Editor’s Note: This article was originally published on January 17, 2020—six years ago. Today, the market is focused on the likely appointment of Kevin Warsh, an ultra-hawkish Federal Reserve Chair. Warsh, handpicked by Trump, has become the target of widespread criticism, with the historic collapse in gold and silver prices largely attributed to him. Other markets are also pricing in uncertainty, and, simply put, there are currently no assets on earth experiencing upward momentum.

In researching Kevin Warsh, it was discovered that he is a protégé of Stanley Druckenmiller and previously worked as a partner at Druckenmiller’s family office. Their relationship is notably close. Druckenmiller himself is the famed protégé of George Soros, having orchestrated the legendary 1992 “attack on the British pound.”

This round of crashes in precious metals and Bitcoin is certainly not Soros’s doing, but it brings to mind a BlockBeats article from January 2020: “If Soros Wanted to Destroy Bitcoin, How Would He Do It?” At that time, Bitcoin had climbed back above $10,000, and the market was optimistic about the upcoming halving. There was hope that the halving would propel Bitcoin to a new all-time high above $20,000.

Looking back, many of the article’s predictions from six years ago have materialized: Bitcoin reached $100,000, the concept of interstellar currency emerged, the majority of mining power shifted to the US, and crypto banks have all but disappeared.

The original intent of the article was to temper excessive optimism. We’re republishing this six-year-old piece as Soros’s protégé steps into the spotlight and Bitcoin has become a multi-trillion-dollar commodity. Even silver, a massive asset, was halved in just two days—making such an outcome for Bitcoin even more plausible. We have skin in the game, but we must always respect the market. The following is the original text:

It’s been a decade of prosperity and celebration.

Few have seriously considered whether Bitcoin could one day experience a true collapse, or what that might look like. The perpetual bulls waving the eternal rally banner have never entertained the thought, and the bears, lacking nuanced analysis, have not examined it in detail either.

The purpose of this BlockBeats article is not to simply take a bullish or bearish stance on Bitcoin, but to explore an interesting and serious question: What inevitable crises will Bitcoin face despite its seemingly bright prospects? If so many capital forces are skeptical about Bitcoin, why haven’t they gone all-in on shorting? And if the likes of Soros ever do enter the market, how might they operate?

Let’s imagine a scenario that could unfold 4N years from now.

Bitcoin’s price hovers around $50,000, and its market capitalization finally crosses the trillion-dollar mark.

The market’s perception of Bitcoin has converged on “digital gold” and a store of value. With some developing countries declaring Bitcoin as a reserve asset and Musk’s rockets rolling off the assembly line, Bitcoin advocates’ slogans become even more compelling—Bitcoin is the new century’s reserve currency and the 22nd century’s interstellar money.

Those who once doubted Bitcoin—whether rational investors or impulsive bystanders—are now mocked by every holder as people who “don’t understand the times.”

What times are these? An era when Western economies require asset hedges, some countries face hyperinflation and need stores of value, geopolitical tensions drive demand for safe havens, and buying in means instant profit.

It seems everything is settled, with no room for reversal.

Beneath the surface of prosperity, crisis is everywhere.

Miners are content, using advanced equipment and financial tools to calculate daily and monthly earnings. They skillfully use forward contracts for hedging, and some accumulate Bitcoin, hoping for the day it hits $1 million per coin.

Investors are happy as well—never before has an asset grown so quickly and consistently. The Bitcoin derivatives market has developed rapidly, with speculators leveraging futures and options to capitalize on volatility. No other asset class offers such opportunity.

The most satisfied are those controlling capital upstream in the industry. Some earn tens of millions daily from traders’ short-term battles, while others profit from the growing demand for industry loans. By now, the Bitcoin market is nearing maturity; compared to mining and trading in 2020, diversified products have become the entry point for the masses.

The allure of easy money is intoxicating, and no one notices that industry metrics are heading toward disaster. After all, the bears are considered “fools”—at least, they didn’t make money.

