Event Core: Why Anthropic Has Entered the "Seller Disappearance" Phase

Image source: Anthropic Official Website

The central focus of this market event is not Anthropic’s employee equity transfer (tender offer), but the outcome of the transaction itself: At an estimated $350 billion valuation, external capital lined up with ample bids, yet internal employees did not sell in significant volume.

This situation can be described as a “seller disappearance”:

- Ongoing buyer demand;

- Proactive contraction of seller supply;

- Price discovery shifts from “buyer negotiation” to “seller-controlled supply.”

In both the primary and private secondary markets, this typically signals two things:

- Internal holders have much higher expectations for future prices than the current transaction price;

- Tradable equity becomes scarce, passively driving the valuation anchor higher.

In other words, the market is no longer asking “is there anyone willing to buy Anthropic,” but “who can buy enough Anthropic.”

Why Employees Aren’t Selling: Price Expectations, Tax Costs, and Liquidity Choices

From the employee’s perspective, this is a classic intertemporal return problem—not a simple cash-out decision.

Selling now at a $350 billion valuation provides immediate liquidity, but comes with two opportunity costs:

- Giving up potential capital gains from a possible upward revaluation before or after an IPO;

- Passing future upside returns to the current buyer.

Employee reluctance to sell is generally driven by a combination of these three factors:

- Clear expectations of a valuation jump: If the market expects an IPO valuation range of $400 billion to $500 billion, selling now is seen as “giving up future upside early.”

- Growth trajectory remains steep: When the company is still in a rapid expansion phase, employees are more likely to treat equity as a mid-term asset rather than a short-term cash-out tool.

- Tax and timing strategies can be offset by “expected upside”: Even if capital gains taxes are high in some regions, as long as employees believe the valuation will rise significantly, the appeal of short-term tax optimization fades.

This explains why the window opens, yet many choose to “take a look, then close it again.”

Valuation Beyond Sentiment: Rebuilding Anthropic’s Pricing Framework with Four Variables

To assess whether Anthropic can continue to see upward repricing, the discussion must shift from sentiment to structural factors.

Consider these four variables as a pricing framework:

Growth Variable: ARR and Growth Sustainability

The current high valuation is built on the premise of sustained high growth. If ARR maintains a steep growth rate, the valuation ceiling will continue to rise; if growth slows quickly, valuation multiples will compress.

Quality Variable: Revenue Recognition and Comparability

Businesses of similar scale can report different revenue figures under gross vs. net accounting. If regulators or underwriters require stricter comparability ahead of the IPO, the market will re-evaluate the gap between nominal revenue and actual monetization.

Cost Variable: Cloud Channel Revenue Sharing and Gross Margin Structure

For AI model companies, the key question is not “can it scale,” but “can margins improve as it scales.”

If cloud channel costs remain high and inference costs decrease slowly, the company will face a “high revenue, low free cash flow” valuation discount.

Liquidity Variable: Tradable Equity Supply and Capital Crowding

When tradable legacy shares are scarce and outside capital keeps lining up, implied secondary valuations often exceed the most recent funding round.

But this also means that if supply is suddenly released, price volatility will spike.

Of these four variables, the first two determine “how high the valuation can go,” while the latter two determine “how long it can be sustained.”

The Key Disagreement: “Quality Discount” for High-Growth Revenue and Accounting Standards

The biggest debate around Anthropic right now is not about demand, but about how to price revenue quality.

In essence, the disagreement centers on two questions:

- Of the high-growth revenue, how much is sustainable and able to be repeated at high gross margins?

- How can revenue numbers be standardized for comparability across different sales channels and accounting methods?

This directly impacts the choice of valuation multiples. For high-growth companies, if the market believes revenue quality is high, standards are clear, and cost reduction is visible, it will assign a higher PS multiple; otherwise, even with strong growth, a significant “quality discount” will apply.

Thus, Anthropic’s valuation game has entered a new phase:

- Phase one: “Who is growing faster?”

- Phase two: “Whose growth is more verifiable and deliverable?”

IPO Implications: How Primary Market Reluctance to Sell Affects Secondary Market Pricing

Employee reluctance to sell is not just a sentiment indicator for IPOs—it’s a prior signal about supply-demand structure.

Positive Transmission Path

- Fewer tradable shares in the primary market;

- Private secondary market transactions become scarcer;

- Public investors face increased competition for IPO allocations;

- Initial and early valuation anchors may be elevated.

Reverse Constraint Path

- If macro risk appetite declines, overall IPO market valuations will fall;

- If accounting disputes intensify, underwriters will take a more conservative approach to pricing;

- If peers in the same sector underperform, valuation premiums will compress rapidly.

So, reluctance to sell is a positive signal—but not an unconditional one.

It raises the “scarcity premium,” but does not automatically eliminate “fundamental verification risk.”

