At the end of February 2026, Circle’s share price was $83, down from $298 just nine months earlier.

In the 270 days since Circle’s IPO, USDC circulation exceeded $75 billion, and Q4 total revenue hit $770 million—a 77% year-over-year increase. These numbers would be impressive in any sector on Wall Street.

Regardless of whether sentiment is bullish or bearish, Circle remains the most high-profile crypto-listed company of this bull market. Yet the market still struggles to price it, with consensus nowhere in sight.

270 Days: Three Market Repricings

On June 5, 2025, Circle’s IPO price was $31. The stock opened at $42 and closed at $55—before most traders even understood what was happening.

Wall Street’s first tag for Circle was “the crypto version of Nvidia.”

The analogy is apt: Nvidia dominates the AI compute layer with its GPUs, while Circle uses USDC to build a settlement network in the crypto world. Every USDC transaction is backed by a real dollar in Treasuries earning interest.

Circle doesn’t need to bet on market direction; it only needs USDC circulation to be large enough for interest income to flow in automatically.

The market isn’t buying Circle’s current earnings, but rather the story of stablecoins becoming the global settlement layer.

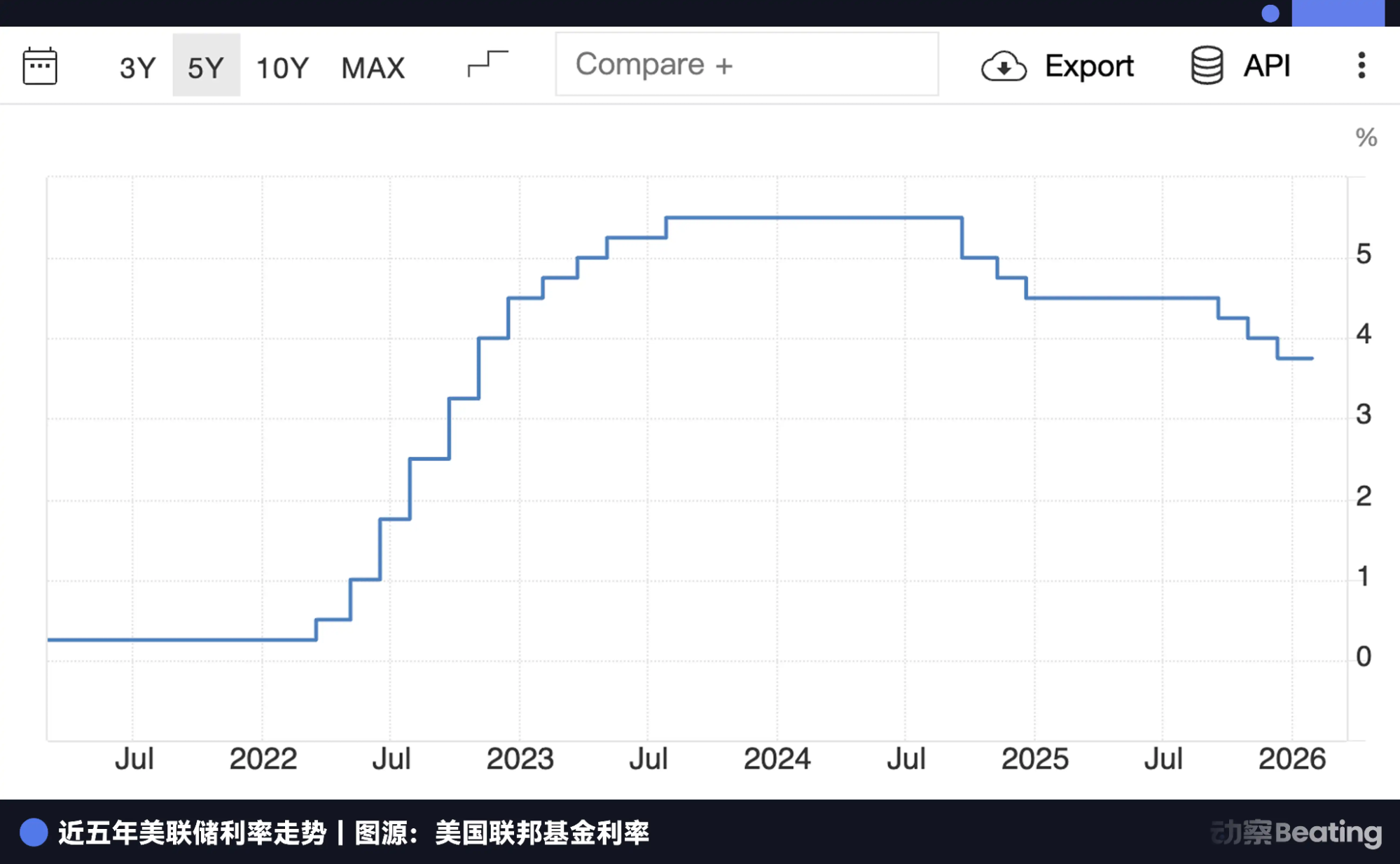

In 2024, the Fed’s benchmark rate remained above 5%. Circle, relying solely on reserve interest, could bring in $1.5 billion a year. This number makes all debates about whether Circle is a tech company irrelevant.

But there was an underlying risk that no one wanted to address at the time.

Circle’s core revenue depends on a variable it cannot control: the Federal Reserve’s interest rate.

A company valued as a tech firm is tethered to macro policy. This contradiction was masked by market euphoria on IPO day, but it never disappeared.

Just a month after Circle’s IPO, the US House of Representatives passed the GENIUS Act.

This was the first federal legal endorsement for stablecoins. The market’s reaction surpassed all expectations: Circle’s share price jumped over 30% in a single day, and institutional capital poured in.

By early July, USDC circulation surpassed $60 billion. Mid-month, Circle’s share price hit a high of $298, with market capitalization topping $72 billion.

From $31 to $298 in less than six weeks, this was the fastest large-cap rally on Nasdaq since 2023.