By then, miner loans and installment purchases of mining rigs have become the norm. Paying in full is seen as foolish for not using leverage.

At this stage, the global Bitcoin mining industry’s overall debt ratio has surpassed 70%, meaning most miners are borrowing and mining with leverage. As long as the loan interest rate is below mining yields, it’s a profitable business.

Soros arrives—the sniper wielding international capital steps onto the stage.

Soros first acquires X billion dollars’ worth of Bitcoin in the spot market. Not only does Soros enter, but more “Soros types” join him—his allies in international capital, various investment funds supporting the long side. This coincides with the Nth Bitcoin halving hype, driving a surge of buy orders. Blockchain investment institutions and media cheer: “The institutional money is here! Let’s embrace the Bitcoin era!”

After building spot positions and as market sentiment peaks, Soros increases his long positions in near-month Bitcoin futures.

Following a major rally, derivatives market bulls charge in en masse, while bears dwindle. The only force that can stop the bulls seems to be their own profit-taking.

With substantial paper gains, Soros secretly instructs his assistant to take a new step—buying out-of-the-money long-dated put options.

By then, options trading is as popular and mature as spot trading was in 2020, with much higher liquidity. Soros’s accumulation is effortless.

No one believes Bitcoin will fall below $20,000 again. Bitcoin has always moved in a spiral upward. And now, thanks to Soros’s spot buying, it’s nearly $100,000. Option sellers happily issue puts with $20,000 strike prices, counting the risk-free premiums they’ll earn in the coming year.

They don’t realize that Soros is the counterparty buying those out-of-the-money puts, and options are his chosen path for this hunt. When you stare into the abyss, the abyss stares back at you.

After Bitcoin officially breaks $100,000, Twitter erupts.

