Yield Prospects Remain Unclear, Payments Are Ascendant

Following the July 2025 passage of the Genius Act, yield stablecoins have encountered broad resistance from the banking sector, while payment stablecoins are flourishing.

Legacy payments have emerged as a new focal point, demonstrating the intricate interplay between Agents and stablecoins within Fintech and Crypto.

Yield belongs to the past, payments to the present, and AI to the future—a categorization that's risky and quickly outdated, but it offers a convenient chronological framework for understanding industry shifts.

Meta has renewed its commitment to stablecoins, Google has allied with over 60 companies to launch the AP2 Alliance, and Stripe sees stablecoins and Agents as key to its future. However, PayPal, which introduced $PYUSD early, and Coinbase, which put forth the x402 protocol, have both seen their stock prices decline.

We urgently face two questions: First, what drives the new battle in payments—who is stoking market sentiment? Second, are Agents and stablecoins truly the next ticket to industry advancement?

This article addresses the former. The interplay among AI, blockchain, and stablecoins will be discussed in a subsequent piece, and outlooks for yield stablecoins will follow once legislation becomes clearer.

The Losers Lag Behind: Fintech’s Anxiety Surpasses Crypto’s

Crypto holds promise, but individuals lack prospects.

Tokenization of U.S. stocks and Treasuries is accelerating, BlackRock and WisdomTree are repeatedly embracing DeFi, and tokenomics is inevitably approaching its endpoint. The wealth-creation effects of blockchain are no longer believed—even with real-world adoption of public chains and Vaults, price appreciation for $ETH or $Aave is not guaranteed.

This view isn’t entirely incorrect but overstates Crypto’s challenges; Fintech is truly at an existential crossroads.