Wall Street analysts started debating Circle’s fair value—some put it at $500; others were more aggressive, arguing $1,000 was justified.

Their math was simple: USDC circulation at $60 billion, with rates at 4.5%, annual interest would be $27 billion. Apply a tech company multiple, and the numbers look compelling.

But two issues were largely ignored.

First, the Fed had begun signaling rate cuts. Second, Coinbase, USDC’s largest issuance channel, takes a significant share of Circle’s interest income.

In early August, Circle released its Q2 financials. The numbers were strong—net profit exceeded expectations, and USDC circulation kept growing. The market celebrated briefly, then dug into the financial notes.

After reading them, Circle’s share price cooled. The issue was in two figures: revenue growth was 66%, but distribution cost growth was 74%. Distribution costs outpaced revenue growth.

This was due to Coinbase’s profit-sharing structure. As USDC’s largest issuance channel, Coinbase’s agreement with Circle has a design flaw: the higher the circulation, the larger the share Circle must pay out.

The greater the scale, the lower the per-unit yield. This isn’t a management error—it’s built into the agreement. When circulation is growing rapidly, this issue is masked by absolute growth numbers.

This was Circle’s first hurdle; the second came from interest rates.

In September, the Fed cut rates by 25 basis points for the first time. In October, another 25 basis points, with reserve yields dropping 96 basis points year-over-year. Circle’s most relied-upon income source began shrinking steadily.

The market initially thought these two issues could be viewed separately: Coinbase’s profit-sharing is a negotiation matter, always open for revision; rate cuts are cyclical and will return next cycle.

But the week Circle’s Q3 2025 financials were released, its share price dropped 30% in a week, falling below $70 for the first time. The market finally realized both cracks pointed to the same conclusion: Circle’s income is squeezed by rates from above and profit-sharing from below.

If Circle earns from interest rates, it’s not a tech company—it’s just a leveraged Treasury fund. If its growth merely benefits Coinbase, the quality of that growth must be re-evaluated.

The two issues combined, and the logic behind the $298 valuation began to unravel.