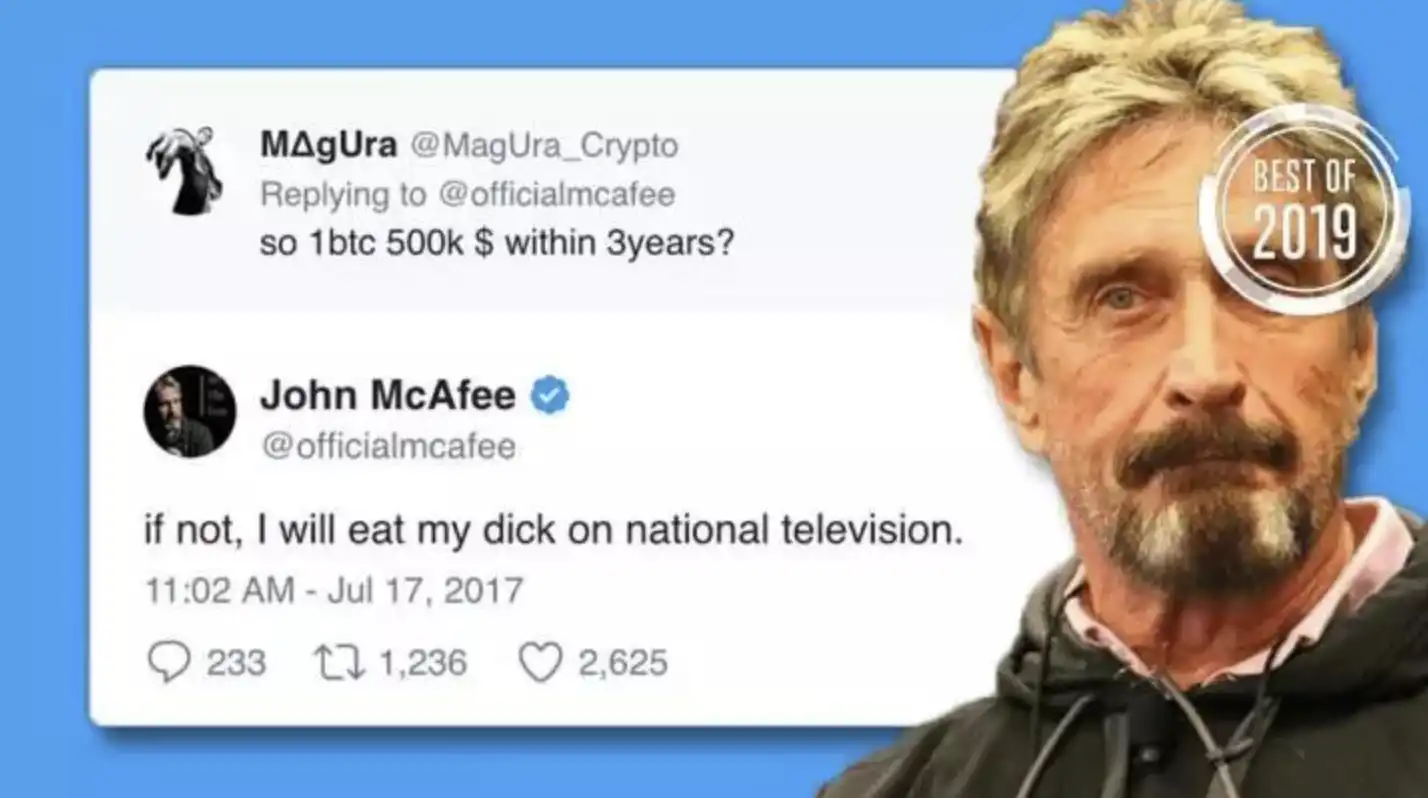

McAfee reiterates his $500,000 prediction was not a joke but his true belief. Musk says whether Bitcoin is a “safe word” no longer matters; what matters is that space travel will only accept Bitcoin payments. Renowned trader K shares his overnight riches from going long Bitcoin on a forum, while miner B sees mining rig prices soar and increases leverage—“keep going!”

Now, Soros is ready to strike. He secretly instructs his assistant to start shorting long-dated Bitcoin futures. With the market in a strong bull trend, the first batch of short positions is quickly assembled. Soros then pauses, watching how things unfold.

To replicate his legendary shorting of the pound and Thai baht, Soros knows this is just the beginning.

By then, 80% of Bitcoin mining rigs have moved to Country M, with most hash power concentrated in State N. Soros contacts local officials in State N, explaining his views on Bitcoin’s overheated valuation, distorted mining leverage, and his intent to short Bitcoin. He mentions that he’s assembled famous international capital P, and the strategy is nearly foolproof. If the officials provide “news support,” Soros will share 10% of the profits after success.

To obtain precise data on circulating Bitcoin and its distribution, Soros analyzes blockchain explorer data and realizes he must access the trading platform “black box.” He approaches the head of the largest exchange H in Country M. Soros tells him that ten years of trading fees can’t compare to joining this operation, and that famous capital P and State N officials are already part of the short alliance. He says that knowing the liquidation levels of H’s major futures longs and their margin balances will allow for precise attacks with less capital, promising to share all saved costs with the H executive after success.

Soros knows the market is a dangerously high tower, and he will be the spark, but more institutions are needed to add fuel to the fire.

He then contacts the aforementioned capital P, explaining his short logic in detail: Mining is Bitcoin’s primary market, but the industry is now chaotic—a sign of decline. Lending companies no longer rigorously vet client credit; instead, they lend freely for quick profits. Miners use loans to buy more rigs, using those rigs to obtain more loans. Data shows industry debt far exceeds 70%. Some sharp cloud mining firms are selling 100 years of future hash power.

Meanwhile, retail investors’ hedging needs in the secondary market have spawned Bitcoin price insurance products. Crypto financial firms no longer prioritize risk management, but simply act as option sellers, happily collecting “rent” again and again.

