When the market undergoes steep declines, narratives often quickly seek a clear culprit.

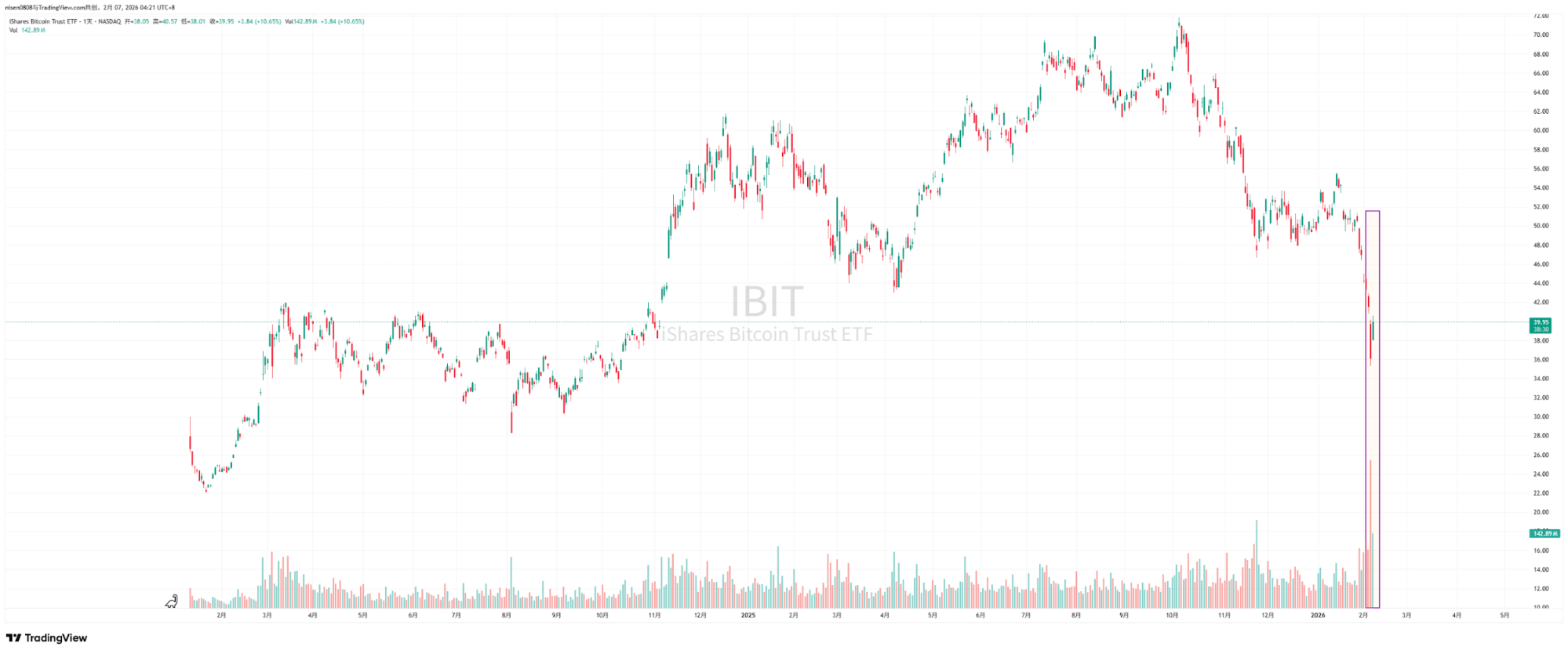

Recently, market participants have been discussing the February 5 crash and the subsequent rebound of nearly $10,000 on February 6 in depth. Bitwise advisor and ProCap Chief Investment Officer Jeff Park contends that this volatility is more tightly connected to the Bitcoin spot ETF ecosystem than many believe, with critical evidence emerging in BlackRock’s iShares Bitcoin Trust (IBIT) secondary market and options market activity.

