As Real World Assets (RWA) increasingly become a key focus in the blockchain sector, market discussions have shifted from "how to put assets on-chain" to "how on-chain tokens can truly represent real-world assets." Unlike native crypto assets, RWA involves real-world debt instruments, commodities, real estate, or securities, and thus cannot rely solely on smart contracts for ownership verification and value mapping.

While blockchain can record token transfers, it cannot directly confirm the existence of real-world assets or automatically enforce legal recourse in the physical world. Consequently, RWA is not merely a technical challenge but also a matter of legal structure and financial infrastructure.

To establish a trustworthy link between on-chain tokens and real-world assets, the industry has developed a standardized framework comprising SPVs, custodians, legal agreements, and off-chain enforcement mechanisms.

What Is the Legal Structure of RWA

The legal structure of RWA essentially defines the legal mapping between real-world assets and on-chain tokens. Its primary objective is to ensure that on-chain holders can claim corresponding rights to real-world assets through a legal mechanism.

In most cases, users are not purchasing the asset itself but rather a rights token issued by a legal entity. For instance, a real estate RWA project may not transfer property ownership directly on-chain. Instead, an SPV holds the property and issues tokens on-chain.

Thus, the key to RWA lies not in the token technology itself but in the validity of the legal relationship underpinning the token. Without a sound legal structure, on-chain tokens—even if tradable—cannot genuinely represent real-world asset rights.

What Is the Role of SPV (Special Purpose Vehicle) in RWA

The SPV (Special Purpose Vehicle) is one of the most common legal structures used in RWA.

An SPV is a specially created legal entity designed to independently hold an asset and isolate risk. For example, in a real estate RWA project, the property may be held by an SPV, and the on-chain tokens purchased by users correspond to partial income rights or equity in the SPV.

This structure serves several important purposes.

First, it enables asset isolation. If the project operator faces financial distress, the assets held by the SPV are generally protected.

Second, the SPV clarifies the legal relationship. On-chain tokens can represent equity, debt, or income rights of the SPV, giving investors legally enforceable rights.

Third, an SPV helps projects meet compliance requirements across different jurisdictions, as securities and fund laws in many countries mandate that real-world assets be managed through legal entities.

Why the Custodian Is a Core Player in RWA

Because blockchain cannot directly safeguard real-world assets, RWA must rely on custodians for off-chain asset management.

A custodian's responsibilities typically include:

- Safekeeping of assets

- Verifying asset authenticity

- Maintaining reserve records

- Cooperating with audits and liquidation

- Executing asset disposition in the event of default

For example, in a gold RWA project, physical gold is usually held by a professional vault or financial institution. In a U.S. Treasury RWA, the corresponding bonds may be held in bank or brokerage accounts.

The custodian's credibility directly impacts market trust in the RWA. If the custodian cannot prove that the assets exist, the value basis of the on-chain token is undermined.

Therefore, many large RWA projects implement third-party audits, Proof of Reserve, and regular disclosure mechanisms to enhance transparency.

