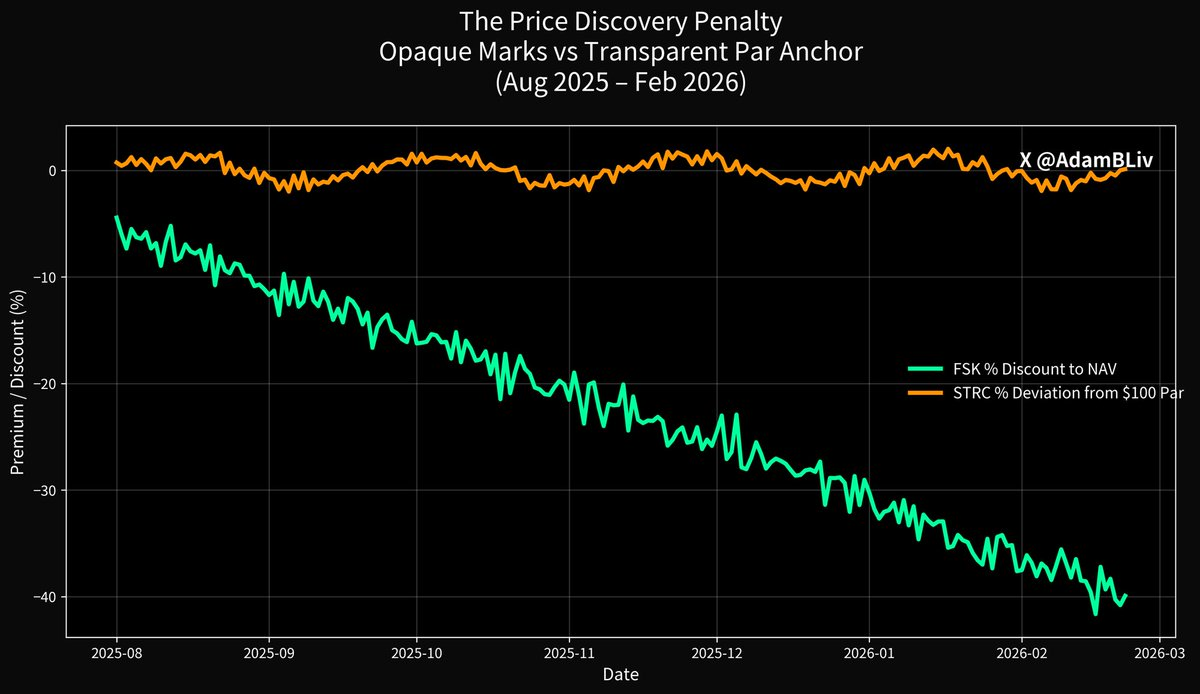

One vehicle that tracks the exact same corner of the credit universe is down roughly 45% in the past year, sitting around $13 a share and bleeding investor confidence by the day.

Another, operating in the same rate environment, same macro backdrop, same borrower stresses, is trading right around its $100 par value and has delivered low-teens total returns over the same stretch. It is operating at low volatility even after a 50% drop in the underlying asset.

Your brain is correctly screaming that something fundamental is different here.

That first vehicle is FSK, the giant publicly traded BDC that serves as the closest real-time proxy for the private credit complex. The second is STRC, Strategy’s exchange-listed perpetual preferred, nicknamed “Stretch.” Same world. Totally different outcome. And that gap is the visible fracture line between an industry built on faith, infrequent marks, and gated liquidity versus one built on real-time price discovery, structural par anchors, and an asset backstop the market can actually see and verify.

Let’s start with the trick that private credit has pulled off for fifteen years.

When most people think they’re buying “private credit exposure,” they usually picture owning the loans themselves. We’re talking senior secured paper with covenants, collateral, and a floating rate that resets higher when Fed funds rise. What they often actually own is the levered equity wrapper sitting underneath a pile of those illiquid loans.

That wrapper, whether a BDC like FSK, a closed-end interval fund, or a drawdown vehicle, promises a smooth dividend while the underlying credit risk gets priced in real time by anyone willing to look. Volatility just concentrates in the equity layer and gets hidden from the end investor until the moment it can’t be hidden anymore.