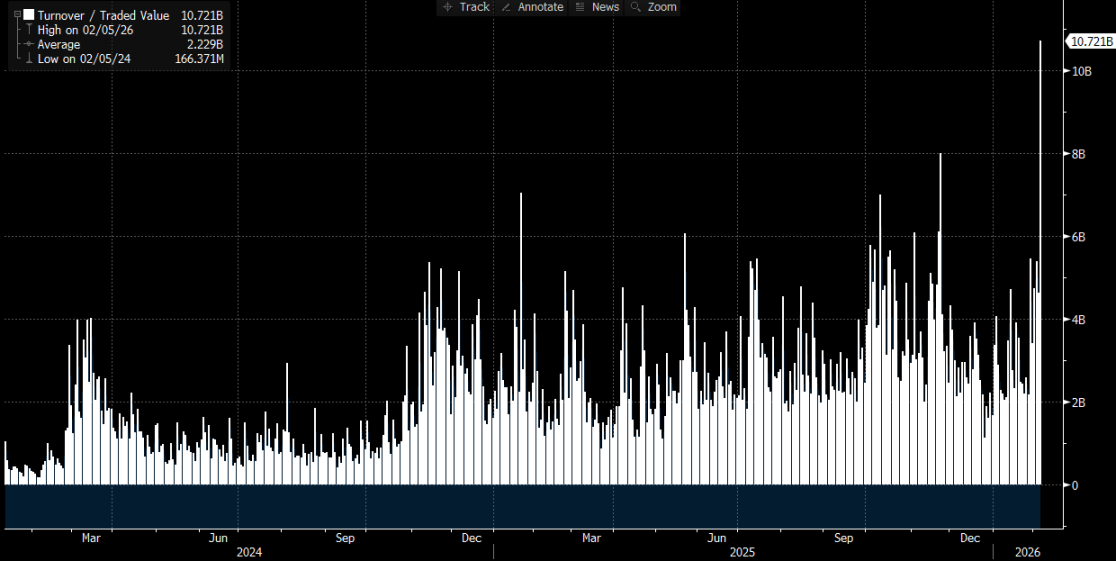

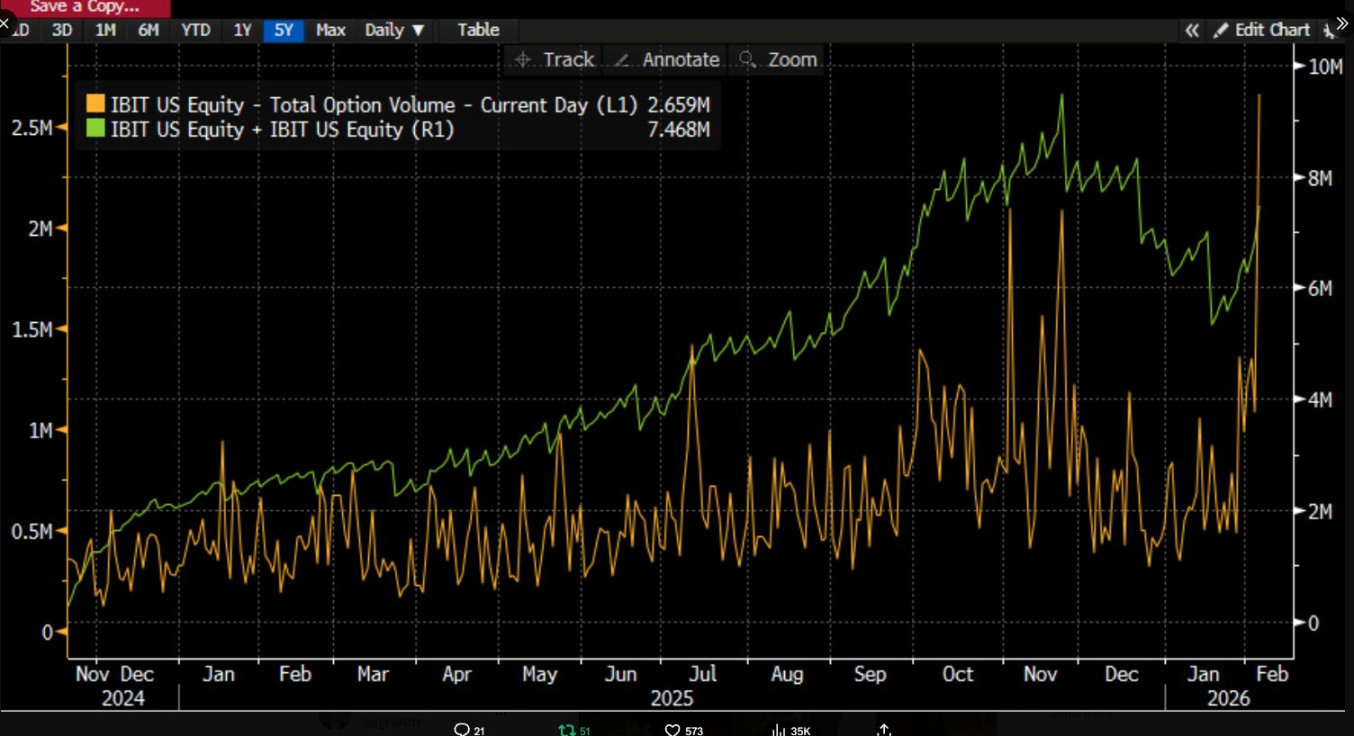

He observed that on February 5, IBIT posted record trading volumes and heightened options activity, with volumes far surpassing historical averages and options trading skewed toward puts. Surprisingly, historical patterns suggest that double-digit price drops in a single day typically prompt significant net redemptions and capital outflows, but this time the opposite occurred. IBIT recorded net creations, with newly issued shares increasing its scale, and the entire spot ETF portfolio experienced net inflows.

Jeff Park argues that this “crash with net creation” scenario diminishes the explanatory power of the single-path thesis that panic-driven ETF redemptions cause price declines. Instead, it aligns more closely with traditional financial system deleveraging and risk reduction, where traders, market makers, and multi-asset portfolios are forced to reduce risk within derivatives and hedging frameworks. Selling pressure mainly stems from portfolio adjustments and hedging chain squeezes within the paper capital system, ultimately impacting Bitcoin prices through IBIT’s secondary market trading and options hedging.

Many market discussions tend to directly link IBIT institutional liquidations with market-driven crashes, but without breaking down the mechanisms, the causal sequence is easily misrepresented. ETF secondary market trading involves ETF shares, while primary market creations and redemptions correspond to changes in the underlying BTC held in custody. Directly mapping secondary market trading volumes to equivalent spot sales omits several critical steps in the logic.

The “IBIT-Triggered Large-Scale Liquidation” Debate Is Really About Transmission Mechanisms