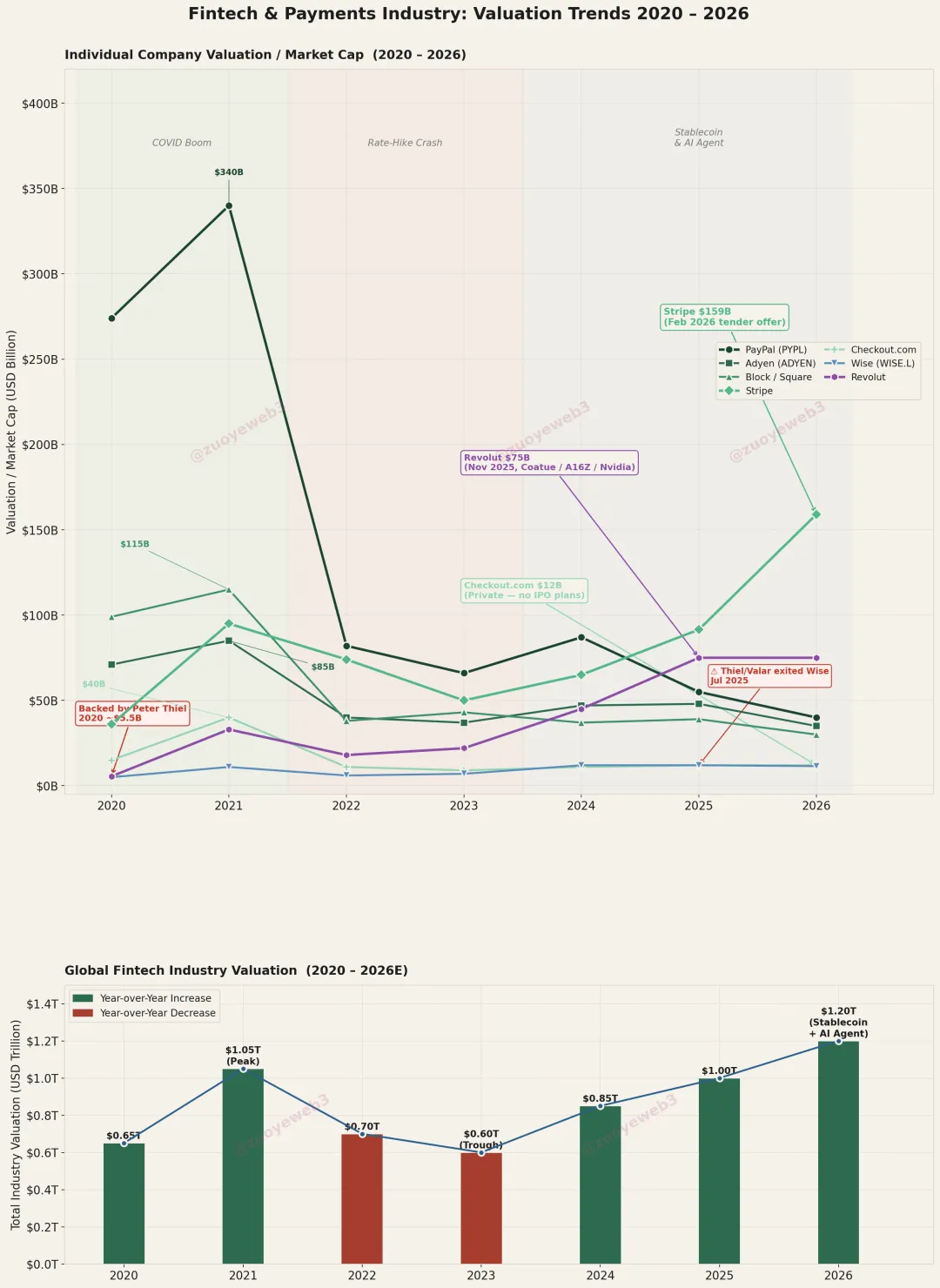

After Stripe reached a $159 billion valuation, such a counterintuitive conclusion is justified.

Examining capital flows—Peter Thiel liquidating Wise stock, backing Trade Republic and other NeoBroker initiatives, or observing the elite investor lineup for Europe’s highest-valued NeoBank, Revolut ($75B)—the logic behind Fintech valuation has changed.

Decades of effort have failed to establish payment rails independent of banks. Only those capable of retaining or converting user funds are considered valuable; Wise’s transfer services and Stripe’s acquiring have no genuine future.

Image caption: Value shifts in Fintech & Payment

Image source: @ zuoyeweb3

One factor is the inability to fully bypass banks for fund handling; another is that blockchain can do it for less.

This is not a problem isolated to individual companies—the Fintech sector peaked during the pandemic. PayPal, once valued at $340 billion in 2021, is now rumored to be seeking a sale. By 2026, the sector will be forced to prove its advantage over stablecoins and Agents.

Stripe’s valuation is five times Adyen’s ($35B), thirteen times Checkout.com’s ($12B), yet Stripe’s business volume doesn’t match this multiple. The leverage is driven by speculation around stablecoins and Agents.

Fintech’s anxiety is far more acute than Crypto’s. “Public chain + stablecoin” is self-sustaining; DeFi is a killer app. What we see as the new payment battle is simply Fintech inflating its own valuation.

Fintech’s only advantage is in existing assets; the future belongs to Crypto.

