Do you recall when Hong Kong launched its own Bitcoin and Ethereum spot ETFs? Despite the initial excitement, the overall trading volume remains modest and has yet to make a significant impact on the market. On April 30, 2024—the first day of listing—the combined turnover for six virtual asset spot ETFs was under HK$100 million, a figure that would barely register in the US market. (1)

As of today, the total assets under management for the six ETFs stand at approximately $333 million, well below Bloomberg analysts’ original $1 billion target. By comparison, US Bitcoin spot ETFs have seen cumulative net inflows exceeding $56 billion and now manage nearly $90 billion in assets. Hong Kong’s ETF scale is a fraction of the US market. (2)

Still, if you conclude that Hong Kong’s virtual asset policy is merely “much ado about nothing,” you may be missing the developments happening beneath the surface.

ETF trading volume remains lackluster, but the real story of crypto in Hong Kong goes beyond ETF candlestick charts. It’s about the pace of licensing, the depth of traditional financial institutions entering the space, and the transition of RWA tokenization from sandbox environments to real-world implementation.

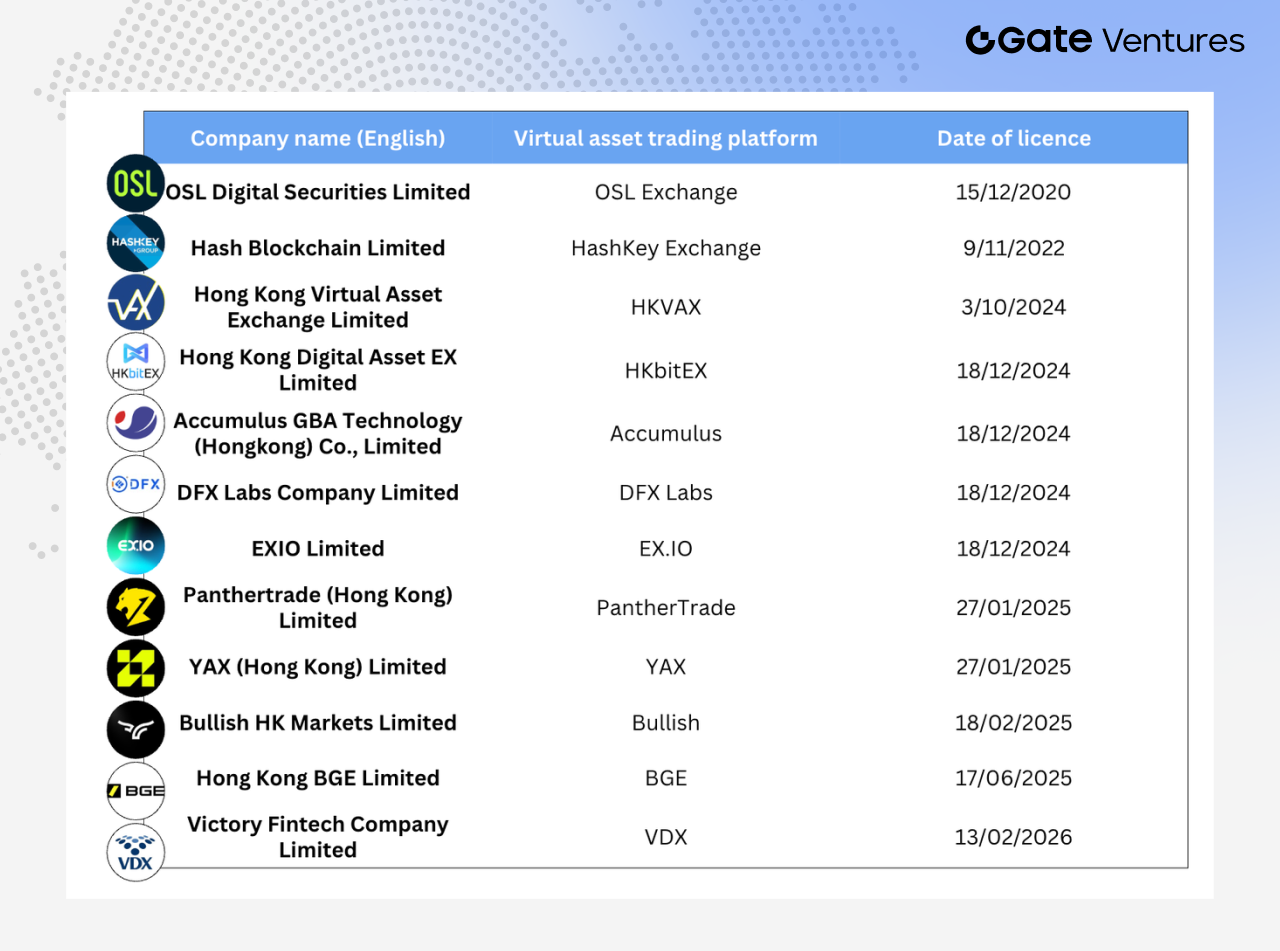

Trading Infrastructure: From 2 to 12—A Licensing Explosion

In 2023, Hong Kong’s Securities and Futures Commission (SFC) approved only two virtual asset trading platforms: OSL and HashKey. These pioneers were the sole platforms authorized to provide crypto trading services to retail clients.

By mid-2025, the number of licensed Virtual Asset Trading Platforms (VATPs) has grown to 12.