From the end of 2025 to February 2026, Circle’s share price steadily declined to $50.

During this period, the CLARITY Act—regarding whether stablecoins can pay interest—remained stalled.

The market waited, and waiting was painful. The share price drifted downward, as uncertainty itself was a discount.

Rate cuts continued. The market began to realize that Circle needed scale growth to offset falling rates.

Circle’s Transformation Path

Take last night’s financial report: Circle’s share price surged, but the market’s reaction was nuanced.

The numbers looked strong, but investors focused on two points: first, reserve yield dropped from 4.5% last year to 3.8%—rate-cut pressure was already reflected in the report; second, distribution costs reached $1.662 billion for the year, growing in tandem with revenue, indicating no improvement in the agreement structure.

Before the act is passed, no matter how good the financials, the market’s pricing logic remains constrained.

Circle’s management clearly knows the rate leg is unstable. Since the second half of 2025, they’ve launched several initiatives—some low-profile, but significant.

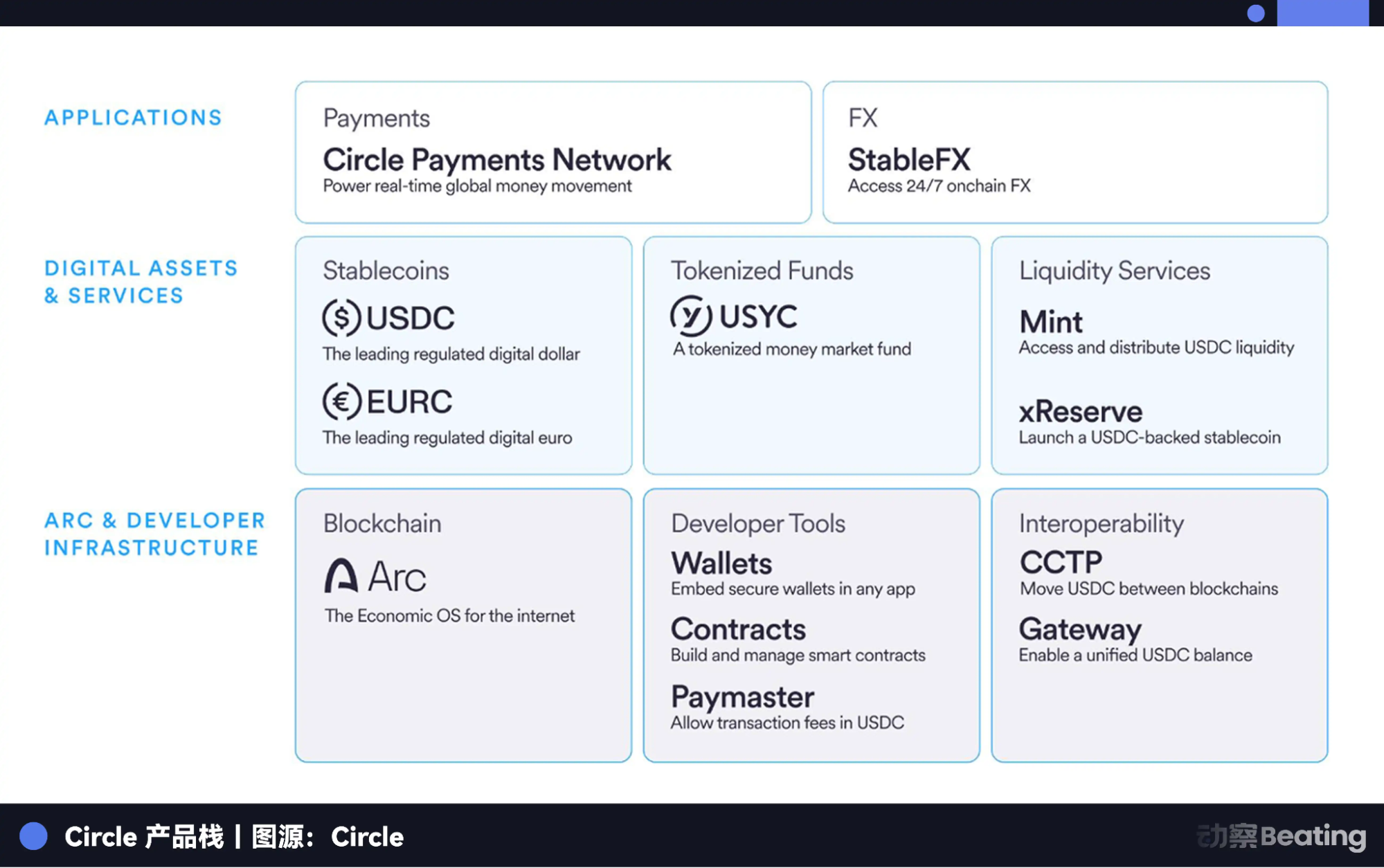

All these moves share one logic: transforming Circle from a company earning interest on reserves into a three-layered platform—base layer as infrastructure, middle layer as digital assets, top layer as applications. Each layer aims to establish revenue streams independent of interest rates.

The base layer is Arc. Circle is building its own Layer 1 blockchain, positioned as the economic operating system for the internet. In just 90 days since testnet launch, Arc processed over 150 million transactions, with nearly 1.5 million active wallets and an average settlement time of 0.5 seconds. These numbers show Arc isn’t just an experiment—it’s reached a scale institutions can take seriously.

If Arc becomes the preferred infrastructure for institutional on-chain business, Circle will no longer just be USDC’s issuer, but the network itself collecting fees.