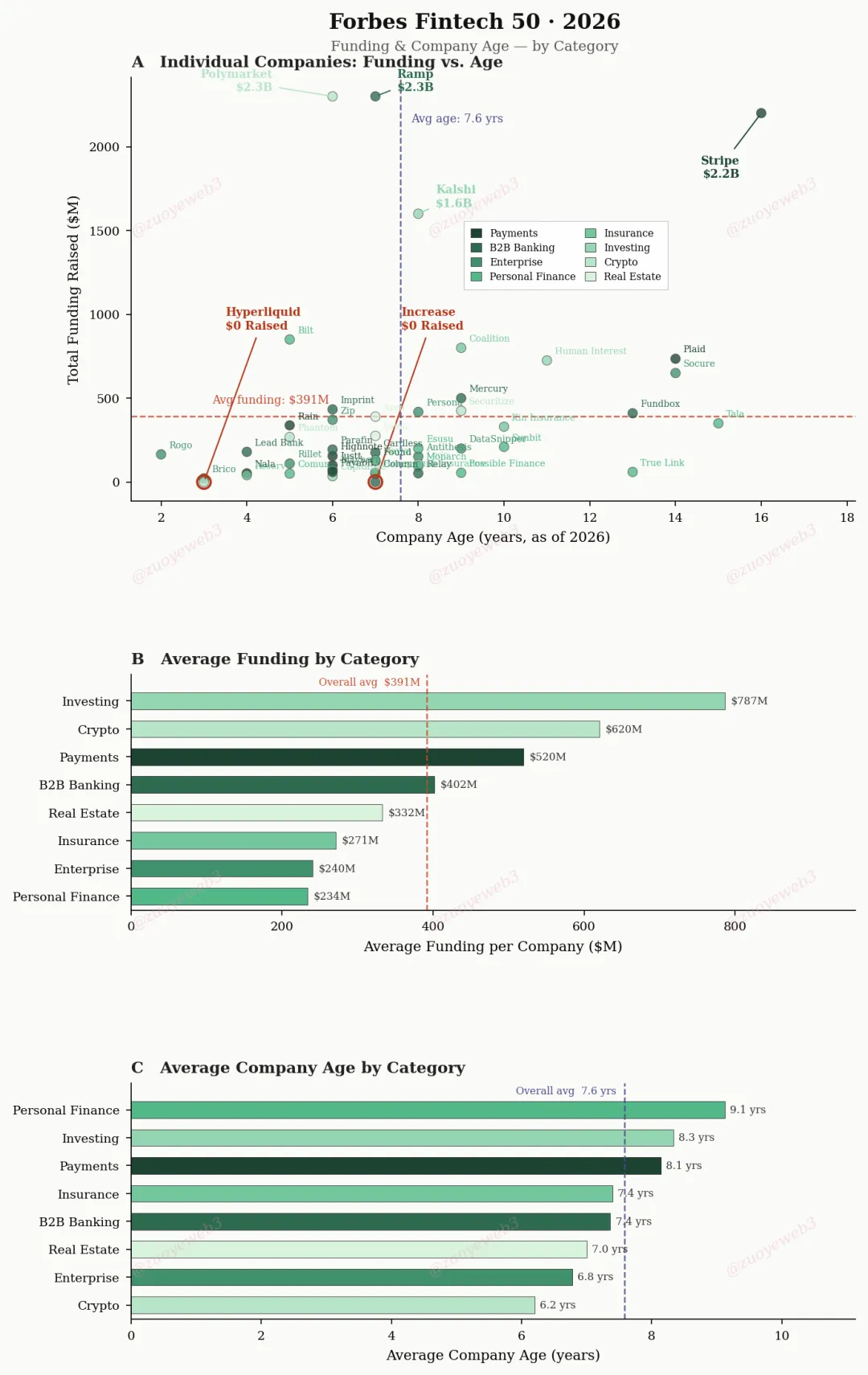

Image caption: Forbes Fintech 50

Image caption: Forbes Fintech 50

Data source: @ ForbesCrypto

Forbes data shows that payment-focused Fintech companies take an average of 8.1 years to make the list, while Crypto firms do so in just 6.2 years.

From a business perspective, long-haul firms like Stripe must justify themselves to capital markets—perhaps even provide an exit rationale. Capital needs to be allocated to a fresher or larger opportunity.

- Larger: Agents will exponentially increase payment transactions. Stripe’s founders, the Collison brothers, believe a chain supporting a billion TPS is needed;

- Fresher: Leveraging stablecoins to transform the payment technology stack—this is the greatest shift since the API-first model.