What’s even more notable is the makeup of these new entrants. Four out of twelve are affiliated with internet brokerage firms:

- PantherTrade, a wholly-owned subsidiary of Futu Securities, received its VATP license in January 2025

- YAX (Hong Kong), under Tiger International

- EXIO, invested by Huasheng Capital (Sina)

- VDX, under Victory Securities

Other players include Bullish HK Markets (the Hong Kong entity of Bullish, a crypto exchange backed by Peter Thiel), DFX Labs, and more.

From “Type 1 License Upgrade” to Dedicated VA Licenses: A Regulatory Overhaul

In the first half of 2025, traditional brokerages collectively upgraded their Type 1 licenses to enter the virtual asset sector, making headlines across the industry. Over 42 institutions were approved to offer virtual asset trading services through omnibus accounts—including Guotai Junan International, Futu Securities (Hong Kong), Interactive Brokers, and ZA Bank. In June 2025, Guotai Junan International secured a “full virtual asset license,” causing Hong Kong stocks to surge nearly 200% the day after the announcement. (3)

However, the “Type 1 license upgrade” framework essentially extends the existing Securities and Futures Ordinance (SFO) licensing system, rather than establishing a fully independent virtual asset intermediary regulatory regime. Brokerages must still execute trades via omnibus accounts on licensed exchanges (such as HashKey), with pre-funding arrangements. Retail clients are largely limited to trading large-cap tokens, and custody remains reliant on exchanges or banks.

Regulations are scattered across joint circulars, appendices, and individual license conditions, resulting in a fragmented compliance framework with limited institutional integration.