Soros smirks, excited as if he’s about to capture his prey, and continues: “Bitcoin’s mining cost is $85,000; the current price is $110,000. With the halving, block rewards will plummet. If we crash the price below $70,000, we’ll trigger a death spiral in highly leveraged mining. The bulls will become our most dazzling fuel, and their cascading liquidations will leave option sellers helpless. Shorting Bitcoin is politically correct—whether stocks or commodities, force majeure could block our plans, but Bitcoin’s capital game is the perfect slaughterhouse.”

Seeing some hesitation, Soros adds: “To guarantee success, I’ve already secured State N officials and the H exchange head. We’re covered for both news and data—failure is impossible. The position strategies are set; just waiting for you to join.” The capital P executive nods.

The curtain rises.

On December 24 of (2020+4N), Soros decides to strike hard on Christmas Eve, when everyone’s guard is down.

That night, Soros suddenly dumps 10X billion dollars in Bitcoin short positions across long-dated contracts, sending Bitcoin plunging from a high of $120,000. With H’s position data in hand, Soros executes precisely at each level, triggering a cascade of bull liquidations. The price crashes to around $95,000 at its lowest.

The next day, as some brave spot buyers rush in, Soros begins offloading the X billion dollars of spot Bitcoin he previously acquired. The crypto world stays up all Christmas night, as institutions and media rush to report Soros’s Bitcoin sell-off and suspected shorting.

On December 26, bearish sentiment spreads, capital P increases short positions, and panic grips the market. Soros immediately contacts State N officials in Country M, who issue a notice to investigate illegal Bitcoin electricity use and a “State N Initiative to Resist Bitcoin Speculation,” urging Country M’s parliament to address Bitcoin’s excessive speculation and power waste. Bitcoin inevitably falls to $75,000.

On December 27, Soros’s original long Bitcoin futures positions enter physical delivery, allowing him to acquire $5X billion worth of Bitcoin spot at $7.5 each.

On December 28, Soros dumps the newly acquired spot Bitcoin, sending the market into the abyss. “Bitcoin Ponzi scheme” and “blockchain scam” trend on Twitter.

McAfee tweets again, saying his $500,000 prediction was clearly a joke and shouldn’t be taken seriously. Musk says Bitcoin’s price volatility makes it unsuitable for interstellar travel payments. Trader K posts “Goodbye!” on the forum and disappears. As for miner B? No one knows where he went. Bitcoin has long since fallen below $40,000; mining rig prices have collapsed, mining is unprofitable, and he can’t repay huge loans. For his wife and children, he vanishes, living incognito.

On December 29, dubbed Bitcoin’s Black Friday by history, bulls are routed and the industry chain collapses like dominoes. Bitcoin falls below $20,000. The largest “bank” Q in the crypto world declares bankruptcy, unable to repay users or policyholders. The largest mining rig manufacturer S in Country M permanently halts mining business and pivots to developing chips for space travel machines.

Amid market wailing, Soros’s early out-of-the-money puts become in-the-money options. That night, he earns $500X billion.

This story could never happen, because…

Many readers’ first reaction after reading BlockBeats’ story above will be just that.

Indeed, the numbers in the story are exaggerated, but the macro logic holds up—or rather, current conditions do not support it, but that doesn’t mean they never will.

The reason Soros and others don’t operate this way now is, first, Bitcoin’s circulating supply isn’t large enough to satisfy the sharks, and second, mining leverage isn’t high enough and derivatives markets lack sufficient liquidity. Today’s leading crypto firms still have principles and original intentions, but if they lose those in future rapid growth, the consequences may play out as above.

BlockBeats’ true intent in this article is not to be bearish or pessimistic, but to offer insight and warning to the industry.

Statement:

- This article is reprinted from [BlockBeats]. Copyright belongs to the original author [BlockBeats]. If you have concerns about the reprint, please contact the Gate Learn team, and the team will handle your request promptly according to established procedures.

- Disclaimer: The views and opinions expressed in this article are solely those of the author and do not constitute investment advice.

- Other language versions of this article are translated by the Gate Learn team. Unless Gate is specifically mentioned, reproduction, dissemination, or plagiarism of translated articles is strictly prohibited.