To realize this promising future, Fintech must not only prove superiority over Crypto firms but also face resistance from banks and internet giants, whose sheer number is turning the market chaotic.

Compared to unicorns like Stripe, mega-platforms like Meta and Google are even more formidable—trillion-dollar valuations and billions of users are commonplace. As channel operators, their role is to share in transaction profits; they may see an opportunity to build their own stablecoins or payment protocols, or simply use their existing advantages to charge higher tolls.

Under Vitalik’s leadership, Crypto handed over its independent hardware layer to the internet, becoming reliant on AWS. Still, blockchain has become a recognized foundation for money movement among banks, internet firms, Fintech, and regulators.

Consensus is still needed on whether banks should be fully replaced, and how payment stablecoins can leverage C2C/B2B distinctions to capture B2C business.

Tether and Circle: Mutual Strategic Encirclement

USDT recedes into the background, surrounding the West from emerging markets; USDC is strengthening its on-chain presence, with compliance serving as a protective layer for replacing banks.

Blockchain can bypass bank-centric finance and, through underground economies, achieve a “theoretical minimum” of independence. In ten years of Ethereum’s evolution, it has demonstrated superior capital efficiency compared to TradFi.

Notably, this dominance isn’t about capital scale: $ETH at $236 billion, stablecoins at $300 billion, $BTC at $1.32 trillion—combined, they don’t surpass JPMorgan’s $2.5 trillion in deposits.

The advantage is that banking alliances can lock out Fintech and PSP (Payment Service Provider) initiatives—banks cannot be circumvented for electronic USD flows, but blockchain can. Even the most challenging stablecoin firms gain limited banking access (Silicon Valley Bank, Lead Bank).

Capitalists may sell their own rope, and banking “traitors” can’t be reabsorbed; Wall Street lacks regulatory authority.

Regulatory priorities are conflicted. Post-2008, “too big to fail” banks are unpopular, yet Crypto may be even more disruptive for financial order than Wall Street.

The ancient strategy of “besiege three sides, leave one open” remains popular among bureaucracies.