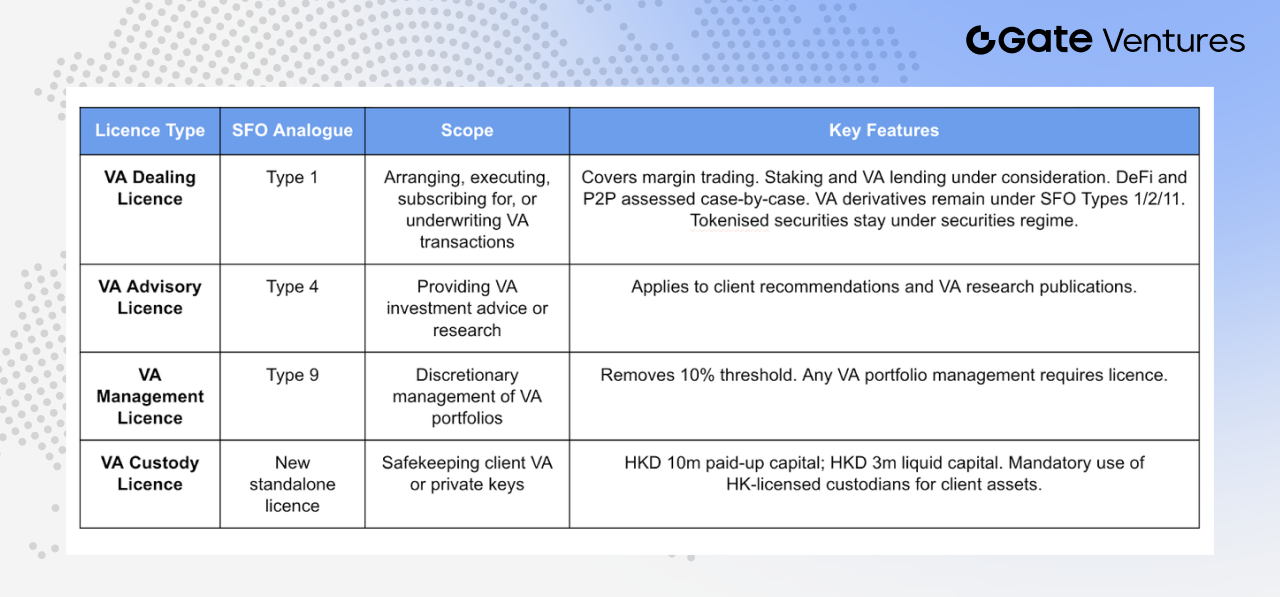

The real turning point arrived on December 24, 2025. The Financial Services and the Treasury Bureau (FSTB) and SFC jointly released a consultation summary, finalizing a new licensing regime tailored for virtual assets. This regime is incorporated into the Anti-Money Laundering and Counter-Terrorist Financing Ordinance (AMLO), with legislation targeted for 2026. A further one-month consultation was launched the same day, covering virtual asset investment advisory and asset management licenses.

The new framework divides virtual asset business into four distinct license categories:

- Virtual Asset Dealing License (VA Dealing): Modeled after SFO Type 1 license (securities trading), covering facilitation of virtual asset purchases, subscriptions, or underwriting arrangements.

This includes margin trading, staking, virtual asset lending, decentralized platforms, and P2P trading. Virtual asset derivatives (such as futures and structured products) remain regulated under SFO Types 1, 2, and 11. Tokenized securities stay within the current securities regime to avoid regulatory overlap.

-

Virtual Asset Advisory License (VA Advisory): Modeled after SFO Type 4 license, covering advisory services for virtual asset trading and publication of research or analysis related to virtual asset investment.

-

Virtual Asset Management License (VA Management): Modeled after SFO Type 9 license, covering discretionary management of virtual asset investment portfolios. The key change is the removal of the previous 10% de minimis threshold.

Previously, enhanced regulation was triggered only when virtual assets exceeded 10% of total assets in a portfolio. The new regime requires a dedicated license for any virtual asset portfolio management, regardless of percentage, eliminating regulatory gray areas caused by market fluctuations.

- Virtual Asset Custody License (VA Custody): A newly established standalone license for institutions responsible for safekeeping, controlling, or managing client virtual asset transfer tools (typically private keys).

Minimum capital requirements are HK$10 million in paid-up share capital and HK$3 million in liquid assets. Virtual asset dealers must custody client assets with an SFC-licensed virtual asset custodian based in Hong Kong, enforcing local custody to mitigate cross-border risk.