FSK’s own Q3 2025 filing spells it out in black and white. $13.4 billion portfolio. 63.2% senior secured. Sounds conservative until you remember that “senior secured” still loses money when enough borrowers miss covenants, PIK, or default outright. Non-accruals were already climbing to 2.9% at fair value (5.0% at amortized cost), and ratings agencies were flagging rising losses.

The stock trades at a massive discount to the reported NAV of $21.99 because the market stopped believing the marks. That is price discovery doing its job when the wrapper finally has to face reality.

Now zoom out and you see why the entire private credit complex grew so explosively after 2008. Remember when banks were (deservedly) crushed by new regulation? Higher capital charges, Volcker Rule, liquidity coverage ratios. Borrowers still needed leverage. Non-bank lenders stepped into the vacuum and sold a beautiful story to everyone.

Same underwriting discipline as banks, higher yields for you the investor, and, most importantly, a smoother ride because we control the marks and the gates. Post-GFC handoff complete.

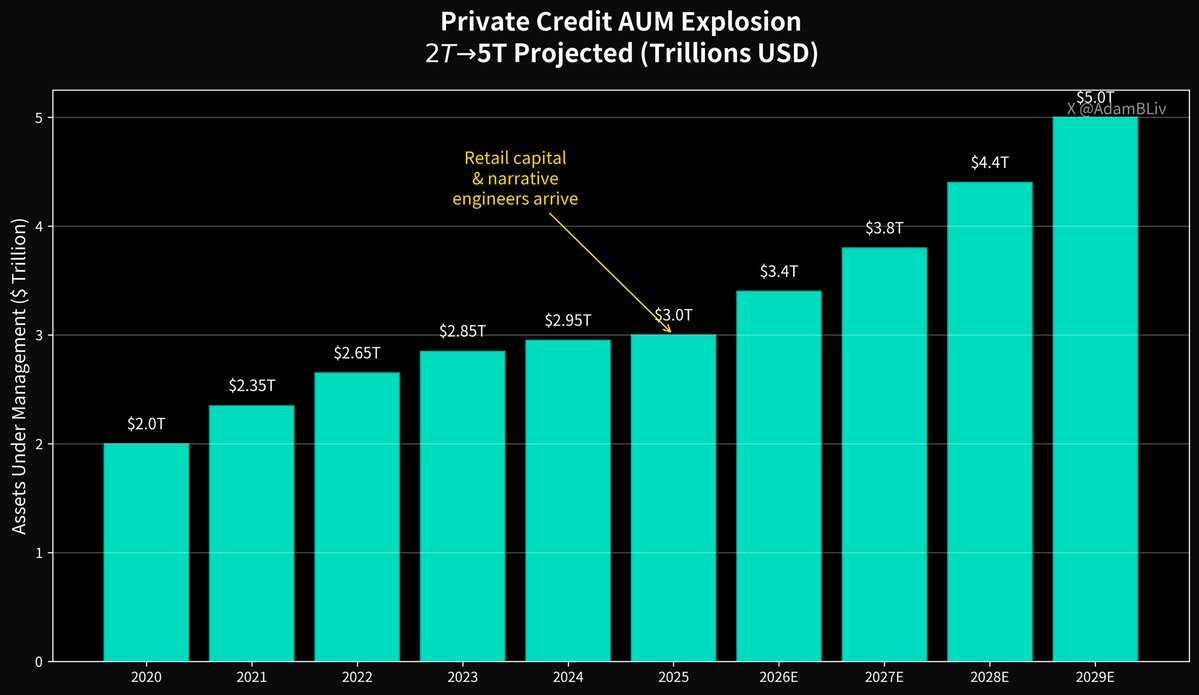

By the start of 2025, according to Morgan Stanley, the global private credit market stood at roughly $3 trillion, up from $2 trillion in 2020, on a trajectory toward $5 trillion by 2029. When any asset class grows that fast, it attracts two predictable groups.

Retail capital chasing yield and narrative engineers polishing the story.

The priesthood’s favorite hymn is “low volatility.” But that begs the question…

How do you manufacture low volatility out of inherently illiquid, long-duration loans?

You mark them quarterly or semi-annually using models and manager judgment. You tell investors “trust the process.” You build structures where liquidity is a privilege and not a right. Redemption gates, notice periods, side pockets, tender limits.