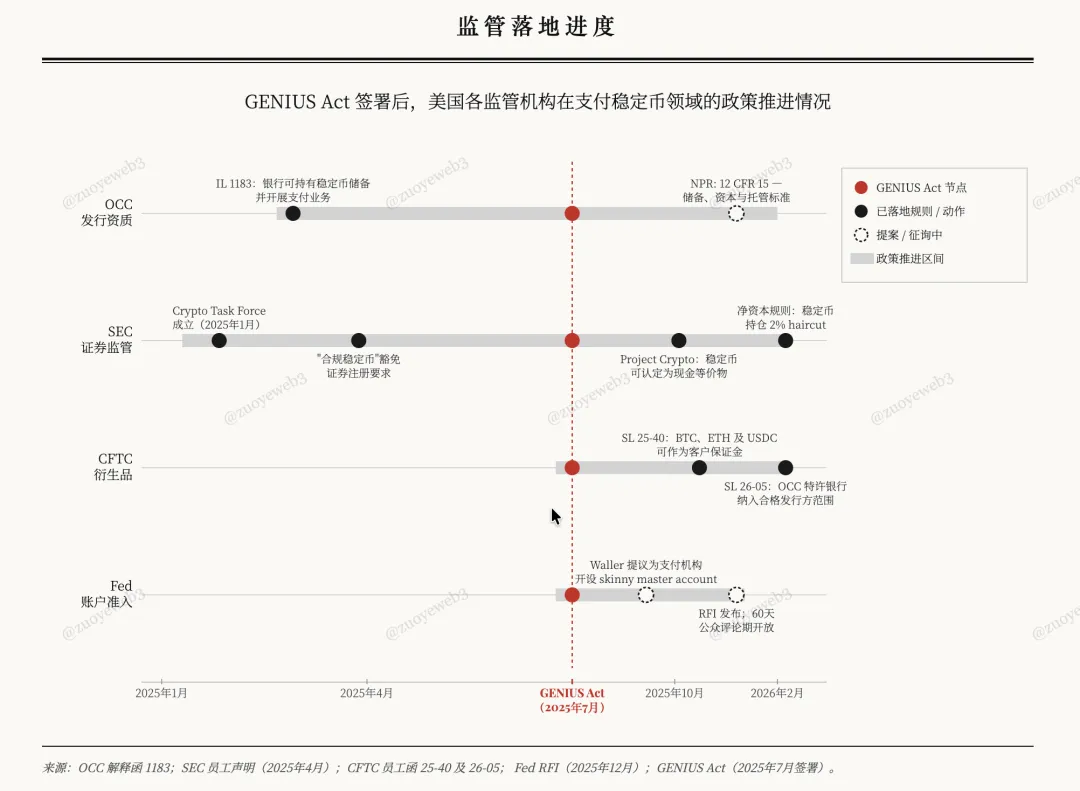

After the Genius Act, Fed, OCC, CFTC, and SEC opened the door to payment stablecoins, but the price was the erasure of yield stablecoins to address banks’ “deposit outflow” fears, guiding stablecoins into existing frameworks.

Image caption: Regulatory rollout progress

Image caption: Regulatory rollout progress

Image source: @ zuoyeweb3

Since Merrill Lynch invented CMA (Cash Management Account) and MMF (Money Market Fund) in the 1970s, banks have blamed them for deposit outflows from small and community banks. The outcome was determined: MMFs supported by CMA offered flexible deposits and withdrawals, as well as higher rates than bank deposits.

Eventually, banks were allowed mixed operations, offering MMF-like products and curbing deposit outflows. Ironically, large banks used their scale to claim deposits from smaller ones.

Heresy is more threatening than heretics.

Yield from stablecoins is not a real issue; banks want to issue their own yields to avoid obsolescence. For example, when Alipay and WeChat dominated in 2013, U.S. banks again protected small banks.

The real victims were U.S.-based Fintech firms like PayPal, fueling the false narrative that third-party payments could disrupt banks by relying on them.

Crypto is genuinely different.

Facing regulatory and banking pressure, Circle is more American and compliant, while Tether is an outsider and upstart. Yet, for a considerable time and across wide regions, $USDC and $USDT aren’t direct competitors.

USDC follows a “+ stablecoin” logic for DeFi + B2B, while USDT follows a “stablecoin +” narrative for CEX + P2P.

It may seem odd, but USDC is more widely used in DeFi as a Quote asset, far outpacing USDT in DEX/Lending and mainstream scenarios. Except for Coinbase, most CEX liquidity is denominated in USDT.

For institutional adoption, USDC is the standard stablecoin, and Circle’s CCTP stack is the institutional gateway to on-chain finance.

USDT is resilient, with $80 billion on Tron supporting global remittance needs. In Argentina and Nigeria, dollarization essentially means USDT-ization.

Joint Artemis and McKinsey research shows that the reported $35 trillion in global stablecoin transaction volume is overstated—only about $390 billion (1%) is actual stablecoin payments, accounting for 0.02% of global payment volume (over $2 trillion).

- B2B payments: $226 billion (60% of use, up 733% YoY), only 0.01% of global B2B payments ($1.6 trillion);

- Payroll and cross-border remittance: $90 billion (<1% global share);

- Clearing and settlement: $8 billion (<0.01% global share);

- U Card: $4.5 billion.

This aligns more closely with real-world experience, and perhaps the adoption trend matters most. Fintech connects to banks, while banks resist stablecoin yields yet support more stablecoins.

Tether’s recent moves—partnering with Lutnick and launching USAT—are camouflage; investing $200 million in Whop is more tangible, effectively buying access to 18 million users, encircling developed markets through remittances from the emerging world.

Thus, remittance firms in Latin America ⇄ US, South Asia ⇄ Middle East, Africa ⇄ Europe are more likely to support USDT, while Stripe and Huma default to USDC.

