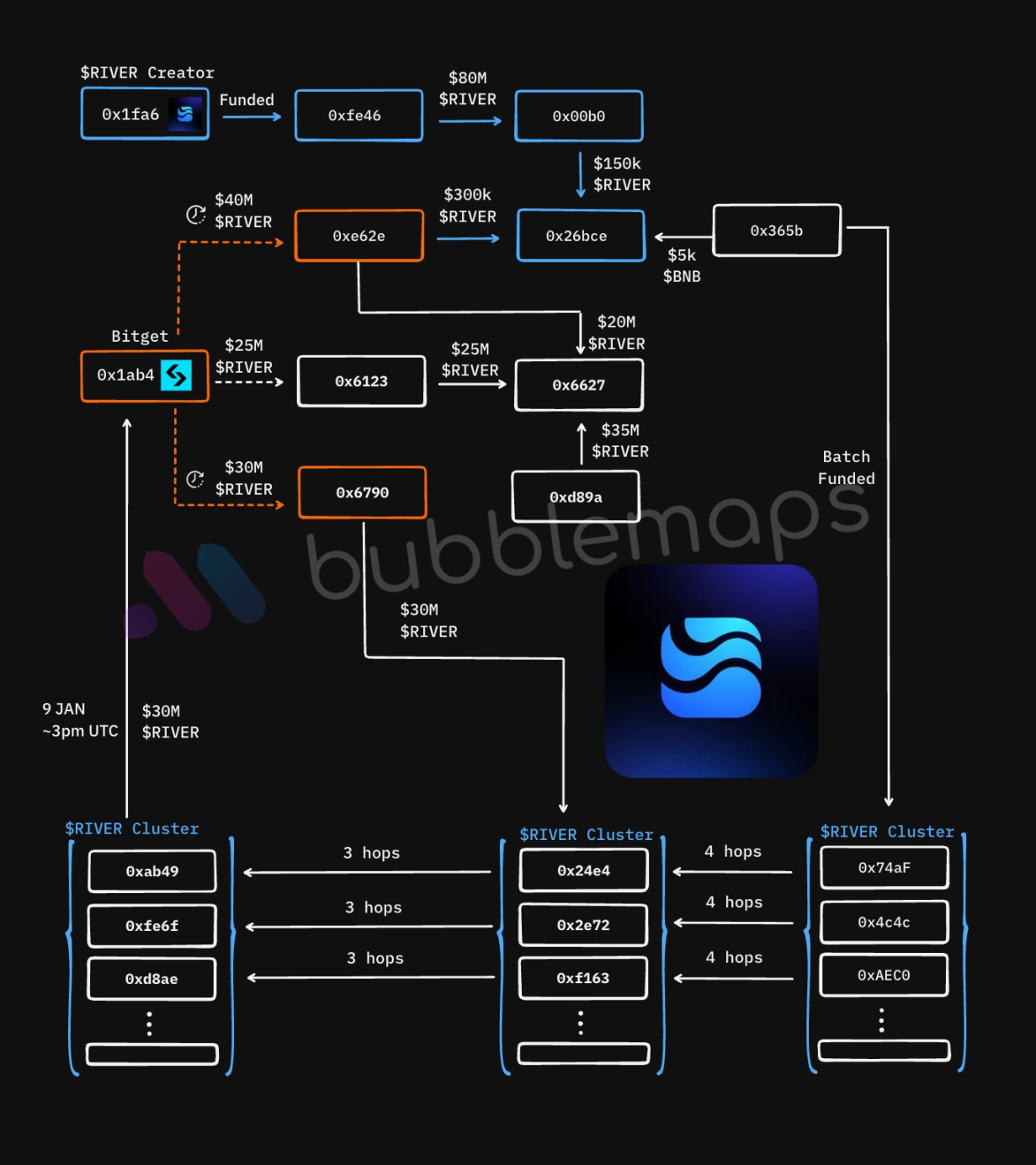

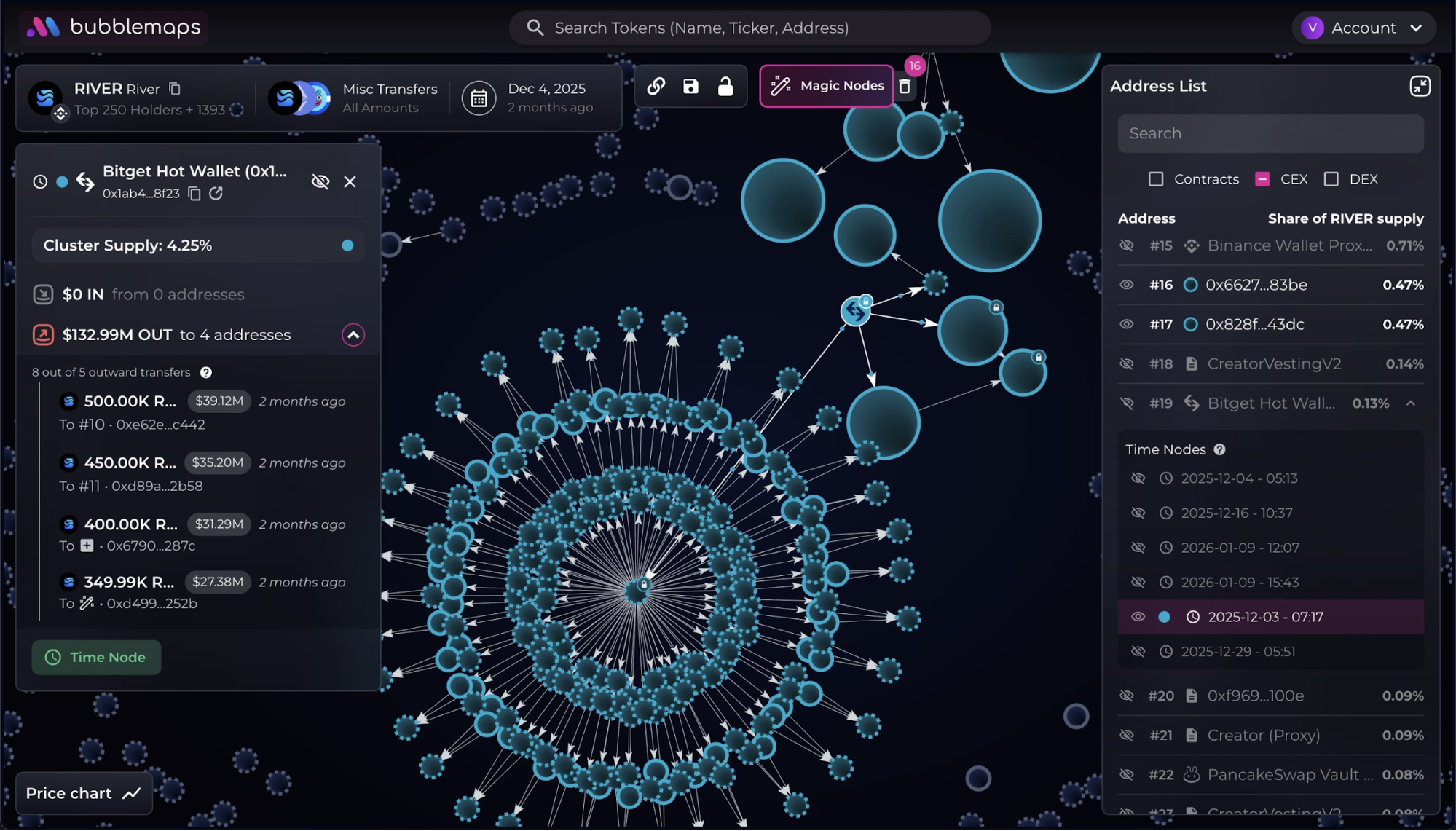

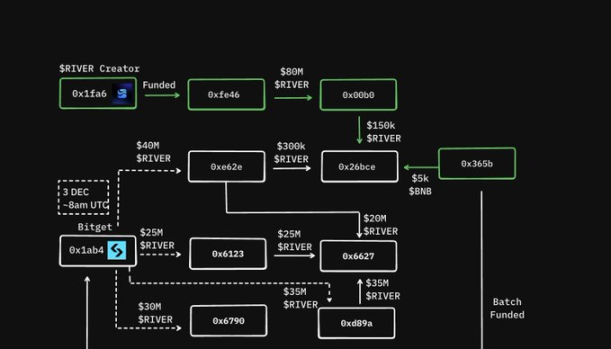

Analysis: RIVER Creator Suspected of Direct Ties to Major Address Cluster, Realizing $10 Million in Profits from RIVER Sales