The debate surrounding IBIT centers on which layer of the ETF market and through what mechanism pressure is transmitted to Bitcoin price formation.

A common narrative focuses on net outflows in the primary market. The intuition is simple: if ETF investors redeem shares in panic, issuers or authorized participants must sell underlying BTC to meet redemption payments, introducing sell pressure to the spot market, which triggers further forced liquidations and a cascade effect.

This logic seems complete but often overlooks a critical fact. Ordinary investors and most institutions cannot directly subscribe or redeem ETF shares—only authorized participants can create or redeem in the primary market. The commonly cited “daily net inflows and outflows” refer to changes in the total primary market share count; even large secondary market trades only change share ownership, not the total share count, and do not automatically alter the amount of BTC held in custody.

Analyst Phyrex Ni notes that what Parker describes as liquidation is actually IBIT spot ETF liquidation, not Bitcoin liquidation. In IBIT, only ETF shares are traded in the secondary market, with prices anchored to BTC, but the trades themselves are completed within the securities market.

The only stage that truly involves BTC occurs in the primary market—share creation and redemption—executed by APs (market makers). For creations, new IBIT shares require APs to provide corresponding BTC or cash, with BTC entering the custody system and subject to regulatory constraints, so issuers and related institutions cannot freely access it. For redemptions, BTC is handed to the AP by the custodian, and the AP handles subsequent disposition and settles redemption funds.