The IMF has been waving red flags on exactly this for years because valuation is infrequent, credit quality is harder to assess in real time, interconnections across the non-bank financial system are opaque, and retail participation is rising fast in vehicles that promise quarterly or even more frequent liquidity against assets that can take months or years to sell without fire-sale discounts.

The BIS put it even more bluntly. Retail-facing structures that offer seemingly liquid shares backed by illiquid private loans are baking in a classic liquidity mismatch. That mismatch is fine in calm markets. In stress, it becomes the thing that turns a credit correction into a redemption spiral.

We’ve already seen the previews. Blue Owl, one of the largest retail-facing private credit platforms, quietly shifted its flagship vehicle away from normal redemption mechanics, effectively telling investors “we’ll return capital as we can sell assets over time.” Activists immediately surfaced offering to buy out frustrated LPs at 30-40% discounts to the stated NAV.

That is the market telling you the marks were optimistic. Headlines about writedowns and “what’s hiding in there” are back because the first time a big name takes a real hit, everyone starts wondering who else is still marking fantasy.

Contrast that with what digital credit actually is in the STRC example.

It is exchange-traded on Nasdaq. Price discovery happens every millisecond. Disclosures are SEC-filed and real-time. The instrument itself is structurally engineered to trade near its $100 par. Strategy’s own language is crystal clear: STRC is perpetual preferred paying a variable dividend, adjusted monthly, with the explicit policy goal of encouraging trading around par and stripping out unnecessary price volatility.

Instead of hiding the price, this is using the price as a governor.

That design is profound. Private credit sells “smooth” by suppressing price discovery. Digital credit can be smooth because the contract itself contains a par anchor and an issuer whose economic incentive is to keep the security trading where retail and institutional buyers expect preferred paper to trade. When the price drifts below par, the dividend rate steps up to attract buyers. When it drifts above, the rate comes down. The market and the issuer are in a constant, transparent negotiation that keeps the security behaving like high-yield credit should… attractive yield with far less gratuitous price swing than levered equity wrappers.

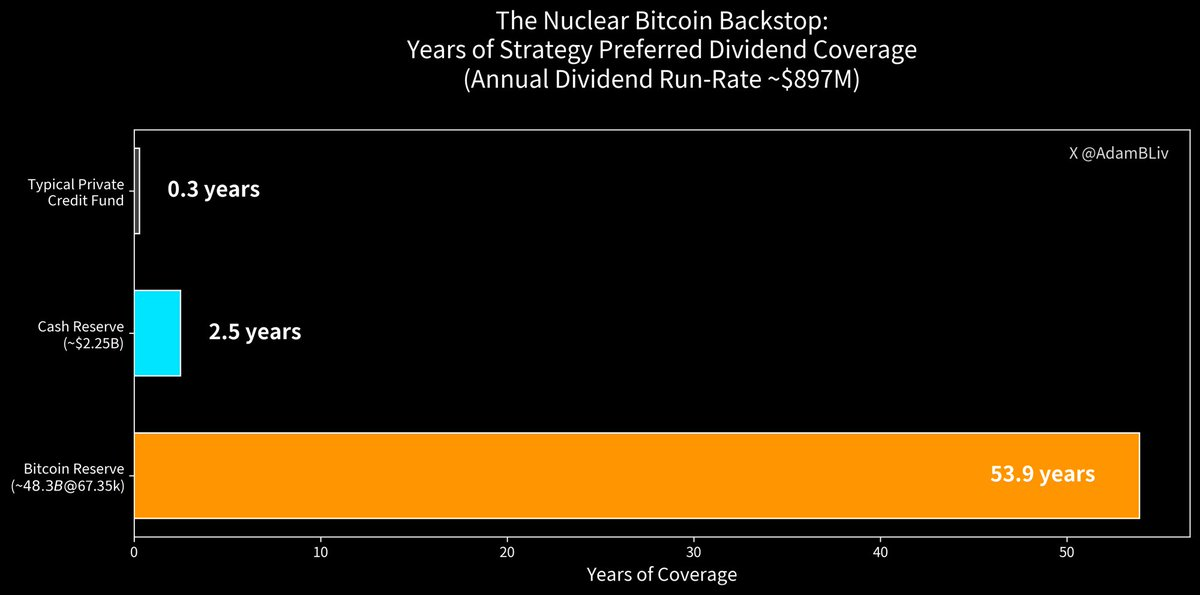

Now layer on the actual safety buffer. Strategy’s STRC is currently paying 11.25% annually, distributed monthly in cash. Notional outstanding sits at $3.458 billion. That implies a run-rate dividend obligation of roughly $389 million per year. Strategy has $2.25 billion in cash, explicitly earmarked in part as a USD Reserve to support preferred dividends and debt service.