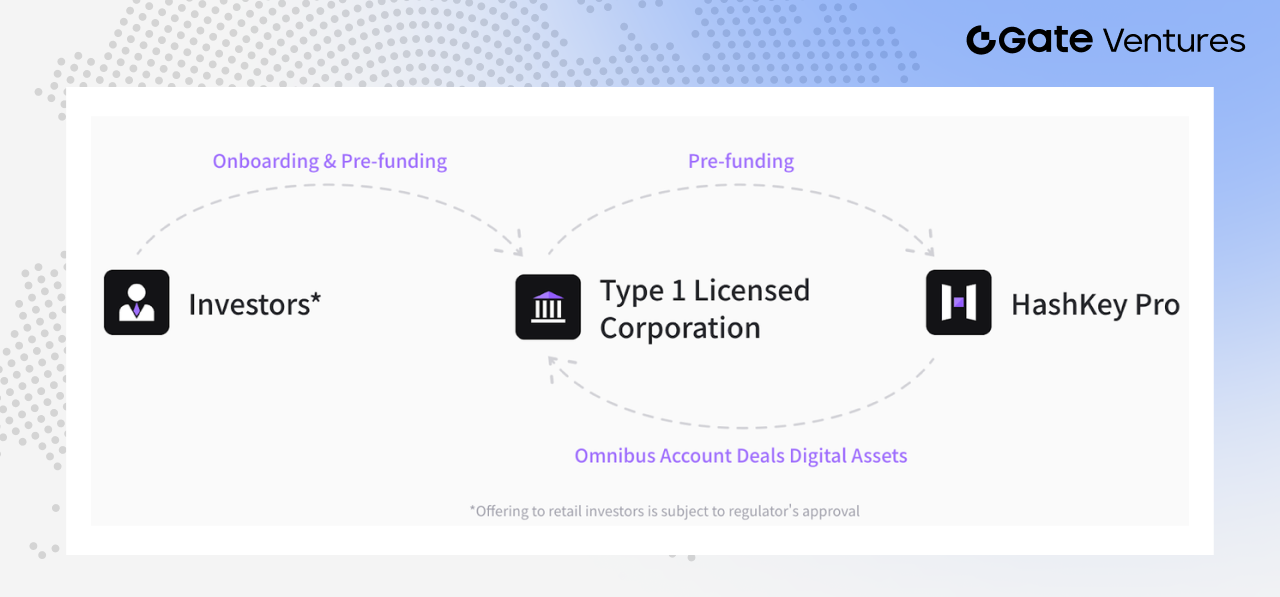

HashKey’s Central Role

Source: Hashkey Pro Docs

Within this ecosystem, HashKey Exchange serves as the infrastructure hub. In June 2025, HashKey announced its Omnibus account service covers 90% of licensed brokerages, providing virtual asset trading, custody, and settlement services to over 30 institutions—including Guotai Junan International, Futu, and Tiger. In effect, most broker crypto trades are ultimately executed through HashKey’s platform. (4)

RWA Tokenization: From Concept to Execution

While spot ETFs and trading platform licenses have yet to deliver clear scale effects or extensive real-world applications, RWA and tokenized assets are seeing more practical development.

In August 2024, the Hong Kong Monetary Authority launched Project Ensemble sandbox, with an initial focus on fixed income and investment funds, liquidity management, green finance, and trade and supply chain finance. Subsequently, the Hong Kong market saw several representative tokenization and RWA projects, signaling a shift from proof-of-concept to real-world deployment.

In the new energy sector, Longshine Group and Ant Digital completed approximately RMB 100 million in cross-border RWA financing based on charging pile revenue rights. GCL New Energy partnered with Ant Digital to tokenize photovoltaic asset revenue rights, raising over RMB 200 million. Xunying Group is advancing RWA exploration for two-wheeler battery swap assets, reflecting a broadening application scope. (5)

Fund products are also making strides. ChinaAMC (Hong Kong) launched a HKD tokenized money market fund in February 2025, widely recognized as one of Asia-Pacific’s first tokenized funds for retail investors, with an initial size of $107–$110 million and distribution via OSL, Futu, and other channels. (6)

In March 2025, Bosera International and HashKey’s HKD and USD tokenized money market ETF shares received SFC approval. By July 2025, ChinaAMC (Hong Kong) introduced USD and RMB tokenized money market funds, with the RMB fund reported as the world’s first RMB-denominated tokenized fund. (7)

In the second half of 2025, RWA applications expanded beyond new energy. Deli Holdings announced a partnership with Asseto to explore tokenization of up to HK$500 million in physical assets, including property rights and fund assets. Hanyu Pharmaceuticals signed an MOU with KuCoin to pilot RWA based on future revenue rights for innovative drugs in Hong Kong. Medical and real estate firms are also exploring IP and commercial property tokenization.