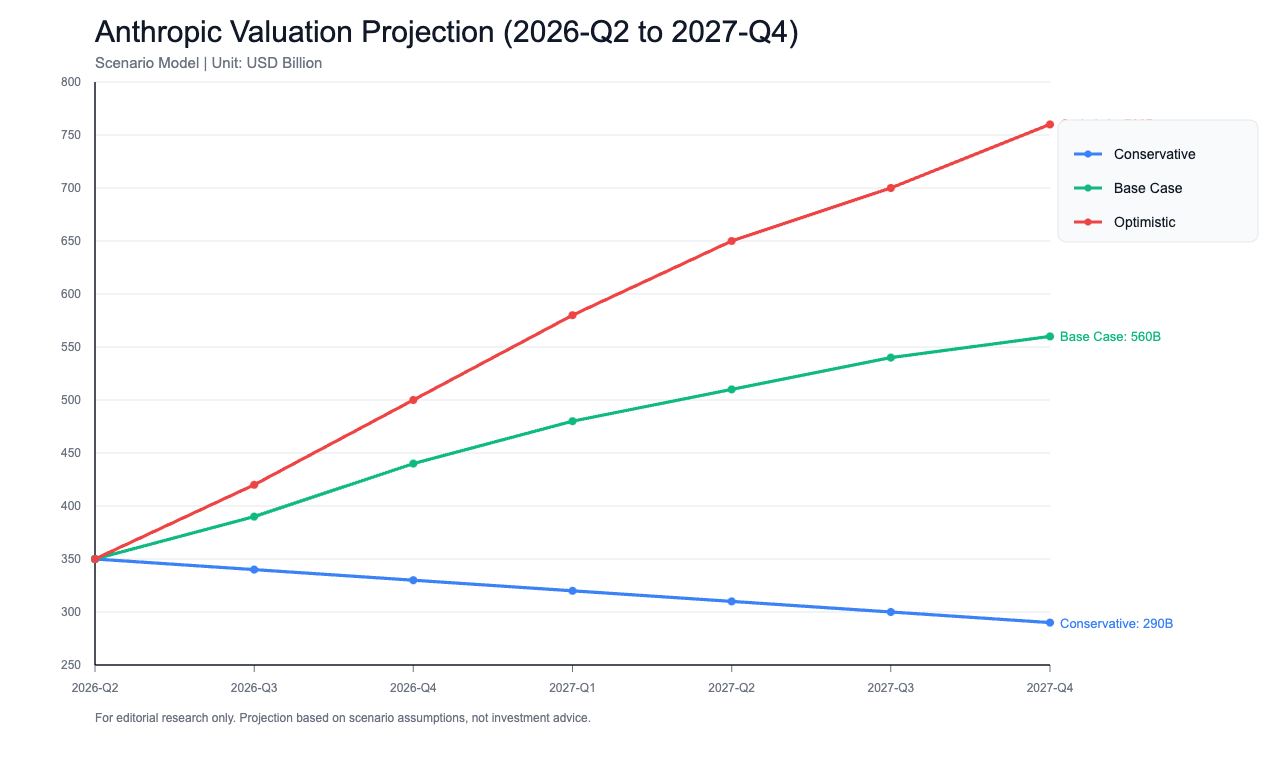

6–12 Month Valuation Forecast: Conservative, Baseline, and Optimistic Scenarios

The following is a research framework and does not constitute investment advice.

Conservative scenario: $280 billion–$380 billion, triggered by:

- Weaker macro environment and a broad valuation correction for tech growth stocks;

- Revenue recognition adjustments lead to downward revisions in comparable revenue;

- Cloud channel cost pressures exceed expectations.

Feature: Valuation shifts from narrative-driven to cash flow–discounted.

Baseline scenario: $420 billion–$550 billion, triggered by:

- Growth remains high but slows at the margin;

- IPO proceeds on schedule;

- Accounting issues are explainable but still warrant a discount.

Feature: Valuation continues to rise, but volatility increases and the market places greater emphasis on quarterly verification.

Optimistic scenario: Above $600 billion, triggered by:

- Sustained high demand, with enterprise revenue and developer ecosystem expanding in tandem;

- Cost curve improves faster than expected;

- IPO market risk appetite recovers, amplifying the premium for scarce assets.

Feature: Valuation shifts from high-growth company levels to platform-level infrastructure.

From a probability perspective, the current scenario is closer to “baseline with an optimistic tilt,” but linear extrapolation is not appropriate. The real focus should be on inflection point variables, not single-point valuation numbers.

Conclusion: Anthropic’s Next Stage Is Not “Can It Be More Expensive,” but “Can It Prove More Stable”

Anthropic’s current valuation logic is straightforward:

- Internal employee reluctance to sell has reinforced upside expectations;

- Ample external bids have confirmed the asset’s scarcity;

- The IPO expectation window has amplified intertemporal returns.

But as the valuation game enters deeper waters, the market’s question shifts from “can it go higher” to “can it be audited, compared, and replicated.”

This means the most important thing going forward is not telling a bigger story, but delivering more stable financials:

- A sustainable growth trajectory;

- Transparent and explainable revenue recognition;

- An improvable profit structure.

Anthropic has already proven it deserves to be discussed at high valuations; the next step is to prove that these high valuations can be confidently priced by long-term holders.