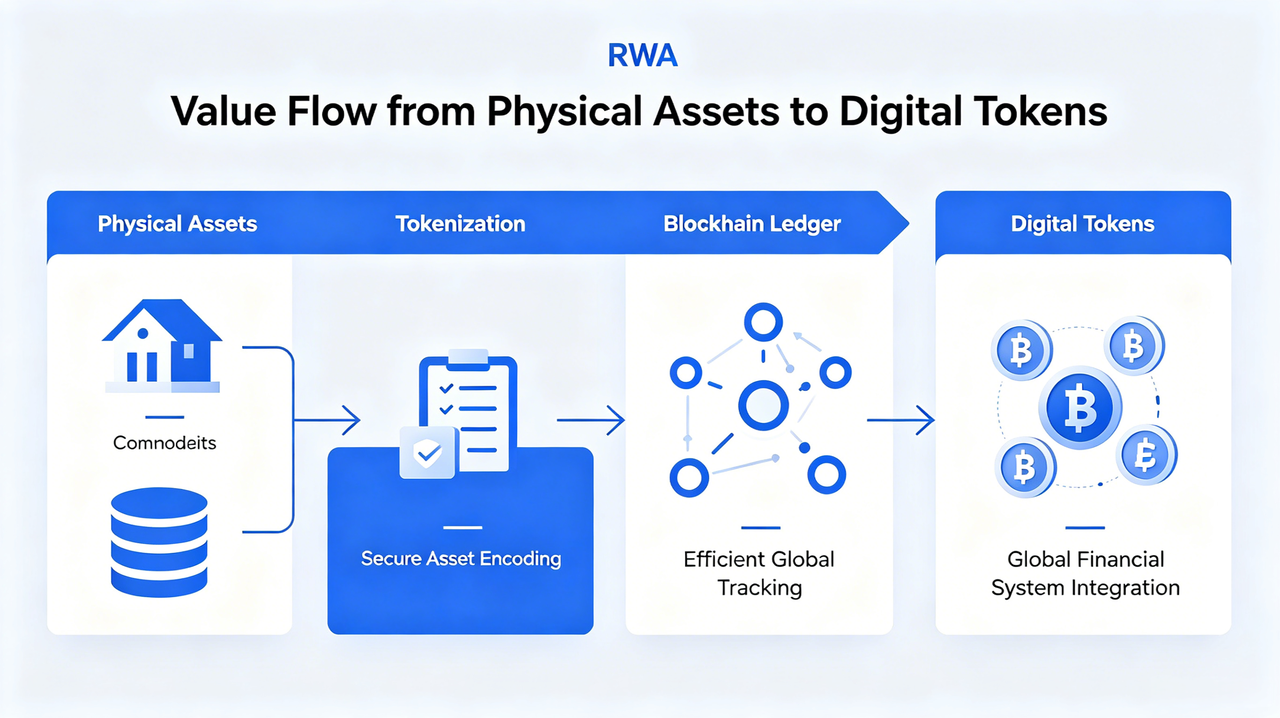

How Off-Chain Assets Map to On-Chain Tokens

A core challenge for RWA is establishing a clear correspondence between real-world assets and on-chain tokens.

This process typically involves several steps:

Asset Ownership Confirmation

First, the legal ownership of the real-world asset must be verified. For instance, U.S. Treasuries, real estate, or gold must be formally held by an SPV or custodian.

Legal Agreement Binding

Then, legal documents define the relationship between the token and the asset, such as whether the token represents income rights, debt rights, or redemption rights.

On-Chain Mapping

Once the asset's legal structure is in place, the project issues corresponding tokens on the blockchain. The number of tokens is typically linked to the asset's value or share.

Oracle Data Synchronization

Since real-world asset prices fluctuate, many RWA projects rely on oracles to sync NAV (Net Asset Value), yield, or market price on-chain.

Through this series of mechanisms, RWA can create a credible bridge between real-world assets and the blockchain.

Why RWA Cannot Operate Outside the Real-World Legal System

Unlike native crypto assets such as Bitcoin or ETH, RWA fundamentally depends on the real-world legal system.

In cases of default, asset loss, or custody issues, smart contracts alone cannot recover real-world assets. Ultimately, courts, regulators, or legal contracts must intervene.

For example:

- Real estate rental defaults require legal enforcement in the physical world

- Bond liquidation relies on the traditional financial system

- Gold redemption requires physical storage and delivery

Therefore, RWA is not a "fully on-chain" financial model but a hybrid that combines on-chain and off-chain elements.

This is why RWA is often described as a "law-first blockchain application."

What Are the Main Legal Risks of RWA

While RWA is seen as a way to improve asset liquidity and global financing efficiency, its legal risks remain a major market concern.

These include:

Asset Authenticity Risk

If off-chain assets do not exist or reserves do not match the tokens, the on-chain assets may lose their value backing.

Custody Risk

If the custodian goes bankrupt, violates regulations, or mismanages assets, token holders may be unable to redeem them.

Regulatory Risk

Countries have widely varying regulations for tokenized securities, fund shares, and on-chain yield products.

Legal Enforcement Risk

Even if token holders have theoretical rights, enforcing them across borders can be difficult.

Thus, a key competitive advantage of any RWA project is not just its technology but whether its legal structure is transparent, stable, and enforceable.

Differences in Legal Structures Across RWA Models

There is no one-size-fits-all legal structure for current RWA projects.

| RWA Type |

Common Legal Structure |

Token Corresponding Rights |

| U.S. Treasury RWA |

SPV + Custody Account |

Income Rights |

| Real Estate RWA |

SPV Holds Property |

Equity / Income Rights |

| Gold RWA |

Custody Vault |

Commodity Reserve Rights |

| Private Credit RWA |

Debt Agreement |

Debt Income Rights |

| Tokenized Fund |

Fund Structure |

Fund Shares |

Each structure directly affects investor rights, regulatory requirements, and liquidation mechanisms.

Conclusion

The core of RWA is not simply asset tokenization; it is about establishing a trustworthy connection between real-world assets and on-chain tokens through SPVs, custodians, legal agreements, and off-chain enforcement. Blockchain can enhance transaction efficiency and global liquidity, but real-world asset ownership verification, custody, and legal enforcement still depend on traditional financial and legal systems.

Therefore, RWA is fundamentally a hybrid financial structure of "on-chain technology + off-chain law." As regulatory, custody, and on-chain infrastructure mature, RWA may accelerate the migration of traditional financial assets to the blockchain and become a key bridge connecting TradFi and DeFi.

FAQs

What is an SPV?

An SPV (Special Purpose Vehicle) is a special purpose entity typically used to independently hold real-world assets and act as a legal intermediary between on-chain tokens and those assets.

Why does RWA need a custodian?

Blockchain cannot directly hold real-world assets, so a custodian is required to manage asset custody, verify reserves, and execute liquidation.

Does an RWA token directly represent asset ownership?

Not necessarily. Many RWA tokens actually correspond to income rights, debt rights, or SPV equity rather than direct ownership of the underlying asset.

What role does an oracle play in RWA?

Oracles sync real-world asset prices, yields, or NAV data to the blockchain, enabling smart contracts to access off-chain information.

What is the biggest legal risk for RWA?

The primary legal risks include asset authenticity risk, custody risk, regulatory uncertainty, and cross-border legal enforcement challenges.