Crypto’s foundation is P2P; Circle targets enterprise and banking development. The widely reported B2B narrative is mistakenly seen as the future of payments.

As previously noted, pure transfer, settlement, and aggregation channels lack substantial value—transaction volume is a fixed number, lacking the imagination for price-to-dream ratios. Everyone needs a graphics card for gaming—selling 7 billion RTX 5090s at best—while AI’s fourth industrial revolution offers far greater upside.

“Payments are not a SaaS or feature, but AI-powered infrastructure like Cloudflare—a distribution network whose value isn’t determined by transaction count.”

This is the story Crypto wants to tell: stablecoins transcending payments, keeping money end-to-end on-chain.

On-Chain Accumulation

There’s talk of SaaS’s decline and the aging of channel partners, as if decades-old Fintech will be replaced overnight.

That won’t happen so quickly—USDC’s institutional B2B adoption needs time, and Tether’s channel investments may not guarantee future success.

The key metric for Crypto’s payment story is managing the relationship between payment and yield. The situation is clear:

- For yield, remain in on-chain DeFi—MetaMask’s U Card partnership with Aave routes into the U.S., but cannot access broader consumer ecosystems;

- For payment scale, seek an OCC bank license, issue compliant, non-yielding stablecoins, and enter the expansive financial derivatives space governed by CFTC and SEC.

BitGo’s Asia-focused institutional dollar stablecoin $FYUSD and Circle’s euro stablecoin $EURC both deliberately restrict themselves to niche markets.

B2B is about pipelines, C2C about scale, B2C about plugins.

The history of payment stablecoins shows that public chains/L2 offer the hope of replacing card networks, but compared to Fintech’s “displacement” of banks, the advantage should be a new MMF + payment product that surpasses banks in capital efficiency.

Peter Thiel backs Neobank and Neobroker; Vitalik favors yield stablecoins backed by ETH.

Vitalik is more prescient—without ETH-based yield stablecoins to diversify risk, at the very least, consider RWA assets for diversified yield sources.

In summary, without on-chain yield-based payment functions, stablecoins remain subordinate to U.S. assets and will eventually be domesticated by OCC as part of the banking system. Those willing to trade freedom for security end up with neither.

A second risky assertion: Existing USDC-based B2B use cases and USDT-enabled cross-border remittance projects cannot propel payment stablecoins to global adoption—they are only temporarily relevant and won’t be the main players in the next era.