Recent cases include tokenization of precious metals, such as silver tokens issued by Eddid Financial and XAUM, an on-chain gold token anchored to LBMA-certified gold on EX.IO, indicating RWA scenarios are extending into commodities. (8) (9)

Esperanza Securities, with regulatory approval, launched two tokenized entertainment investment projects: Hong Kong’s “Wong Ka Kui 40th Anniversary Concert 2026” and a Korean boy band concert in Malaysia. These cases reflect the continuous expansion of tokenized asset applications. (10)

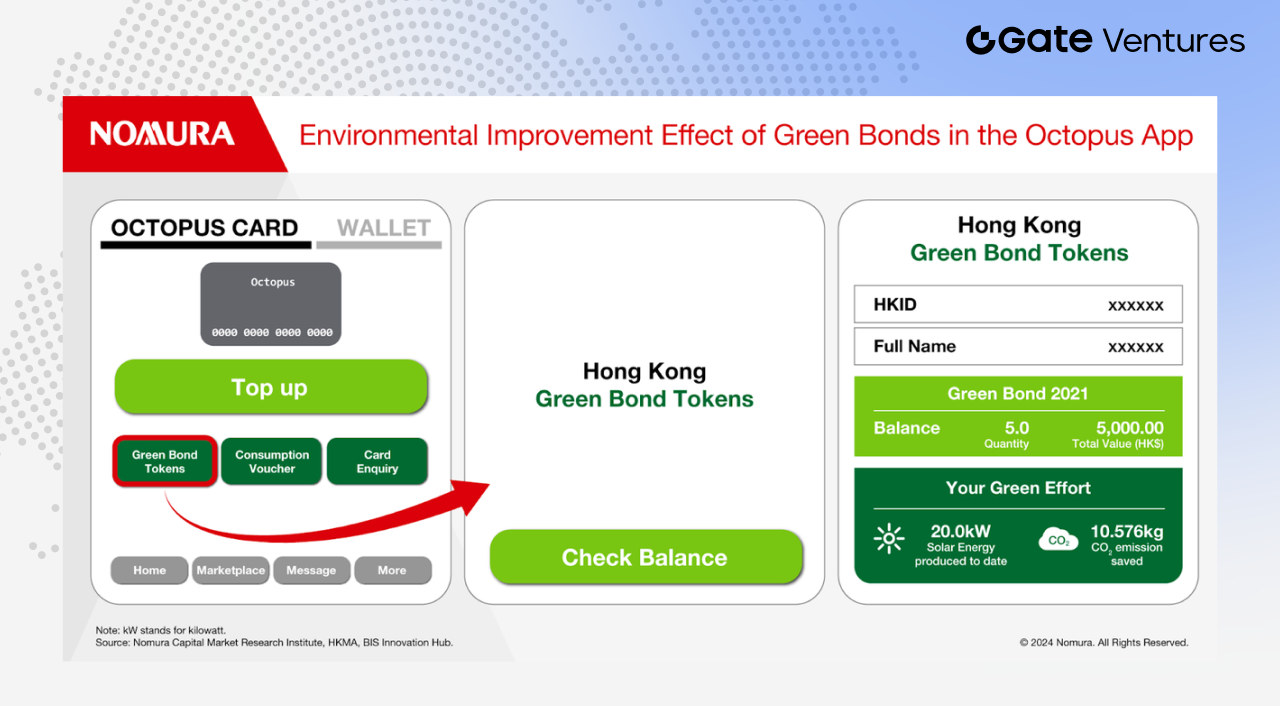

Hong Kong Government Tokenized Bonds: From Pilot to Mainstream

While tokenization at the corporate and fund level is still evolving, the development of Hong Kong government tokenized bonds clearly demonstrates the official push toward institutionalization.