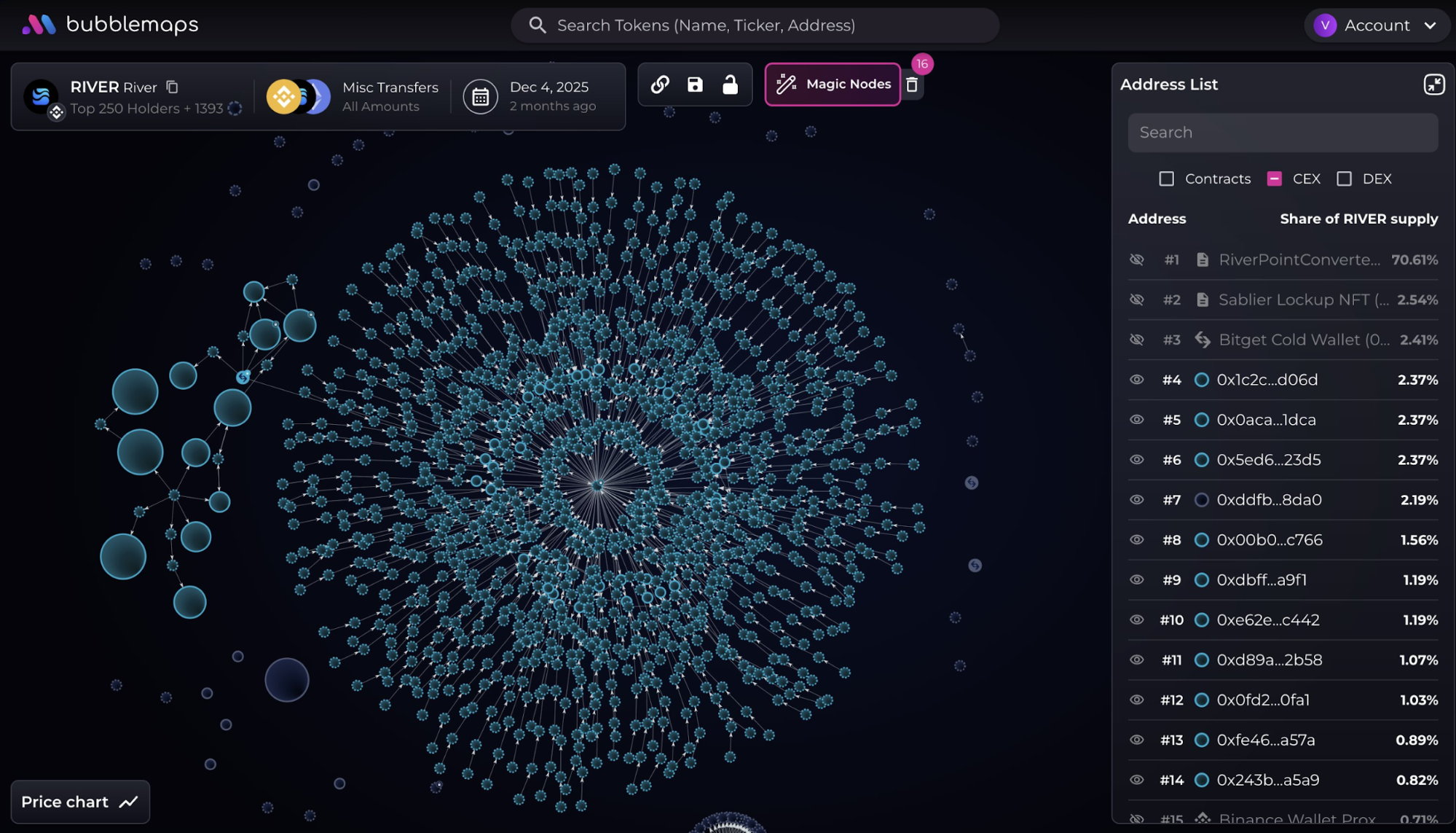

According to Bubblemaps, a massive cluster of over 2,000 wallet addresses is directly related to RIVER.

They found that one month after RIVER’s launch, seven addresses withdrew 230 million RIVER tokens from Bitget. These wallets had no prior activity and received tokens during a tight window on December 3 and 29.

One of these wallets, 0x6790, distributed 400,000 RIVER tokens across hundreds of wallets. All of these recipient wallets showed similar patterns: no prior activity, received similar amounts of RIVER, sent tokens to Bitget on January 9 (likely to sell), were funded from a single source, and involved four layers of transfers.

Bubblemaps noted that the wallet address funding this cluster, 0x365b, is directly connected to the RIVER creator. The wallet 0x6790, which distributed RIVER to the cluster, also shows links to the RIVER creator. Bubblemaps estimates the cluster’s profits at $10 million.

What is clear for now is that RIVER experienced a dramatic repricing—from a rapid surge to a swift correction—in a very short period. Market focus has shifted from narrative and growth expectations to concerns about token distribution and fund flow anomalies. The address cluster and associated clues revealed by Bubblemaps have heightened doubts about early token concentration, profits by related addresses, and exchange-based selling. CoinGlass’s discussion of funding rates and position crowding offers another explanatory framework, suggesting that derivatives structures may have amplified the price swings.

The RIVER case is a reminder that tokens with low float and high elasticity are prone to extreme movements when sentiment and structural factors align. When negative signals appear in token distribution and trading structure, price corrections tend to be faster and deeper.

Disclaimer:

- This article is republished from [Foresight News]. Copyright belongs to the original author [ChandlerZ]. For any objections regarding this republication, please contact the Gate Learn team. The team will respond promptly in accordance with relevant procedures.

- Disclaimer: The views and opinions expressed in this article are solely those of the author and do not constitute investment advice.

- Other language versions of this article are translated by the Gate Learn team. Unless Gate is mentioned, reproduction, distribution, or plagiarism of the translated article is not permitted.