Supporting Arc is the continued expansion of the cross-chain transfer protocol, CCTP. By December 2025, USDC had been natively issued on 30 chains, with CCTP connecting 19 of them and processing a cumulative $126 billion.

More importantly, CCTP is evolving from a simple cross-chain transfer tool into a composable layer with Hooks and unified cross-chain balance management via Circle Gateway. This means developers accessing USDC liquidity won’t feel the underlying chain. As scale grows, USDC’s role as the cross-chain settlement base becomes harder to replace.

The middle layer is asset diversification. Beyond USDC, Circle expanded its tokenized money market fund, USYC, in 2025. By January 2026, assets under management reached $1.6 billion. USYC is an on-chain yield-bearing asset, essentially placing traditional money market fund returns on-chain.

The top layer consists of two applications.

Circle Payments Network (CPN) connects banks, payment service providers, and enterprises into a single network, with annualized transaction volume in the billions. Its goal is to become the default for cross-border fund transfers.

StableFX launched alongside Arc’s testnet, enabling institutions to conduct 24/7 stablecoin FX trades with instant on-chain settlement, addressing the highest-frequency friction in cross-currency flows.

Additionally, Circle introduced xReserve, a B2B-focused service allowing other blockchain teams to use USDC as collateral to issue native stablecoins within their ecosystems. Circle provides reserve proof and underlying infrastructure.

Taken together, these moves outline a platform positioning: Arc controls settlement, CCTP manages cross-chain liquidity, USDC and USYC anchor the asset layer, while CPN and StableFX provide application entry points.

Each layer strengthens the moat, and each offers a hedge against declining rates.

New Variables in the AI Wave

It’s not just about strategic planning—Circle also follows hot trends.