Source: Nomura

The Hong Kong government has completed multiple rounds of tokenized bond issuance. In Q4 2025, the SAR government issued its third batch of tokenized green bonds, totaling HK$10 billion. Authorities have indicated that tokenized bonds will gradually transition to regular issuance.

In the 2026–27 fiscal budget, Financial Secretary Paul Chan announced that CMU OmniClear Holdings, a wholly-owned HKMA subsidiary, will develop a dedicated digital asset platform for tokenized bond issuance, registration, and settlement, with plans to expand to more digital asset types. (11)

This shows tokenized bonds are moving beyond experimental trials and are becoming part of Hong Kong’s long-term financial infrastructure.

CMU OmniClear: The Backbone for Tokenized Bonds

CMU OmniClear is pivotal. As the operator of Hong Kong’s Central Moneymarkets Unit (CMU), it is a core infrastructure for government bond issuance and settlement.

Both traditional and tokenized government bonds rely on the CMU system for registration, custody, and settlement. Integrating tokenized bonds into CMU OmniClear is not a new beginning, but a direct connection to Hong Kong’s existing bond infrastructure.

This arrangement offers three key advantages:

- Standardized processes: Tokenized bonds use a mature settlement system

- Clear regulation: HKMA direct involvement and oversight

- Scalable platform: Designed for institutional-level adoption from day one

With HKEX acquiring a 20% stake in CMU OmniClear Holdings in November 2025, the platform is further positioned as critical infrastructure for Hong Kong’s fixed income and money markets. (12)

In summary, Hong Kong’s tokenization landscape is evolving along two main tracks: market-driven exploration of corporate, fund, and physical assets, and institutionalized development anchored in government bonds and core financial infrastructure. The latter is particularly significant, as tokenization is steadily entering the heart of Hong Kong’s financial system.

Stablecoin Legislation: Bridging RWA’s “Last Mile”

RWA tokenization faces a structural challenge: assets are on-chain, but funds remain off-chain.

Even if underlying assets are tokenized, key steps—financing, subscription/redemption, and distribution—still depend on the traditional fiat system. The gap between on-chain and off-chain remains. Stablecoins are the key infrastructure to bridge this divide.

On May 21, 2025, Hong Kong’s Legislative Council passed the Stablecoin Bill, taking effect August 1, 2025. Key requirements include:

- Issuers must be Hong Kong-registered entities with at least HK$25 million paid-up share capital

- Reserve assets must fully cover circulation and be strictly segregated from proprietary assets