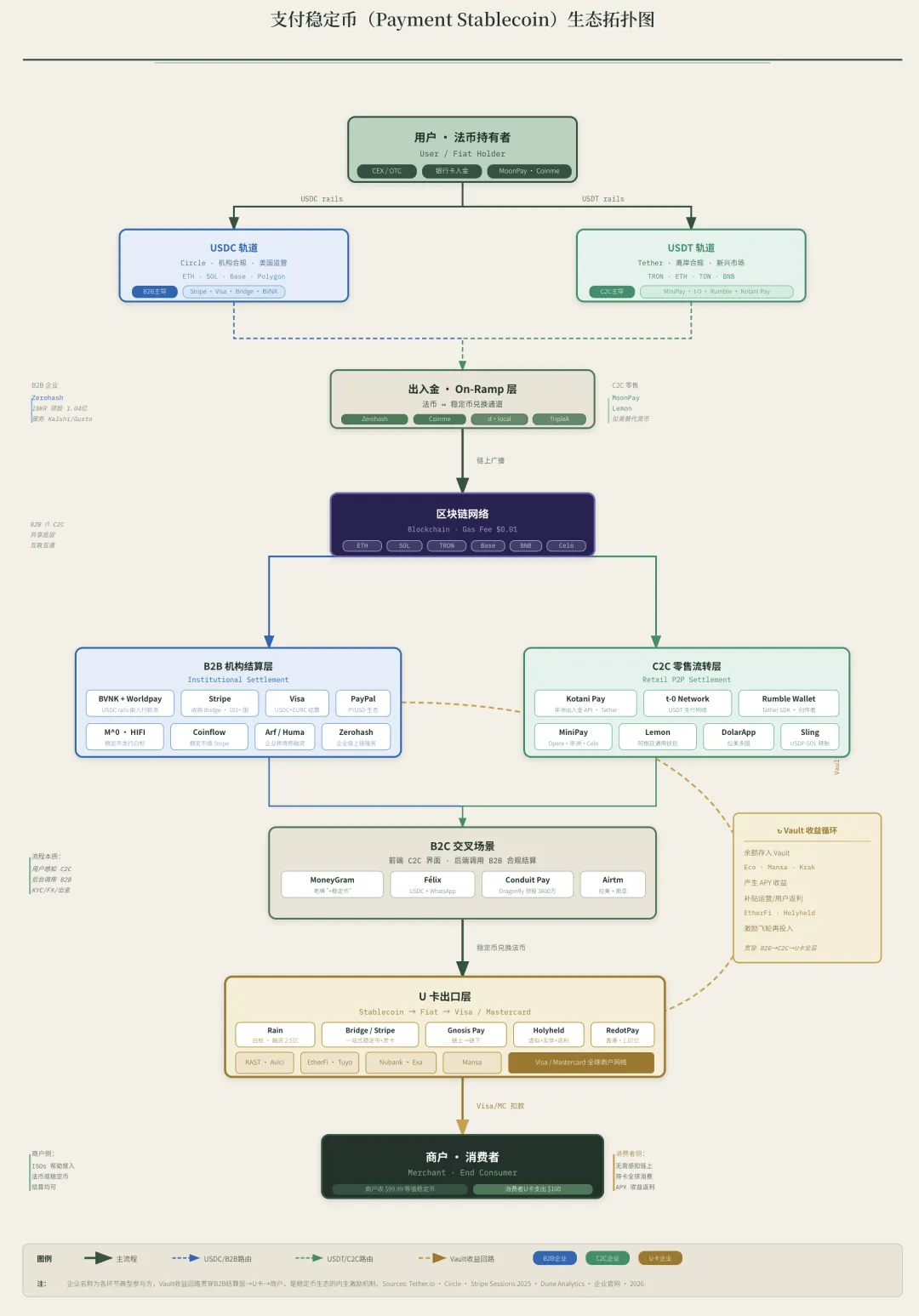

Image caption: Payment stablecoin circulation

Image caption: Payment stablecoin circulation

Image source: @ zuoyeweb3

The phase of using yield as a customer acquisition tool has ended. With banking opposition, both off-chain (post $USDe and $xUSD) and on-chain have cooled, making it imperative to analyze real-world payment adoption.

Be mindful: studying payments without considering yield means missing half the value of this wave. USDT/USDC use Treasury interest to recruit, banks win the third round, and continue to dominate with cheap demand deposits.

Conclusion

While Fintech leads, we hope Crypto charts a different path forward.

Four drivers define the new payment battle: Stripe and others aggressively adopting new narratives for IPO, Meta/Google leveraging channel bargaining power, banks retaining channel fees and cheap assets, and Tether investing heavily in payment companies to encircle Circle.

Two new narratives are bundled into expectations for the future: stablecoins are assumed to be Agent payment tools, but no one has questioned whether Agents are truly needed.

That question will be addressed in a future article.

Disclaimer:

-

This article is reposted from [佐爷 web3]. Copyright belongs to the original author [佐爷 web3]. If you object to this repost, please contact the Gate Learn team, who will handle it in accordance with relevant procedures.

-

Disclaimer: The views and opinions expressed herein are solely those of the author and do not constitute investment advice.

-

Other language versions of this article are translated by the Gate Learn team. Reproduction, dissemination, or plagiarism of translated content without reference to Gate is strictly prohibited.