ETFs operate across two market layers: the primary market primarily handles Bitcoin purchases and redemptions, almost exclusively provided by APs. This is fundamentally similar to using USD to mint USDC, and APs rarely circulate BTC via exchanges, so the main effect of spot ETF purchases is to lock up Bitcoin liquidity.

Even when redemptions occur, APs’ sales don’t necessarily go through the open market—especially not through exchange spot markets. APs may hold BTC inventory or use flexible methods within the T+1 settlement window for delivery and fund management. As a result, even during the large-scale liquidation on January 5, BlackRock investors redeemed fewer than 3,000 BTC, and all US spot ETF institutions redeemed less than 6,000 BTC in total. This means the maximum Bitcoin sold by ETF institutions to the market was 6,000 coins, and not all of these necessarily entered exchanges.

Parker’s reference to IBIT liquidation actually pertains to the secondary market, with total trading volume around $10.7 billion—the largest in IBIT’s history—which did trigger some institutional liquidations. However, this liquidation pertains only to IBIT, not Bitcoin, and at least this portion did not transmit to IBIT’s primary market.

Therefore, Bitcoin’s sharp decline only triggered IBIT liquidation, not BTC liquidation caused by IBIT. The underlying asset of ETF secondary market trading is still the ETF, with BTC serving as the price anchor. The only market-impacting liquidation comes from primary market BTC sales, not IBIT. In fact, although BTC prices fell more than 14% on Thursday, BTC net outflows from ETFs accounted for only 0.46%. On that day, spot Bitcoin ETFs held 1,273,280 BTC, with total outflows of 5,952 BTC.

How IBIT Pressure Transmits to the Spot Market

@MrluanluanOP argues that when IBIT long positions are liquidated, concentrated selling occurs in the secondary market. If natural buy-side demand is insufficient, IBIT trades at a discount to its implied net asset value. The greater the discount, the larger the arbitrage opportunity, incentivizing APs and market arbitrageurs to buy discounted IBIT, as this is their routine profit strategy. As long as the discount covers costs, professional capital will always be willing to step in, so concerns about “no buyers for sell pressure” are unfounded.

After acquiring the shares, the focus shifts to risk management. APs cannot immediately redeem these shares at current prices—redemption involves time and process costs. During this period, BTC and IBIT prices continue to fluctuate, exposing APs to net exposure risk, so they hedge immediately. Hedging may involve selling spot inventory or opening BTC short positions in the futures market.

If the hedge involves spot sales, it directly pressures the spot price. If it involves futures shorts, it first manifests as price spreads and basis changes, then further affects spot prices through quant, arbitrage, or cross-market trades.

Once hedging is complete, APs hold a relatively neutral or fully hedged position and can flexibly decide when to deal with the IBIT shares. One option is to redeem with the issuer the same day, which appears in official inflow/outflow data as redemption and net outflow after the close. Another is to delay redemption, waiting for secondary market sentiment to recover or prices to rebound, and then sell IBIT back into the market, completing the trade without touching the primary market. If IBIT returns to a premium or the discount narrows the next day, APs can sell their holdings in the secondary market for spread profits while closing futures shorts or replenishing previously sold spot inventory.

Even if most share handling happens in the secondary market and the primary market doesn’t see significant net redemptions, IBIT pressure can still transmit to BTC, because APs’ hedging actions when taking on discounted shares transfer pressure to BTC spot or derivatives markets. Thus, IBIT secondary market sell pressure spills over to the BTC market via hedging activity.

Disclaimer:

- This article is reprinted from [Foresight News]. Copyright belongs to the original author [ChandlerZ]. If you have any objections to this reprint, please contact the Gate Learn team, and the team will handle your request promptly according to relevant procedures.

- Disclaimer: The views and opinions expressed in this article are solely those of the author and do not constitute investment advice.

- Other language versions of this article are translated by the Gate Learn team. Do not copy, distribute, or plagiarize translated articles without referencing Gate.