- Holders have statutory rights to redeem at par value

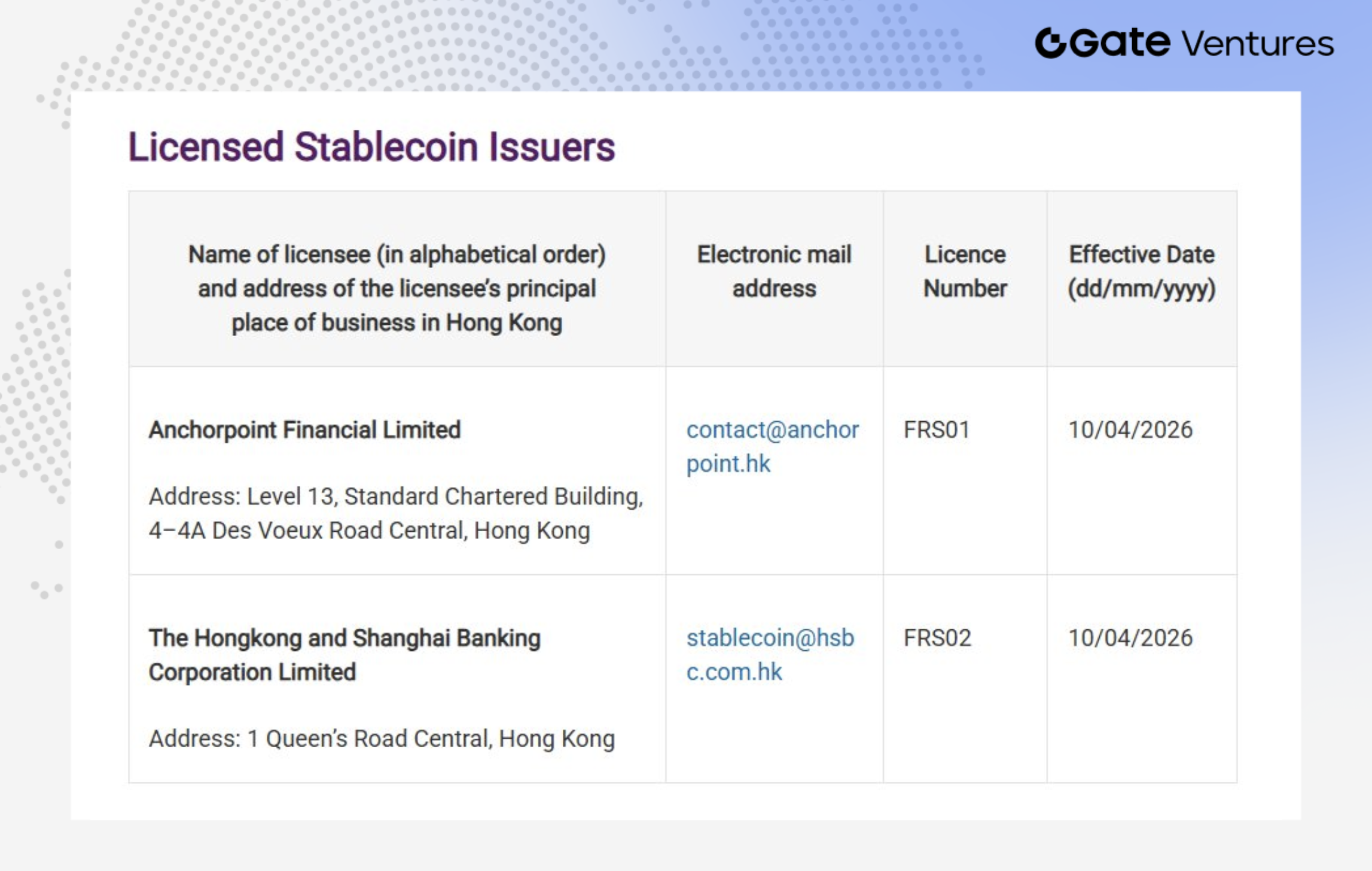

Source: HKMA (as of February 4, 2026)

The HKMA has issued the first two stablecoin issuer licenses to The Hongkong and Shanghai Banking Corporation Limited and Anchorpoint Financial Limited (a joint venture between Standard Chartered, Animoca Brands, and Hong Kong Telecom). (13)

HSBC plans to launch a HKD stablecoin in the second half of 2026, integrating with PayMe and HSBC HK App. Initial use cases include P2P transfers (instant stablecoin transfers via PayMe and HSBC HK App), P2M payments (stablecoin payments to merchants via PayMe), and tokenized investment (stablecoin subscriptions for tokenized products via HSBC HK App).

Standard Chartered’s Anchorpoint Financial Limited will launch HKDAP, a regulated HKD-pegged stablecoin, in phases starting Q2. The B2B2C model leverages distributor networks to expand reach and drive adoption in retail and payment scenarios.

From both institutions’ market strategies, several points stand out. Stablecoins are currently more like settlement infrastructure than standalone consumer products. Their presence is mostly felt in improved payment and clearing efficiency—lower transaction costs, faster transfers, and movement toward real-time settlement.

Retail adoption in Hong Kong is still nascent, with demand and usage habits not fully established. The mass market remains unproven, and distribution channels are dominated by banks and licensed institutions, not organic retail growth.