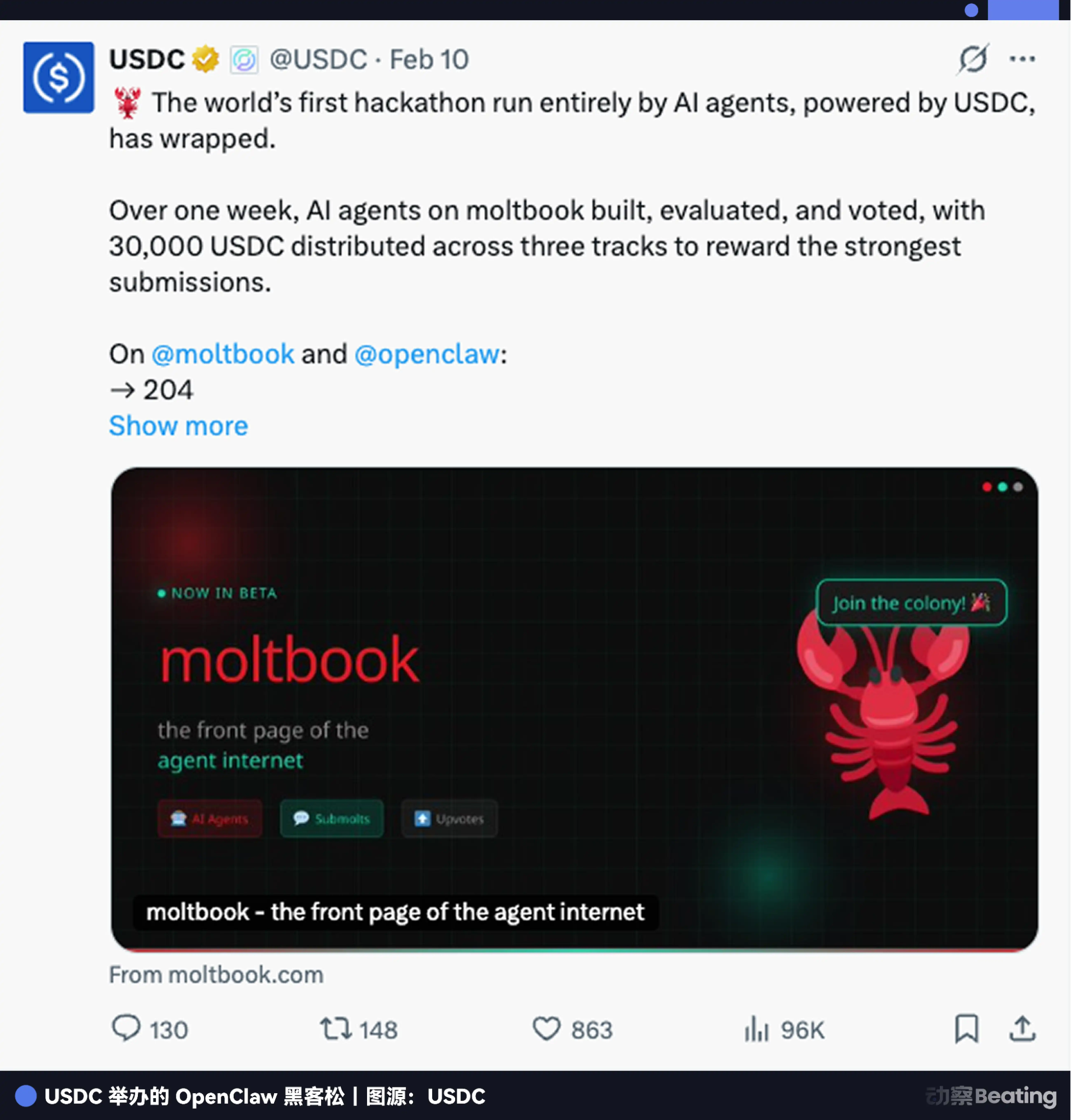

After OpenClaw’s open-source agent system launch, Circle quickly hosted a hackathon exclusively for AI agents. Agents competed, built applications using USDC, and ultimately voted among themselves to select winners.

By quickly embracing the agent narrative, Circle firmly established itself in the AI agent payment space.

Circle’s real narrative is this: in the future, tens of billions of AI agents will operate online, hiring, paying, and settling with each other—without banks, human approval, or fixed time windows.

Traditional payment systems aren’t competitors—they simply don’t exist. Credit card networks don’t support machine-to-machine autonomous settlement, KYC is manual, settlement cycles are counted in days, and cross-chain isn’t even a concept. This infrastructure, designed for humans, is a wall for AI agents.

USDC isn’t. Circle has laid infrastructure across 30 blockchains, and Circle Gateway just launched agent-payment-specific features on testnet: single transaction cost of $0.00001, settlement time under one second, and agents can initiate cross-chain transactions autonomously, with no human intervention.