This is roughly 2.5 years of cash coverage on the preferred stack, but even that understates the fortress once you include the nuclear backstop.

Strategy owns 713,502 BTC. At spot prices around $67,521, that reserve is worth approximately $48 billion. Even after conservative haircuts for what is earmarked where, the scale is absurd relative to the $389 million annual STRC dividend run-rate. Mechanically, on paper, you are looking at multiple decades, over half a century of coverage before you even touch the cash buffer. And that is after a 50% drawdown in Bitcoin.

This does not mean dividends are paid by selling Bitcoin every month. It means the issuer’s balance sheet carries an extraordinary, verifiable, liquid asset that the market can see, price, and stress-test in real time.

The psychology of credit risk changes completely when the backstop is not “trust our models” but “here is a hard asset the entire planet can verify on a public ledger.”

Private credit safety has always been more optical illusion than engineering. Stale marks that only get updated when convenient, gates and tender limits that evaporate exactly when you need liquidity, credit quality that becomes visible only after non-accruals spike, and interconnections that regulators admit they cannot fully map.

The IMF’s polite language about “infrequent valuation and unclear system-wide linkages” is basically saying “You do not actually know what you own until the moment you try to exit.”

And the cycle is maturing in the classic way. The sector is now so large and fee-rich that even the banks that were regulated out of the space fifteen years ago are rushing back in through partnerships, co-lending, and balance-sheet deals. When the incumbents pile in to capture the spread, you are not early anymore.

So why does FSK get wrecked while STRC stays pinned near par?

Because FSK is private credit exposure plus leverage, plus equity volatility, plus discount-to-NAV risk, plus real-time market panic repricing the underlying loan book.

STRC is credit-like exposure (also in an equity wrapper) minus those amplifiers and plus four deliberate upgrades:

- Par-anchoring mechanics that use dividend policy as a stabilizer

- Transparent, continuous, exchange-traded price discovery

- Disclosed, massive issuer-level buffers (cash plus Bitcoin treasury)

- Monthly cash dividends paid when declared, with zero reliance on “trust the process”

Private credit built its empire on the promise that you could harvest yield without ever seeing how the sausage was made. Digital credit is the opposite. The sausage is made in public, the price is set in public, the disclosures are exhaustive and real-time, and when you need liquidity you simply hit “sell” on your brokerage platform instead of filing a redemption request and praying the gate stays open.

Private credit sells stability as a proprietary product available only through them. But stability is not a product. It is an emergent property of superior structure: yield that is competitive, transparency that is uncompromising, and survivability under stress that does not depend on manager discretion.

Right now the market is voting with its feet, its capital, and its price action.

One side of the ledger is a closed temple where risk is mispriced because it is hidden. The other side is an open, digital, Bitcoin-backed credit ecosystem where risk is priced in real time, backstopped by the hardest asset humanity has ever created, and accessible to anyone with a brokerage account.

The priesthood had a good fifteen-year run. But the temple doors are open, the light is streaming in, and the new architecture is mechanically, mathematically, and psychologically superior.

Digital credit is replacing the private credit market, one honest price, one verifiable backstop, and one frictionless trade at a time.

The next decade of credit will belong to the structures that can deliver yield, transparency, and resilience all at once.

The market has already chosen. The rest is just narrative lag.

Disclaimer:

- This article is reprinted from [AdamBLiv]. All copyrights belong to the original author [AdamBLiv]. If there are objections to this reprint, please contact the Gate Learn team, and they will handle it promptly.

- Liability Disclaimer: The views and opinions expressed in this article are solely those of the author and do not constitute any investment advice.

- Translations of the article into other languages are done by the Gate Learn team. Unless mentioned, copying, distributing, or plagiarizing the translated articles is prohibited.