Thus, product rollout, user coverage, and penetration remain uncertain. Hong Kong’s stablecoin market is entering formal implementation, but commercialization and retail adoption are still in the early exploration phase.

Taking a Step Back: Where Are the Gaps?

Objectively, several issues remain:

- ETF scale gap is substantial. Hong Kong’s six virtual asset ETFs manage about $333 million, while US Bitcoin ETFs manage nearly $90 billion and have net inflows over $56 billion—two orders of magnitude apart.

- Most RWA projects are still in sandbox or private placement stages. Cases like Longshine charging piles and GCL photovoltaics are demonstrative, but overall financing remains in the RMB 100–200 million range, far from the trillion-dollar tokenization vision.

For commodity tokenization, demand-side development is uncertain. In the US, tokenized gold is being integrated into DeFi as collateral and leveraged lending, opening up to retail investors and forming a usage ecosystem. In Hong Kong, most products target professional investors, with retail channels not fully open—reflecting a cautious approach to investor protection.

- The “on-chain asset, off-chain funds” disconnect persists. The Stablecoin Bill is enacted, but widespread adoption of compliant stablecoins will take time.

The market will be watching where stablecoins find real-world use first—cross-border payments, settlement for on-chain asset trades, subscription/redemption for tokenized funds or bonds, and cash management within enterprises or platforms.

These scenarios can help bridge the current gap for RWA. HKMA has clarified that initial licenses will be limited, and applicants must demonstrate clear use cases, robust operations, and credible business models. Regulators are focused on real-world adoption, not just token issuance.

Main data sources:

- https://www.reuters.com/markets/currencies/asias-first-spot-bitcoin-ether-etfs-gain-hong-kong-debut-2024-04-30/?

- https://www.coinglass.com/hk-etf-eth

- https://www.21jingji.com/article/20250626/herald/7a7d09161b82588b801777a3d6f713db.html

- https://www.wublock123.com/news/news-44551

- https://www.21jingji.com/article/20250710/herald/10533d03952cd28b3c08f3be0ea28e1b.html

- https://www.chinaamc.com.hk/zh-hant/product/chinaamc-hkd-digital-money-market-fund/

- https://group.hashkey.com/newsroom/hashkey-group-and-bosera-launch-world-s-first-tokenised-money-market-etf

- https://www.prnewswire.com/apac/news-releases/eddid-financial-coordinates-issuance-of-hong-kongs-first-silver-rwa-302728489.html

- https://phemex.com/news/article/exio-launches-xaum-gold-token-for-professional-investors-57051

- https://finance.mingpao.com/fin/instantf/20260223/1771841319302/esperanza%E8%AD%89%E5%88%B8%E6%8E%A8%E5%A8%9B%E6%A8%82%E7%94%A2%E6%A5%AD%E4%BB%A3%E5%B9%A3%E5%8C%96-%E9%BB%83%E5%87%B1%E8%8A%B9%E6%BC%94%E5%94%B1%E6%9C%83%E6%88%90%E9%A6%96%E5%80%8B%E4%BB%A3%E5%B9%A3%E5%8C%96%E9%A0%85%E7%9B%AE

- https://www.budget.gov.hk/2026/chi/ui.html

- https://www.hkex.com.hk/News/News-Release/2025/251112news?sc_lang=zh-HK

- https://www.coindesk.com/policy/2026/03/24/hong-kong-awards-first-stablecoin-licenses-to-hsbc-standard-chartered-led-group

About Gate Ventures

Gate Ventures is the venture capital arm of Gate, specializing in investments across decentralized infrastructure, ecosystems, and applications to shape the Web 3.0 era. Gate Ventures partners with global industry leaders, empowering teams and startups with innovative thinking and capabilities to redefine the intersection of society and finance.

For more information, visit: Official Website | X | Telegram | LinkedIn | Medium

Disclaimer:

This content does not constitute an offer, solicitation, or advice. Always seek independent professional advice before making any investment decisions. Gate Ventures may restrict or prohibit services for users from certain regions. Please review the user agreement for details: https://www.gate.com/zh/user-agreement.