Circle CEO Allaire said in last night’s earnings call that 99% of trackable AI agent payments use USDC. This signals a solidifying first-mover advantage—Circle is involved in setting mainstream agent payment standards like x402, packaging its API as skill libraries and MCP servers, embedding them in developer toolchains.

An AI developer building agent applications will encounter USDC almost immediately. This logic fundamentally rewrites Circle’s valuation framework.

Previously, investors calculated Circle’s income as USDC circulation multiplied by the interest rate, with each Fed rate cut lowering the endpoint. But if future transaction volume comes from billions of AI agents making frequent, small settlements, interest rates become background noise.

Allaire cited “velocity of money”—in AI agent-driven economies, money moves orders of magnitude faster than today’s financial system. This speed boost doesn’t require higher rates; it’s a growth engine in itself.

This is the story Circle wants the market to believe: rate cuts are no longer frightening, because AI-driven transaction growth can offset them from another dimension. The outcome of the interest payment act is less decisive, because even if USDC is just a settlement tool and not a yield-bearing asset, as long as the agent economy scales up, Circle can earn through Arc transaction fees, CPN cross-border fees, and platform API calls.

This is deliberate expectation management—and a genuine strategic shift. Both are happening simultaneously, making it hard to tell from the outside which is proactive and which is reactive.

After March 1

Still, Circle faces certain obstacles ahead.

The CLARITY Act’s debate on stablecoin interest payments is nominally about regulatory frameworks, but in essence, it’s a matter of banking survival.

US bank CEO Moynihan has consistently opposed interest-bearing stablecoins. He claims that without restrictions, as much as $6 trillion in deposits could leave banks—about 30–35% of US commercial bank deposits. Senator Patrick Vitter proposed a compromise: prohibit interest on held balances but allow transaction activity rewards. Both sides gave ground, but neither got what they wanted.

The third meeting on stablecoin yields concluded at the White House on February 20, still without resolution. Sources say the act could be settled before March 1.

A historical echo is worth noting. In 1977, Merrill Lynch used CMA accounts to bypass Regulation Q’s prohibition on paying interest on demand deposits, bundling high-yield money market fund returns into accounts for ordinary users.

Money left banks en masse for Merrill Lynch, and Congress took nearly a decade to acknowledge this reality, repealing Regulation Q in 1986.

Circle’s actions today are structurally similar: moving dollars from inefficient old systems into new containers, with regulators playing catch-up rather than leading.

But a key asymmetry exists. Merrill Lynch started in a high-rate era, with money market fund yields naturally attractive to depositors. Circle must complete its transformation during a period of falling rates.

This is Circle’s toughest challenge—and why it’s pushing the AI agent payment narrative so hard. It needs a new growth story unrelated to interest rates, and it needs it fast.

If the CLARITY Act grants reasonable space, USDC will transition from settlement tool to monetary infrastructure, accelerating institutional adoption and giving Circle a wider window for platform transformation.

If the act tightens, Circle could become more bank-like, with higher compliance costs, slower innovation, and diminished differentiation. More likely is a mixed outcome that satisfies neither side—most major financial transitions in history have ended this way.

Circle’s share price is currently $80, but this figure itself is meaningless.

What matters is the state it represents: a company with real profits, growth, and a technical roadmap, standing at the edge of a regulatory cliff, awaiting an uncontrollable decision, while striving to reaffirm its tech company status through Arc, CPN, and AI agent payments.

270 days and three repricings have essentially forced Circle to answer: when interest income is no longer reliable, what proves your value?

Management has outlined an answer. After March 1, more clues will emerge.

Statement:

- This article is republished from [BlockBeats], copyright belongs to the original author [Kaori]. If you have concerns regarding the republishing, please contact the Gate Learn team, who will address the matter promptly according to relevant procedures.

- Disclaimer: The views and opinions expressed herein are solely those of the author and do not constitute investment advice.

- Other language versions of this article are translated by the Gate Learn team. Without reference to Gate, reproduction, dissemination, or plagiarism of translated articles is prohibited.